Crown Equity Holdings Navigates Declining Revenue and Liquidity Challenges Amid Strategic Shift

CRWE’s revenue dropped sharply in FY2025 as it refocuses on consulting and online media publishing, facing liquidity constraints and ongoing losses.

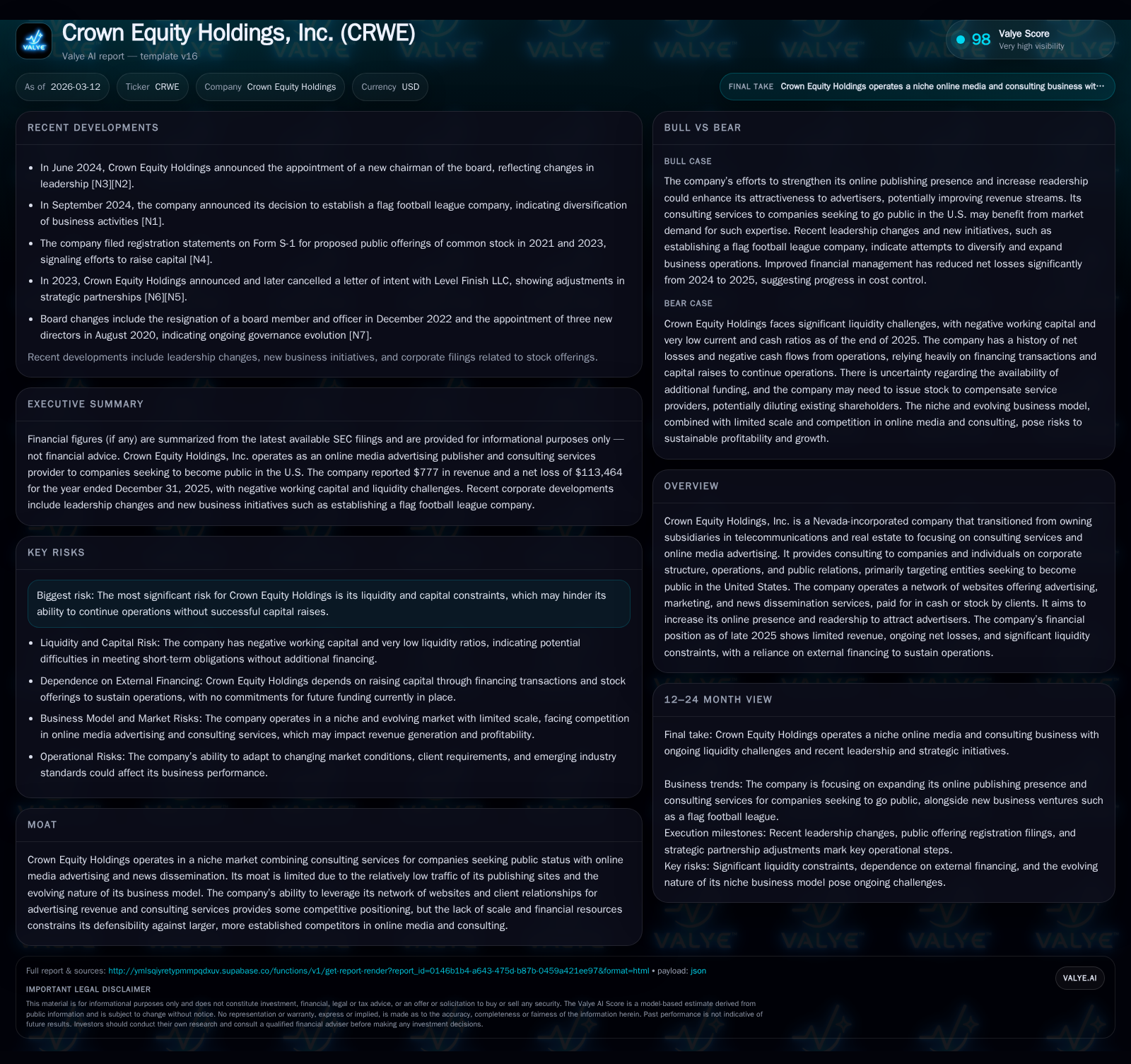

Crown Equity Holdings, Inc. reported a 46.2% revenue decline to $777 in FY2025 alongside continued net losses of $113,464 despite lower operating expenses. The company has transitioned from legacy telecom and real estate subsidiaries to consulting services and online media advertising through a network of websites with low to medium traffic. Liquidity remains tight with negative working capital exceeding $314k and dependence on related-party financing. Profitability challenges persist due to operating expense levels relative to revenue and limited scale in digital publishing. Future growth depends on expanding web presence, advertiser engagement, and securing additional capital to fund operations.

Revenue Decline Reflects Business Model Transition

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 777 | 0 | -34604 | -71831 | -46.2% | +96.9% |

| 2024 | 1443 | -4 | -52373 | -1320806 | +1188.4% | -373.9% |

| 2023 | 112 | -1 | -80281 | -771787 | -96.2% | -6.0% |

| 2022 | 2935 | -1 | -89366 | -478577 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 36.1 |

| 2024 | 1155.6 |

| 2023 | 53.4 |

| 2022 | 53.6 |

Source: SEC companyfacts cache [F1].

Crown Equity Holdings experienced a notable decline in revenues from $1,443 in FY2024 to $777 in FY2025, a decrease of 46.2% ([F1], [S1]). This contraction follows the company's strategic shift away from its previously owned telecommunications and real estate subsidiaries—sold by the end of 2017—toward providing consulting services and operating online media publishing platforms.

The nascent revenue streams are influenced by limited traffic across its portfolio of publishing websites that generate advertising income paid partly in cash or client equity ([S4], [S5]). The modest scale of site visitation constrains the volume and quality of advertising contracts achievable.

Dual Focus on Consulting Services and Online Media

Crown Equity offers consulting targeted at domestic and international companies aiming to become public entities in the U.S., including corporate structure advisory, operational management assistance, financial reporting compliance support, and public relations ([S4]). Concurrently, the company maintains multiple websites delivering marketing content, news dissemination, and PR services primarily for publicly and privately held companies.

This combined approach attempts to leverage consulting credibility alongside media-driven marketing reach. However, most online properties currently attract only light-to-medium traffic volumes which limit monetization potential ([S5]).

Cash Flow Pressures Amid Tight Liquidity

At fiscal year-end 2025, Crown Equity's liquidity position was strained with just $1,862 cash on hand plus $410 in marketable securities ([F1], [S6]). Current assets stood at $8,572 against current liabilities totaling $322,634 resulting in a deeply negative working capital position of roughly -$314k ([F1], [S6]).

Operating cash flow used was -$34,604 during FY2025 compared with -$52,373 in FY2024 ([F1], [S8]). Financing activities generated net proceeds of $33,018 mainly through related-party borrowings and sale of common stock (11,000 shares) ([F1], [S6]). No formal agreements exist for ongoing funding from insiders or third parties.

Management acknowledges the need for continual capital acquisition to sustain operations including compliance with SEC reporting requirements ([S6]).

Profitability Remains Elusive Despite Expense Reduction

Operating loss improved markedly to -$71,831 in FY2025 compared to much larger prior year losses largely due to elimination of significant non-cash amortization charges ([F1], [S1]). Nonetheless, the company remains unprofitable.

Net loss narrowed substantially to -$113,464 from over $3.7 million the previous year ([F1], [S1]). This improvement primarily reflects reduced one-time charges rather than sustained operational profitability.

With revenues under $800 against operating expenses near $73k for the same period ([F1], [S1]), fixed cost absorption challenges persist. The business lacks scale typical of more mature digital media or consulting firms.

Operating Costs Outpace Revenues

General operating expenses approximated $72K versus scant sales reported during FY2025 ([F1], [S1]), highlighting a significant cost-to-income imbalance that limits margin expansion.

While shedding legacy amortization costs contributed to expense reductions year-over-year, core costs related to website development support by software/hardware technicians remain steady ([S15]).

Without meaningful growth or pricing power gains in consulting or advertising segments, profitability improvements are unlikely without operational scaling or cost rationalization.

Growth Strategy Centered on Online Presence Expansion

The company focuses on strengthening its competitive position through community-targeted news publishing initiatives aimed at increasing readership ([S5]). Enhanced audience engagement is sought both for direct monetization and as leverage when attracting advertisers.

However, modest traffic levels cap near-term advertising revenue growth potential. The fragmented digital media landscape combined with established competitors possessing greater scale complicates Crown Equity's growth trajectory.

Success depends heavily on effective SEO campaigns and sustained content quality—areas potentially constrained by limited resources.

Capital Deployment and Returns Profile

Capital expenditures are minimal historically with last known figures dating back several years suggesting lean operational focus ([F1]). Return on equity is negative reflecting ongoing losses relative to shareholder deficit exceeding $314k at year-end 2025 ([F1]).

No dividends or share repurchase programs have been declared recently; capital formation relies predominantly on sporadic related-party loans and small equity offerings without formal underwriting commitments ([F1], [S6], [S8]).

Risks Centered Around Liquidity and Market Positioning

Key risks include persistent negative cash flows requiring external financing for survival amid uncertain growth prospects within niche consulting and digital publishing markets ([S7], [S9], [S12]). Regulatory compliance costs add further pressure.

Market fluctuations affecting investor sentiment could impact stock price given OTC Pink listing status. The lack of scale limits competitive moats while evolving client needs pose challenges for sustaining consulting relevance.

Outlook Considerations

Milestones warranting close observation include:

- Evidence of quarterly increases in web traffic indicating successful audience expansion;

- New client acquisitions or contract expansions within consulting contributing recurring revenues;

- Material financing arrangements improving liquidity outlook;

- Cost containment initiatives balancing service delivery with expense control;

- Progress on regulatory compliance reducing administrative burdens.

Absent such developments Crown Equity faces a challenging path where operational viability depends heavily on external capital availability combined with incremental growth successes.

Disclaimer: This report is based exclusively on publicly filed documents as of early 2026. It does not constitute investment advice or endorsement. All financial figures are sourced strictly from Company filings without extrapolation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments