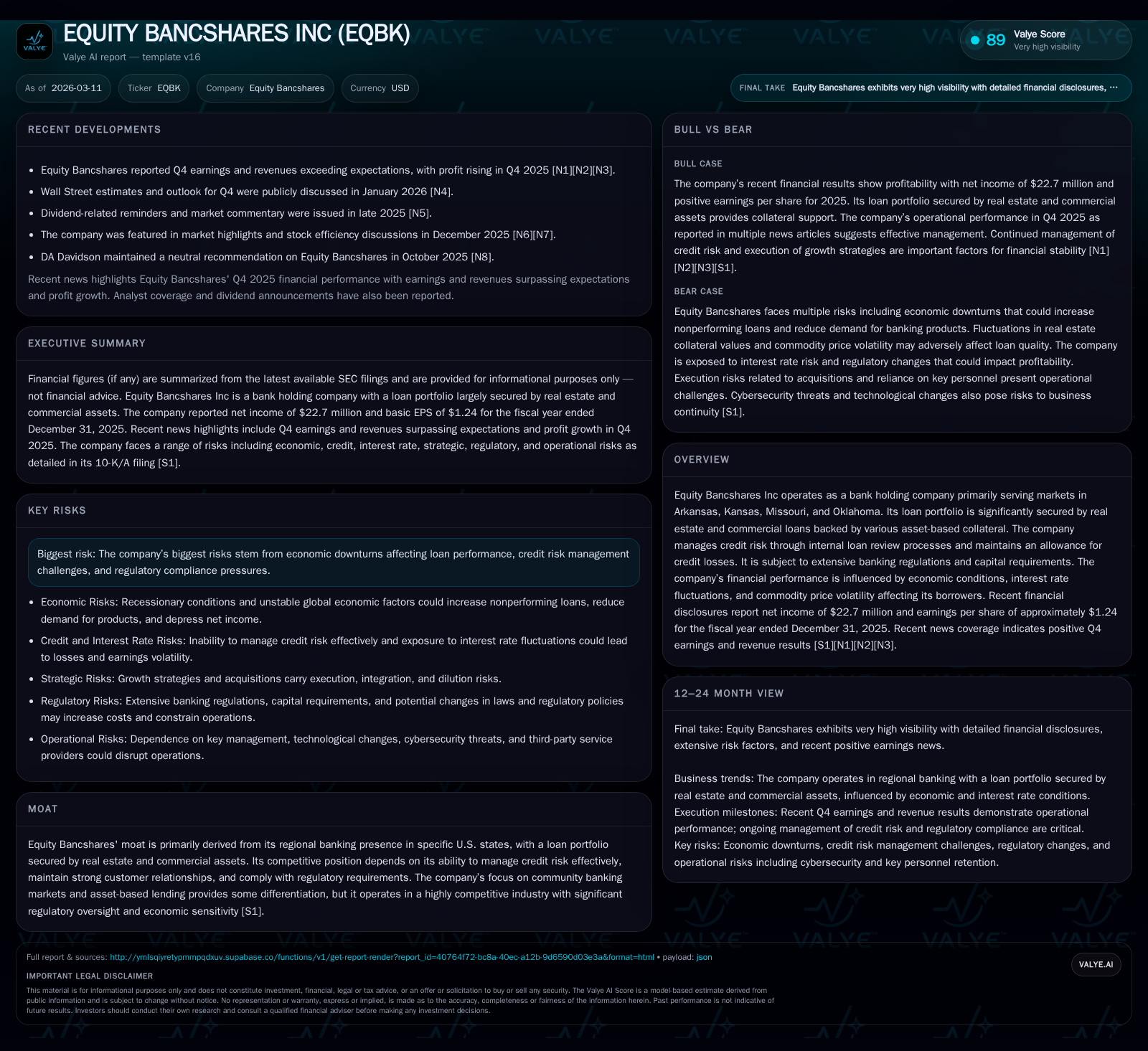

Equity Bancshares Inc: Regional Bank Earnings Rebound and Capital Allocation Strategy

Examining Equity Bancshares’ profitability trends, credit risk approach, and capital deployment amidst regional market and regulatory challenges.

Equity Bancshares experienced a marked net income contraction of 63.7% in 2025 following prior years of robust growth, largely driven by its asset-secured loan portfolio concentrated in four U.S. states. The company manages credit risk through stringent internal reviews and maintains provisions for potential losses, but is sensitive to economic downturns and real estate market fluctuations. Its capital allocation illustrates a balance between dividend payments and scaled-back buybacks amid moderate return on equity, while navigating increasing regulatory scrutiny and operational risks.

Financial Performance Trends: Navigating Fluctuations in Profitability

Equity Bancshares saw significant volatility in its profitability over the past four years culminating in a pronounced net income decline in FY2025. Net income fell to $22.7 million in FY2025 from $62.6 million in FY2024—a drop of approximately 63.7%—after reaching a notable peak the prior year [F1]. This sharp correction contrasts with the more moderate fluctuations seen earlier, such as the $7.8 million net income earned in FY2023 amid ongoing growth initiatives.

Operating cash flow (CFO) mirrored this contraction, decreasing by 30.4% to roughly $51.4 million in FY2025 from $73.8 million in FY2024 [F1]. One contributory factor was a marked increase of 56% in capital expenditures (capex), rising to $13.3 million after spending $8.5 million the year before—a strategic investment that pressured free cash flow generation [F1]. The resultant free cash flow hovered around $38.1 million (CFO minus capex).

Despite this recent dip in profit metrics, shareholder equity expanded notably by about 23% year-over-year to $732 million at end-2025 from $593 million at end-2024, reflecting retained earnings and capital accumulation [F1]. The reported return on equity (ROE) accordingly softened to approximately 3.1%, indicating subdued profitability relative to capital base scale.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 23 | 51 | 13 | -63.7% |

| 2024 | 63 | 74 | 8 | +700.7% |

| 2023 | 8 | 77 | 16 | -86.4% |

| 2022 | 58 | 74 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 14 | 38 | 3.1 |

| 2024 | 12 | 65 | 10.6 |

| 2023 | 18 | 61 | 1.7 |

| 2022 | 33 | 71 | 14.1 |

Source: SEC companyfacts cache [F1].

Table summarizes annual financial performance from FY2022 through FY2025 [F1]

Key Drivers Behind Equity Bancshares’ Historical Growth

Until the recent correction seen in late cycle year FY2025 results were buoyed by strategic focus areas aligning with regional economic strengths across Arkansas (AR), Kansas (KS), Missouri (MO), and Oklahoma (OK) [S7]. The bulk of Equity Bancshares’ loan portfolio is secured by real estate assets alongside commercial loans backed by various forms of asset-based collateral such as accounts receivable or equipment [S1][S7]. These secured lending products have been pivotal drivers of revenue growth given their relative risk mitigation benefits compared to unsecured counterparts.

Concentration within these four midwestern states gives Equity Bancshares both an intimate understanding of local market dynamics and a community banking positioning that distinguishes it from larger national players . The company’s strategy has emphasized relationship-driven banking services targeted at small to medium-sized businesses and entrepreneurs—a segment often underserved by bigger institutions due to smaller credit demand scales [S16].

However this geographic concentration inherently concentrates risk exposure should regional economic conditions soften or real estate markets weaken materially—factors noted as key risk vectors within the company’s filings [S7][S8]. Additionally internal limitations such as federally mandated lower lending limits compared with larger competitors restrict portfolio expansion prospects despite solid organic client demand trends.

Credit Risk Management in a Changing Economic Environment

Equity Bancshares employs robust internal loan review procedures alongside an allowance for credit losses to manage credit risk within its primarily collateralized loan book [S1][S4]. These controls are vital given the company’s high exposure to real estate-secured loans that remain vulnerable to fluctuating property valuations arising from local economic shifts or wider macroeconomic shocks.

Additionally its commercial loan segment relies heavily on asset-based collateral such as inventory or receivables whose values may deteriorate swiftly under recessionary pressures—heightening potential for elevated nonperforming loans or charge-offs if borrowers face distress [S4][S8]. Recent filings emphasize sensitivity to regional economic cycles including commodity price volatility impacting borrower sectors such as agriculture or manufacturing prevalent across its operating footprint [S7].

Economic stress scenarios further challenge underwriting discipline especially where historic asset values provide less cushion against downside risks—an issue compounded by recovery uncertainties tied to prolonged inflationary environments or monetary policy tightening cycles [S1]. The company’s management explicitly flags risks of rising delinquencies and foreclosures during downturns which could materially affect financial outcomes despite conservative provisioning strategies [S8].

Earnings Drivers and Constraints Moving Forward

Forward-looking earnings will hinge on multiple interrelated factors including interest rate movements that influence net interest margins given funding cost volatility; deposit competition intensified by customer shifts toward alternative investment vehicles; ongoing regional economic health; and regulatory cost pressures [S1][S9].

The highly competitive landscape pits Equity Bancshares not only against other community banks but also larger national banks with greater resources and non-bank fintech entrants offering digitally optimized lending or deposit products often at lower operational costs—pressing margin compression risks [S19]. Furthermore technological investments necessary for digital channel expansion impose upfront costs potentially offsetting efficiency gains over several periods—representing a medium-term constraint on earnings improvement efforts [S4][S9].

Maintaining deposit inflows at competitive pricing remains crucial as deposits constitute the company’s primary low-cost funding source; any sustained outflows toward money market funds or short-term securities could raise overall funding costs reducing net interest income contribution significantly [S5][S9].

Capital Allocation: Dividends, Buybacks, and Funding Strategy

Capital management reflects a conservative but disciplined approach balancing payout consistency with shareholder value preservation amid volatile earnings achievement.

In February 2026 the Board declared a quarterly cash dividend of $0.18 per share payable April 15 to shareholders of record at March 31 indicating ongoing commitment to returning capital even during earnings softness periods [S3]. Historically however dividends have been modest relative to net income reflecting reinvestment priorities.

Share repurchases have decelerated somewhat—from peaks exceeding $33 million annually in FY2022 down to nearly $14 million executed in FY2025—despite growing equity levels signaling strategic caution possibly driven by uncertain near-term profitability outlooks and regulatory capital considerations [F1]. The equity base expanded robustly over the interval reaching $732 million suggesting capacity for potential future buyback resumption if conditions stabilize.

Return on equity remains muted around low-single digits—in line with community bank norms but below large bank peers—highlighting room for improved capital efficiency though constrained by regulatory capital charges linked to loan collateralization profiles and risk weightings typical for mid-sized regional banks [F1][S11].

Regulatory Environment and Operational Risks Impacting Returns

Post-2023 industry turbulence has intensified regulatory scrutiny notably regarding deposit compositions such as levels of uninsured deposits—which comprised approximately one-third of non-brokered deposits at end-2025—and expectations around liquidity coverage ratios requiring detailed reporting and contingency planning from regional banks like Equity Bancshares [S9][S28].

The company faces regular legal proceedings typical of banking operations including potential class actions related to lending practices such as overdraft fee assessments or interest calculations posing financial liability threats should unfavorable judgments arise [S4][S12]. Enhanced anti-money laundering compliance burdens and evolving Consumer Financial Protection Bureau regulations add complexity and cost burdens impacting operating margins indirectly via increased personnel and systems investments required for adherence [S29].

Technological innovation demands simultaneously heighten cybersecurity risks including potential breaches impacting customer data confidentiality—mandating sustained expenditures on protection frameworks yet introducing risk exposure that can affect reputation adversely if incidents occur [S13][S20].

Operational dependence on long-tenured management team poses retention risks; unexpected key personnel departures could disrupt relationship-driven business models dependent on local market knowledge undermining growth execution capability temporarily [S14].

Assessment of Market Position and Competitive Advantages

Equity Bancshares sustains competitive differentiation primarily through deep-rooted relationships within midwestern community banking segments across its four-state footprint fostering strong customer loyalty based on personalized service models emphasizing ethical standards [S19].

Its asset-based lending specialization provides resilience via collateral-backed exposures though simultaneously limits rapid scaling opportunities due to geographic concentration constraints inherent to localized banking models unable to tap larger national markets easily without costly expansion or acquisition strategies which carry integration risks themselves [S19].

Heightened competition from technologically advanced national banks and fintech challengers necessitates continuous innovation balancing cost constraints typical among community banks lacking scale advantages found among larger players with significant IT budgets—a challenge identified explicitly as limiting near term efficiency improvement potentials while safeguarding quality service delivery standards critical for client retention [S19][S9].

Future Performance Indicators to Monitor

Stakeholders should closely watch several key metrics indicative of recovery or emerging risks post-FY2025 earnings decline:

- Quarterly net income trajectory: evidence of sustained rebound versus episodic normalization will guide confidence levels.

- Loan portfolio credit quality: monitor delinquency rates, provision expense trends reflecting real-time credit risk evolution aligned with economic conditions impact.

- Deposit growth patterns: inflows versus outflows signal liquidity stability affecting funding cost structures.

- Digital transformation progress: cost optimization achievements through technology adoption impacting expense ratio improvements without erosive customer experience effects.

- Regulatory developments: changes especially relating to liquidity requirements or consumer protection rules influencing compliance expenses or operational flexibility.

- Legal proceeding outcomes influencing contingent liabilities or reputational standing.

Maintaining vigilance across these areas offers insights into whether management’s strategic emphasis on asset-secured lending combined with prudent capital deployment can translate into renewed sustainable profitability amid ongoing competitive pressures and macroeconomic variability.

Disclaimer: This analysis is based solely on publicly available information as referenced without forward-looking projections beyond reported guidance or explicit company disclosures. It presents no investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments