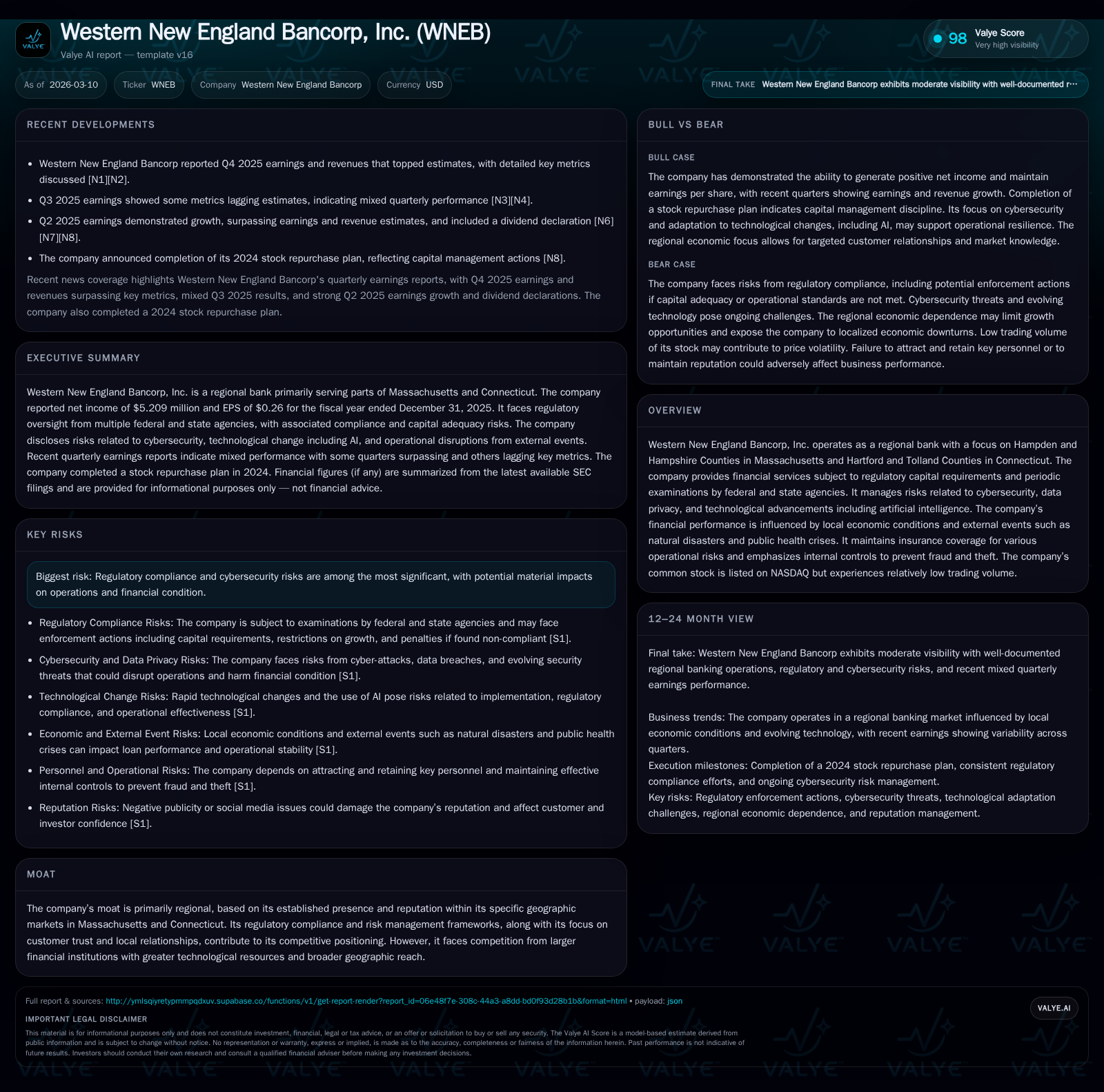

Western New England Bancorp's Regional Focus Faces Growth and Capital Allocation Challenges

WNEB leverages regional banking roots to sustain growth while managing cybersecurity and regulatory risks.

Western New England Bancorp, Inc. (WNEB) operates primarily within select counties in Massachusetts and Connecticut, focusing on traditional banking services tailored to its regional clientele. Its historical performance shows fluctuating net income with a notable rebound in 2025 alongside improved cash flow generation, though return on equity remains modest. Going forward, WNEB’s growth depends heavily on local economic conditions and technological adaptation, particularly around cybersecurity and artificial intelligence risks. Capital allocation reflects disciplined dividends and share repurchases, yet the bank faces the persistent challenge of meeting evolving regulatory capital requirements while addressing competitive pressures from larger institutions.

Company Background and Regional Moat

Western New England Bancorp, Inc., operating as a regional bank focused on Hampden and Hampshire Counties in Massachusetts along with Hartford and Tolland Counties in Connecticut, maintains a localized footprint centered on community banking services. Its moat stems largely from these entrenched local relationships and trust built over time, buttressed by rigorous regulatory compliance and established risk management systems [N1][S1]. Despite this positioning, the company contends with competition from larger financial institutions equipped with greater capital resources and advanced technology capabilities.

Historical Performance Trends

Over the past four fiscal years, WNEB has experienced variable earnings results but visible improvement over the recent period. Reported net income was $5.2 million in FY2025 compared to $3.3 million in FY2024 — a substantial jump of nearly 58% year-over-year — after more muted gains from FY2023 to FY2024 [F1]. Operating cash flow mirrored this trend, rising from $12.2 million to $18.2 million during the same interval, supporting an estimated free cash flow of approximately $17.1 million in FY2025 given relatively modest capital expenditures totaling $1.07 million [F1].

Despite these improvements, return on equity remains contained at around 2.1%, reflecting WNEB’s sizable equity base ($247.6 million at FY2025) typical for community banks relying heavily on traditional lending portfolios [F1]. Dividends have been stable overall ($5.7 million paid in dividends during FY2025), supplemented by disciplined share repurchases which totaled $6.1 million in FY2025 following completion of its 2024 Repurchase Plan authorized earlier [S24][F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 5 | 18 | 1 | +58.4% |

| 2024 | 3 | 12 | 1 | +30.9% |

| 2023 | 3 | 15 | 3 | -72.2% |

| 2022 | 9 | 36 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 6 | 17 |

| 2024 | 6 | 8 | 11 |

| 2023 | 6 | 5 | 12 |

| 2022 | 5 | 6 | 35 |

Source: SEC companyfacts cache [F1].

Note: Year-over-year percentages approximate compound changes between years based on available data.

Regulatory Environment and Risk Management

WNEB operates under substantial regulatory scrutiny given its status as a federally insured financial institution subject to oversight by agencies such as the Federal Reserve Board (FRB), FDIC, OCC, and CFPB [S1][S4][S9]. The company’s risk factors include regulatory compliance failures which could trigger enforcement actions ranging from cease-and-desist orders to monetary penalties or restrictions on business growth [S9]. Capital adequacy is critical; failure to maintain minimum regulatory capital ratios — including Basel III buffers — could impair franchise value through costlier funding or constrained operations [S10][S25]. Extensive internal controls are maintained to mitigate fraud, theft, and operational risks with periodic independent audits [S15][S27].

Cybersecurity risk commands significant attention given persistent threats such as phishing attacks, malware intrusions, and potential data breaches that could damage financial condition or customer trust [S1][S8][S16][S29]. The bank employs multiple committees dedicated to information security oversight and continuously trains employees on social engineering awareness [S1]. Third-party vendor risks are similarly governed through rigorous due diligence processes.

Technological Adaptation Including Artificial Intelligence

Like many institutions contending with industry-wide digital transformation, WNEB has started integrating AI technologies but acknowledges associated risks including inaccurate outputs, intellectual property concerns, legal liabilities, and dependency issues with third-party providers [S6][S25]. The innovative application of AI remains a double-edged sword: it can enhance operational efficiency but also expose the bank to new forms of operational complexity amid a rapidly evolving regulatory landscape.

Local Economic Dependencies and External Risks

WNEB’s performance is tightly linked to the economic fortunes of its core markets in western Massachusetts and central Connecticut [S6][N2]. Factors such as employment levels, real estate values affecting loan collateral quality, and deposit stability drive earnings potential [S11]. External shocks ranging from natural disasters to pandemics can disrupt operations materially despite tested business continuity plans [S11]. Furthermore, competitive pressures increase as regional banks face consolidation trends or aggressive expansion by larger national players with more diversified service offerings.

Outlook: Growth Prospects and Operational Priorities

The primary avenues for growth remain organic expansion within existing markets supported by leveraging technology for enhanced customer experience while maintaining prudent credit practices [N2][S1]. However, growth is constrained by regulatory capital requirements which may necessitate careful balancing between asset growth initiatives versus capital conservation strategies [S10][S25]. Given its modest return metrics relative to peers based on reported numbers [F1], management must focus on improving operational efficiency possibly through further automation or product diversification.

Continued emphasis on cybersecurity resilience coupled with transparent communication about risk management capabilities will be important to safeguard reputational capital which is vital for customer retention amidst increasing digital threats [S17]. Shareholder returns have been supported through steady dividends plus opportunistic buybacks contingent on capital availability rather than aggressive repurchase programs [F1][S24].

Returns and Capital Allocation Summary

WNEB demonstrates a conservative approach to capital allocation characterized by moderate dividend payouts sustained over multiple years alongside recurring share repurchases completing earlier authorized programs [F1][S24]. The free cash flow profile improved markedly in FY2025 driven by higher operating cash flows relative to capex requirements highlighting effective working capital management even as investment needs remain modest reflecting limited technology infrastructure expansions so far.

Given approximate ROE near low single digits (~2%) [F1], there is implied room for improvement either via loan book optimization or controlled expense reduction efforts if growth ambitions are pursued without disproportionate leverage increases.

Additional Considerations

Volatility in WNEB’s stock price related partly to low trading volume creates potential liquidity constraints for investors despite NASDAQ listing status [S13]. The voluntary board retirement announced effective May 14, 2026 suggests forthcoming corporate governance evolution that may impact strategic priorities [S3].

Management's cautious stance regarding issuing new shares limits shareholder dilution risk but reflects sensitivity towards maintaining existing ownership structure amid regulatory capital adequacy concerns [S12].

Conclusion

Western New England Bancorp remains a regionally focused community bank navigating an operating environment defined by tight regulation, intensifying cybersecurity complexities, evolving technological disruption including AI incorporation, and dependence on local economic health for sustainable growth prospects. Its recent financial performance exhibits encouraging signs of recovery although absolute profitability measures suggest ongoing challenges typical of midsized banks balancing legacy operations with innovation imperatives. Capital allocation reflects a balanced mix of returning value through dividends plus disciplined share repurchases while preserving the ability to meet increasing operational needs safely. The bank’s ability to continue adapting effectively within its localized niche will hinge critically on managing emerging risks prudently without losing competitive ground against more resourceful peers.

This analysis does not constitute investment advice or recommendations but aims to provide a detailed factual and contextual assessment based solely on provided public financial disclosures and filings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments