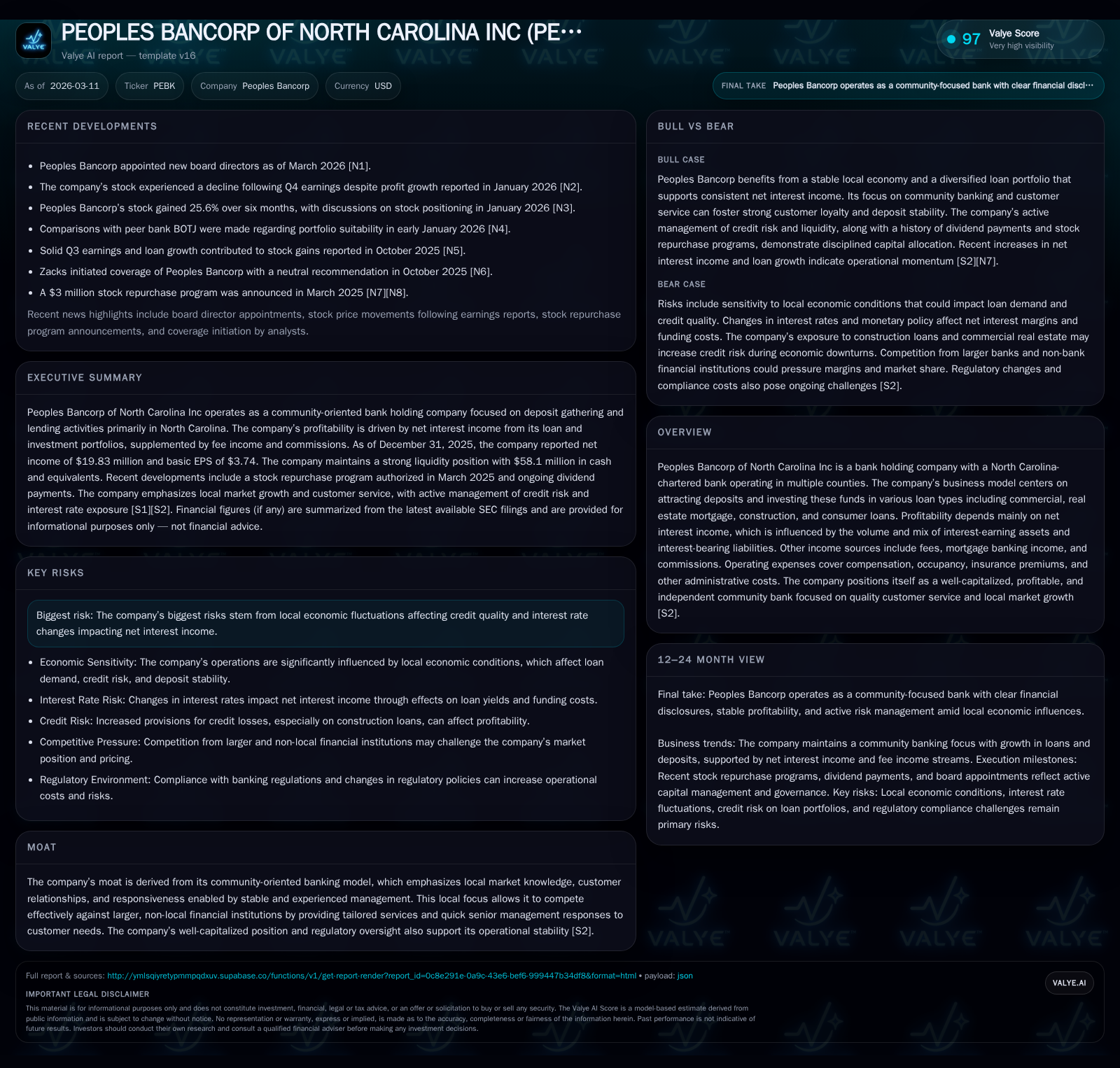

Peoples Bancorp’s Earnings Momentum Fuels Community Banking Resilience

Recent robust net income growth at Peoples Bancorp highlights the strength of its local banking strategy amid evolving regional economic conditions.

Peoples Bancorp of North Carolina has demonstrated sustained earnings growth, propelled primarily by expansion in net interest income and loan portfolios concentrated in commercial and real estate sectors. Its community-centric business model creates a competitive moat through deep local ties and responsive management. Capital allocation remains disciplined with steady dividend payments and prudent buyback activity tapering in favor of reinvestment. Investors should monitor loan growth trends, credit quality signals, and evolving interest rate impacts in assessing future performance under shifting macroeconomic conditions.

Historical Financial Trajectory and Earnings Drivers

Peoples Bancorp of North Carolina has showcased an encouraging financial progression over the past four fiscal years, culminating in a net income surge of 21.3% to $19.83 million in FY2025 from $16.35 million in FY2024 [F1]. This acceleration follows a remarkable recovery trajectory post-2022, where net income was lower at $4.15 million recovering through FY2023 and FY2024. Operating cash flow has held steady within the $20-$23 million range throughout this period, underpinning strong internal liquidity [F1]. Capital expenditures fluctuated moderately but remain a small fraction of cash inflows indicating efficient investment strategy. Equity grew materially from $105.2 million at end-FY2022 to $157.1 million at end-FY2025, improving capital precision aligned with earnings gains.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 20 | 21 | 1 | +21.3% |

| 2024 | 16 | 21 | 1 | +375.5% |

| 2023 | 3 | 23 | 2 | -17.1% |

| 2022 | 4 | 23 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 5 | 0 | 20 |

| 2024 | 5 | 1998000 | 20 |

| 2023 | 5 | 1997000 | 21 |

| 2022 | 5 | 710000 | 18 |

Source: SEC companyfacts cache [F1].

Net income improvements reflect solid execution on net interest income expansion driven by rising interest rate environments earlier during the period as well as strategic loan growth fostering asset yield enhancement. Notably absent were buybacks during FY2025 following share repurchase programs that featured prominently in prior years but were suspended or expired recently.

Localized Business Model and Competitive Moat

Peoples Bancorp’s operational ethos is firmly anchored in its community-oriented banking model which nurtures lasting customer relationships built on local market expertise and responsiveness [S2]. Its deposit franchise demonstrates significant stability accentuated by core deposits comprising roughly90% of total deposits—primarily demand deposits and savings accounts under $250k—providing a reliable low-cost funding source essential for margin sustenance [S4][S12]. The company's senior management maintains close interaction with clients and swift decision-making capabilities uncommon among larger regional or national banks mitigating customer attrition risk.

The robust capital foundation governed under Basel III accords further supports operational resilience while regulatory compliance ensures sustainability amid evolving banking supervision landscapes [S21]. This localized approach forms the basis of competitive differentiation versus larger non-local financial institutions whose scale often dilutes service-level customization.

Loan Portfolio Composition and Risk Considerations

The loan book composition is diversified yet significantly weighted toward commercial loans (including commercial mortgages), followed by residential mortgage loans and construction loans coupled with consumer lending segments [S2][S23][S24]. At September end-2025 snapshots reveal approximately $721.6 million in commercial mortgage loans — itself largely secured by commercial properties — along with substantial residential mortgage exposure totaling near $132.8 million and home equity lines around $120.7 million [S23]. Construction and land development loans stood near $129.2 million.

Credit quality metrics are closely monitored given inherent sensitivities to local economic cycles impacting borrower repayment capacity through employment fluctuations or SME performance stresses [S2][S17]. Non-performing assets remained low relative to overall asset size (0.28%) across recent reporting dates suggesting effective underwriting discipline [S11][S13]. The allowance for credit losses scaled modestly upward reflecting incremental loan growth yet maintaining coverage ratios near historical norms (0.86%) with additional provisions for off-balance sheet unfunded commitments [S17][S23], reinforcing prudent risk provisioning.

Key present-day risk vectors hinge upon localized economic downturns undermining credit performance and interest rate volatility influencing margin compression via funding cost variability.

Recent Operating Performance and Net Interest Income Trends

Q4 FY2025 results released January revealed continued net interest margin resiliency albeit amid a tightening Federal Reserve rate environment earlier in the cycle subsequently eased down from mid-2024 levels resulting in compressed yields [N1][S2][S4]. The predominance of core deposits as funding reduces volatility risk while the company's diligent asset-liability management committee (ALCO) actively manages repricing gaps mitigating earning sensitivity nuances [S12][S20].

Rate sensitive assets exceed comparable liabilities by an excess of half a billion dollars supporting positive spread generation despite downward pressures on prime-indexed variable rate loans representing a material portion (~$174.8 million) of the portfolio.

Additional revenue streams from fees tied to mortgage banking activities and commissions supplement core net interest revenue while operating expense discipline containing compensation costs maintain bottom-line absorption efficiency.

Capital Allocation: Dividends, Buybacks, and Cash Flow Efficiency

Peoples Bancorp reported an approximate return on equity of 12.6% for FY2025 calculated via year-end net income versus average equity reflecting deft capital utilization [F1]. Free cash flow after modest capex expenditures approximated nearly $20 million sustaining robust dividend distributions totaling roughly $5.25 million consistent with prior years’ payouts revealing commitment to shareholder returns without aggressive leverage or payout ratio outstripping earnings [F1][S28].

While share repurchase activity tapered off completely during FY2025 following prior authorized plans executed through FY2024—this suggests a tactical capital retention preference possibly linked to macro uncertainties amid ongoing Fed policy recalibrations highlighting prudence.

Collectively these allocations align with bank holding company best practices balancing reinvestment capacity alongside shareholder remuneration while upholding regulatory capital buffers.

Management Changes and Governance Impact

The company bolstered governance quality with recent board director additions announced March signaling enhanced oversight capabilities including specialized attention toward cybersecurity risks—a critical component within today's banking risk landscape as managed by the Chief Operations Officer and technology leadership teams who report monthly to the Board’s oversight committees [N2][S1].

This governance focus extends into regular reviews of information security posture ensuring enterprise resilience against cyber threats which aligns with sector best practices enhancing operational reliability.

Such governance advancements support strategic agility amidst digital transformation trends permeating community banking sectors increasingly reliant on secure technological infrastructures.

Outlook: Growth Opportunities and Macroeconomic Constraints

Management’s outlook underscores expectations for continued moderate growth fueled by expanding lending demand within its geographic footprint punctuated by investments into contiguous North Carolina markets while remaining cautious on acquisition-driven expansion which presently is not deemed essential for satisfactory returns based on current market dynamics [S2][S18].

Economic stability locally has tempered credit stress though continued exposure to Federal Reserve interest rate maneuvers presents margin pressure risks requiring vigilant balance sheet positioning particularly given tightening monetary conditions earlier transitioning into easing phases during late-2025 [S2][N1].

Local small business credit performance remains pivotal as this segment often acts as economic activity barometer influencing allowance levels reflecting cyclical sensitivity highlighting investor watchpoints.

Key Milestones and Factors to Monitor

Explicit guidance disclosures are currently limited; however critical metrics warranting close monitoring include quarterly loan origination trends evidencing sustainable portfolio growth velocity; shifts in deposit structure potentially impacting cost of funds; changes to allowance for credit losses signaling emerging credit quality developments; regulatory capital ratios reflective of solvency health; dividend policy adjustments reflecting profitability trajectory; alongside senior leadership continuity or alterations influencing strategic direction [N1][N2][S2].

These measures collectively form tangible barometers for assessing Peoples Bancorp’s trajectory navigating prevailing macroeconomic uncertainties balanced against inherent benefits from its entrenched community-focused franchise.

This analysis incorporates publicly available financial data as filed with regulatory agencies combined with recent market commentary without speculative forecasts or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments