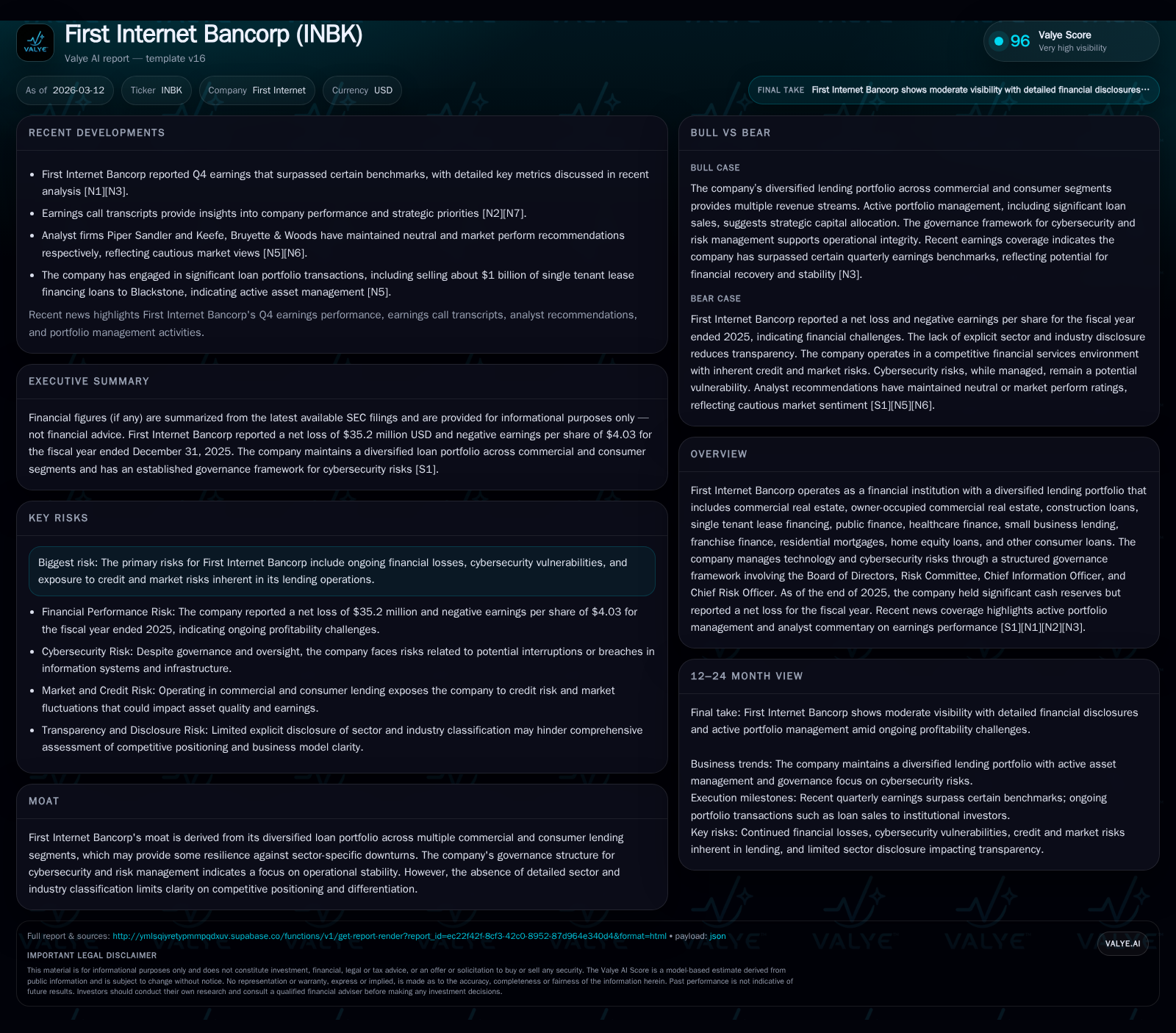

First Internet Bancorp Faces Earnings Pressure Despite Diversified Lending and Strong Cash Position

The company's diversified loan portfolio provides resilience, but recent net losses and slowing cash flows highlight operational challenges.

First Internet Bancorp (INBK) operates a broad loan portfolio across commercial and consumer segments, which historically supported steady income and cash flow growth. However, in the fiscal year 2025, the bank reported a significant net loss reversing prior profitability trends, accompanied by sharply reduced operating cash flow. Ample cash reserves and a conservative capital base underline financial stability, but ongoing and rising credit risks along with cybersecurity governance remain key vulnerabilities. Future growth depends on effective portfolio management and market dynamics affecting loan performance and interest rates.

Overview

First Internet Bancorp (INBK) presents a business model built on diversified lending spread across multiple commercial real estate categories, healthcare financing, small business loans, franchises, residential mortgages including home equity loans, and various consumer credit products [S1]. Such diversification potentially cushions the bank against sector-specific downturns but does not immunize it entirely from macroeconomic headwinds or credit deterioration.

Governance around technology and cybersecurity is robust; the Board of Directors receives quarterly updates from the Chief Information Officer and Information Security Officer. The Risk Committee holds dedicated responsibility for ongoing oversight of cyber risks. This layered governance model aligns with industry best practices aiming to prevent operational disruptions [S1].

Historical Financial Performance

From a financial perspective, INBK demonstrated steady profitability improvements through early 2020s but encountered material setbacks in 2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -35 | 3 | 1 | -239.1% |

| 2024 | 25 | 13 | 3 | +200.3% |

| 2023 | 8 | 12 | 5 | -76.3% |

| 2022 | 36 | 83 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 2 | 1 | 2 |

| 2024 | 2 | 0 | 10 |

| 2023 | 2 | 9 | 6 |

| 2022 | 2 | 28 | 65 |

Source: SEC companyfacts cache [F1].

(Source: [F1])

Net income swung sharply negative in FY25 reflecting increased loan loss provisions or mark-to-market pressures not disclosed explicitly but inferred from public filings [S1][N3]. Operating cash flow similarly contracted dramatically from over $82 million in FY22 to just $3.4 million by FY25.

Capital expenditures declined steadily indicating cautious reinvestment amid uncertain earnings.

Dividend payments have been relatively steady despite profitability volatility—suggesting board confidence in shareholder distributions or signaling strategic priorities for capital return.

Share repurchases plummeted after FY23’s high activity level but modest buybacks resumed in FY25.

Business Segments and Loan Portfolio Dynamics

INBK's diversified loan book spreads credit risk but also demands extensive monitoring:

- Commercial Real Estate: Core exposure includes both investor-owned and owner-occupied properties; this sector typically faces volume sensitivity to interest rate shifts.

- Construction Loans: Tend to carry higher risk given project completion uncertainty.

- Single Tenant Lease Financing & Public Finance: Specialized niches requiring careful underwriting.

- Healthcare Finance: Stable demand sector but sensitive to regulatory changes.

- Small Business & Franchise Lending: Highly dependent on regional economic health.

- Residential Mortgages & Home Equity Loans: Consumer credit cycle sensitivity.

Given the varied product mix highlighted in filings [S6][S8], risk grading has become increasingly vital as economic conditions tighten. Delinquencies and nonperforming assets may rise disproportionately in cyclical exposures like construction or small business segments.

Capital Structure and Liquidity

At December-end 2025 the bank held approximately $457 million of cash and equivalents [F1], providing ample liquidity buffer amid earnings pressure. Equity stood at about $360 million with no drastic decline compared to prior years indicating moderate erosion due to losses but manageable capital position overall [F1].

Debt issuance mainly consists of subordinated notes supporting regulatory capital requirements; details from Q3 filings show investment-grade municipal bonds and mortgage-backed securities underpin risk asset composition [S5][S7].

Liquidity ratios remain consistent with historical practice emphasizing conservative funding profiles suitable for a mid-sized institution focused on asset quality preservation.

Returns and Capital Allocation Considerations

Return on equity dipped into negative territory around -9.8% for FY25 due to net losses versus stable equity capital base [F1]. Cash flow generation sharply reduced yet remained positive after capex — free cash flow approximated at $2.2 million indicating very limited surplus available for growth reinvestment or discretionary distributions beyond dividends.

Dividend payout continuity despite earnings pressure signals management intent to maintain investor confidence but may be subject to revision if losses persist or regulatory scrutiny intensifies [F1][N2].

Buybacks sharply curtailed from previous years; resumption at low levels likely reflects opportunistic share price support rather than primary capital return strategy during a challenging earnings environment.

Recent Operational Highlights and Outlook

Earnings releases indicated that Q4 results slightly outperformed analyst estimates driven by disciplined portfolio management despite broad macroeconomic challenges [N3]. Management highlighted active risk mitigation measures such as tightening underwriting standards and selective lending pauses within more volatile sectors [N2][N1].

Cybersecurity remains an elevated priority area with formalized Board oversight mechanisms reaffirmed in recent annual disclosures [S1], appropriate given increasing regulatory expectations for financial institutions handling sensitive client data.

Future growth prospects hinge on several factors:

- Improvement or stabilization of credit quality across diverse loan segments remains critical.

- Interest rate trajectories will directly impact net interest margins given floating-rate loan composition.

- Market competition dynamics among digitally focused banks could pressure fee income streams.

Absent explicit forward guidance from filings or management commentary beyond cautionary language [N2][S1], key performance indicators to monitor include quarterly provisioning trends, nonperforming loan ratios by segment, margin pressures reported in upcoming quarters and actual versus expected credit losses.

Risks Summary

Apart from financial volatility evident in recent annual results:

- Credit risk exposure intensified by recessionary pressures or sector-specific downturns could further impair loan portfolios.

- Cybersecurity threats require ongoing vigilance; breaches could disrupt operations posing reputational damage beyond immediate costs.[S4]

- Regulatory shifts especially impacting consumer lending or capital requirements present additional uncertainties.

- Low free cash flow limits flexibility during periods of operational stress or heightened capital needs.

Concluding Thoughts

First Internet Bancorp’s diversified lending approach offers theoretical resilience that has helped sustain intermittent earnings amid fintech competition and economic cycles. Nonetheless the steep swing into net losses coupled with markedly lower operating cash flows underscore tangible challenges facing INBK entering calendar year 2026. Their strong liquidity position along with prudent capital structure provides operational runway while active portfolio management aims to curb risk buildup discovered during recent periods of economic strain.

Monitoring of detailed segment-level asset performance along with updated disclosures following each quarter will be essential for better understanding trajectory toward restoring profitability.

This analysis is prepared solely for informational purposes without investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments