Community West Bancshares Posts Turnaround After Strategic Merger Boost

The company's net income surged nearly 400% in 2025 following its transformative 2024 merger, reshaping its growth trajectory and capital framework.

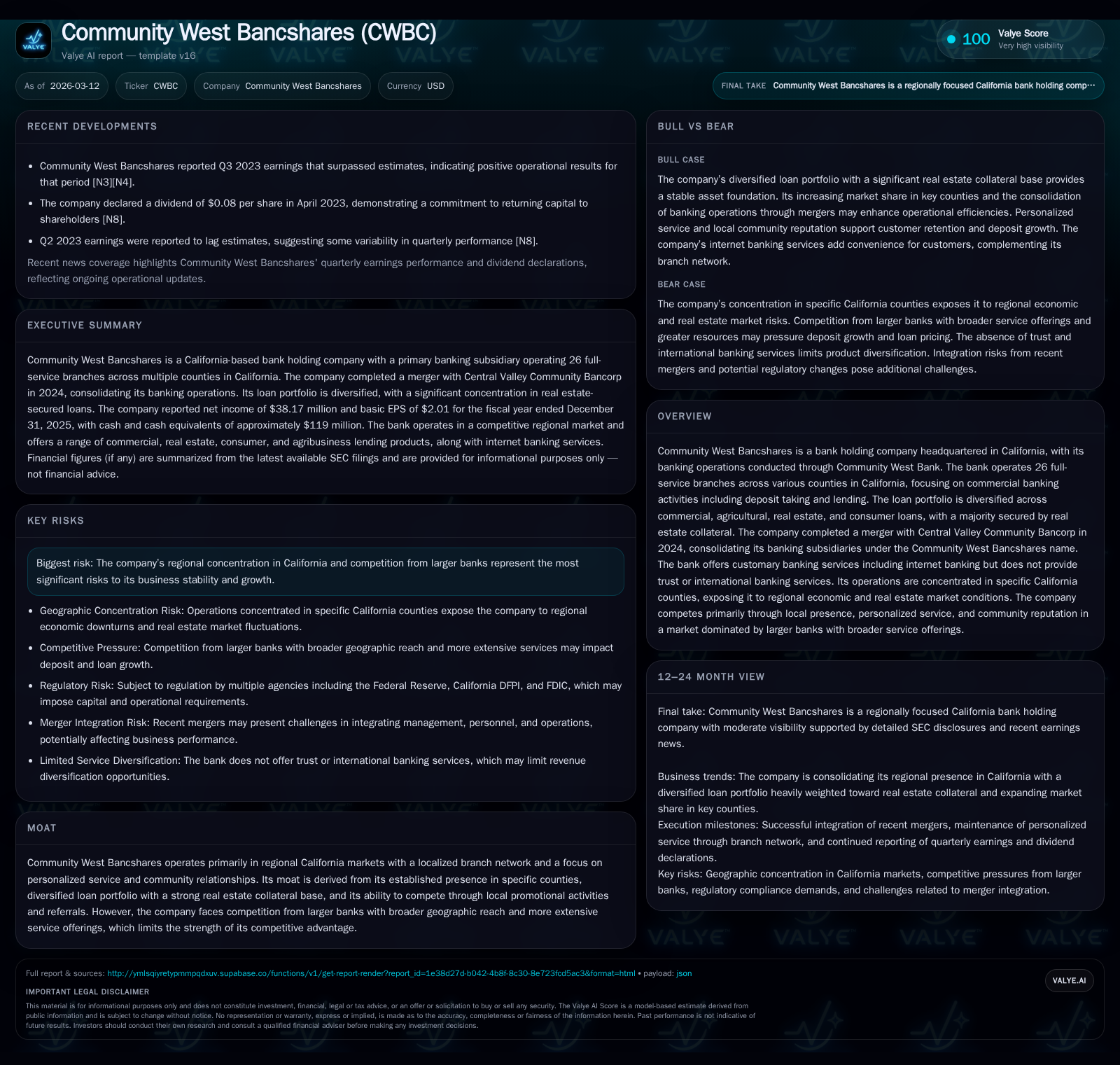

Community West Bancshares delivered an impressive financial rebound in fiscal 2025 driven primarily by synergies from its 2024 merger with Central Valley Community Bancorp. Net income climbed to $38.2 million, a near fourfold increase year-over-year, supported by expanded market share and improved operational efficiencies. The loan portfolio remains heavily weighted toward real estate-secured credit across California counties, presenting both growth opportunity and regional concentration risk. Capital strategy emphasized consistent dividends with modest share buybacks amid strong free cash flow generation. Looking forward, leadership transitions and competitive pressures from larger banks constitute key facets to monitor.

Returns Surge Driven by Merger Synergies and Market Focus

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 38 | 46 | 3 | +397.9% |

| 2024 | 8 | 22 | 5 | -70.0% |

| 2023 | 26 | 28 | 10 | -4.2% |

| 2022 | 27 | 24 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 14 | 0 | 44 |

| 2024 | 14 | 0 | 17 |

| 2023 | 7 | 0 | 18 |

| 2022 | 38 | 7 | 24 |

Source: SEC companyfacts cache [F1].

Community West Bancshares experienced a dramatic turnaround in profitability during fiscal year 2025 following the completion of its merger with Central Valley Community Bancorp in 2024. Net income leapt from $7.7 million in FY2024 to $38.2 million in FY2025, reflecting a sizable increase of about 398% [F1][S4]. This growth was largely fueled by operational synergies realized post-merger as well as expanded footprint and customer base in key California counties.

The consolidation under one holding company enhanced scale advantages and improved efficiency, allowing the bank to leverage its broader commercial banking platform more effectively. While these factors boosted financial results, it also concentrated CWBC’s earnings exposure geographically within California’s regional markets, particularly within counties vulnerable to local real estate cycles [S4]. Despite this concentration risk, the company maintained solid underwriting standards supported by predominantly secured loan assets.

Loan Portfolio Composition and Real Estate Collateral Concentration

At the close of 2025, CWBC carried a net loan portfolio balance of approximately $2.54 billion [F1], diversified across commercial & industrial (C&I), agricultural loans, real estate (both owner-occupied and investment), and consumer lending segments [S4][S7]. Lending remains heavily anchored in real estate-secured assets—about 76% of the total loan book—covering construction loans, commercial real estate (CRE), agricultural real estate, home equity lines of credit (HELOCs), and residential mortgage exposures.

This portfolio composition underscores management’s focus on lower-risk secured lending collateralized chiefly by various forms of tangible real estate [S7]. The bank balances traditional commercial banking with agribusiness sector exposure relevant to its California footprint. Notably absent are international or trust banking lines that might diversify fee income but fall outside CWBC’s localized community banking model.

From a sector perspective, while CRE and owner-occupied real estate loans can offer stable cash flows if underwritten prudently, their performance is highly correlated with regional property valuations and economic conditions—a critical risk factor given CWBC’s market concentration [S4]. Portfolio monitoring remains essential amid California’s evolving economic landscape.

Competitive Positioning in Key California Markets

Community West Bancshares operates through a network of 26 full-service branches concentrated primarily in Fresno, Madera, San Joaquin, Tulare counties and several others within California [S1][S4]. According to FDIC deposit data as of June 30, 2025, the company’s combined deposit market share in Fresno, Madera, San Joaquin, and Tulare counties rose from approximately 4.10% in the prior year to around 4.41% [S4], exhibiting modest gains indicative of effective customer retention and incremental acquisition.

Competition remains intense from major national and regional banks with significantly larger footprints that offer more diversified products including trust services and international banking capabilities [S4]. In contrast, CWBC leverages its strong local presence with personalized customer service, community relationships cultivated through officers’ outreach efforts, targeted promotion campaigns focused on local businesses and referrals from shareholders [S4]. These localized dynamics form the backbone of its competitive moat but limit scalability beyond core markets without further expansion or product diversification.

Operating Cash Flow Growth Outpaces Capex Reduction

Cash flow metrics reveal robust liquidity generation coinciding with the firm’s growth trajectory. Operating cash flow (CFO) nearly doubled year-over-year from $22.2 million in FY2024 to $46.1 million in FY2025 [F1]. Simultaneously, capital expenditures were reduced sharply by over half—from roughly $5 million down to about $2.5 million—reflecting disciplined spending likely aimed at optimizing branch operations post-merger integration [F1].

This dynamic resulted in an estimated free cash flow (FCF) of approximately $43.6 million for FY2025 [F1], providing ample internal funding for dividends and strategic initiatives without reliance on external capital sources.

Strong CFO alongside controlled capex enhances financial flexibility crucial for managing working capital needs in a regional banking context where technological investments must be balanced against margin pressures.

Capital Structure, Dividend Policy, and Share Repurchases

At December 31, 2025, Community West Bancshares reported shareholders’ equity totaling about $410 million—a substantial increase from $363 million at the end of FY2024 reflecting retained earnings accumulation following strong profitability [F1]. Using these figures alongside net income yields an approximate return on equity (ROE) near 9.3%, consistent with efficiency expectations for mid-sized regional banks focusing on conservative growth [F1].

Dividend distributions have remained consistently around $14 million annually for two consecutive years post-merger despite surging earnings—a policy indicating management’s commitment to returning steady income while supporting organic balance sheet growth [F1].

Share repurchases are conducted selectively at modest levels; FY2025 buybacks totaled approximately $151 thousand versus even lower activity prior years [F1]. This restrained repurchase strategy suggests prioritization of capital preservation amid ongoing integration activities rather than aggressive share price support.

Management Changes and Organizational Outlook

A notable organizational development occurred early 2026 when COO Blaine C. Lauhon announced his planned retirement effective December 31, 2026 [S3]. This marks an important succession event during a critical phase as the company continues post-merger integration efforts and strategic execution.

Stability within senior management will be vital for sustaining momentum built since consolidation given his role overseeing day-to-day operations including branch network efficiency and lending operations—areas central to CWBC’s value proposition.

Potential shifts under new leadership could introduce fresh perspectives or recalibrate priorities especially around geographic expansion or product innovation areas where CWBC currently lags larger competitors.

What to Watch: Future Opportunities and Geographic Constraints

Looking ahead analysts should monitor several key variables shaping Community West Bancshares' trajectory:

- Branch Network Optimization: Management’s ongoing decisions regarding branch openings or consolidations will impact cost structure and customer accessibility within saturated California markets [S4].

- Competitive Responses: Larger banks’ expansive services (trusts, international banking) pose challenges; understanding how CWBC enhances referral partnerships or develops indirect offerings will be instructive [S4].

- Credit Quality Trends: Vigilance over loan portfolio performance particularly CRE and agricultural segments amid fluctuating property values is crucial due to inherent regional concentration risks [S4].

- Capital Allocation Strategy: Balancing dividends against reinvestments or opportunistic acquisitions remains a delicate tradeoff given current payout steadiness but limited buybacks observed [F1].

- Leadership Transition Impact: Executing COO succession smoothly will be essential to maintain operational continuity during strategic evolution phases [S3].

Overall future growth appears tethered strongly to regional economic health specifically California’s real estate markets alongside CWBC’s ability to sustain differentiation via community-centric service models amidst intensifying competition.

This analysis is based solely on publicly available company filings and documented financial data as of March 12, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments