Exodus Movement Navigates Modest Revenue Growth Amid Profitability and Regulatory Challenges

In 2025, Exodus Movement advanced its digital asset platform offerings while facing a sharp decline in profitability and increased cash outflows, alongside regulatory settlements.

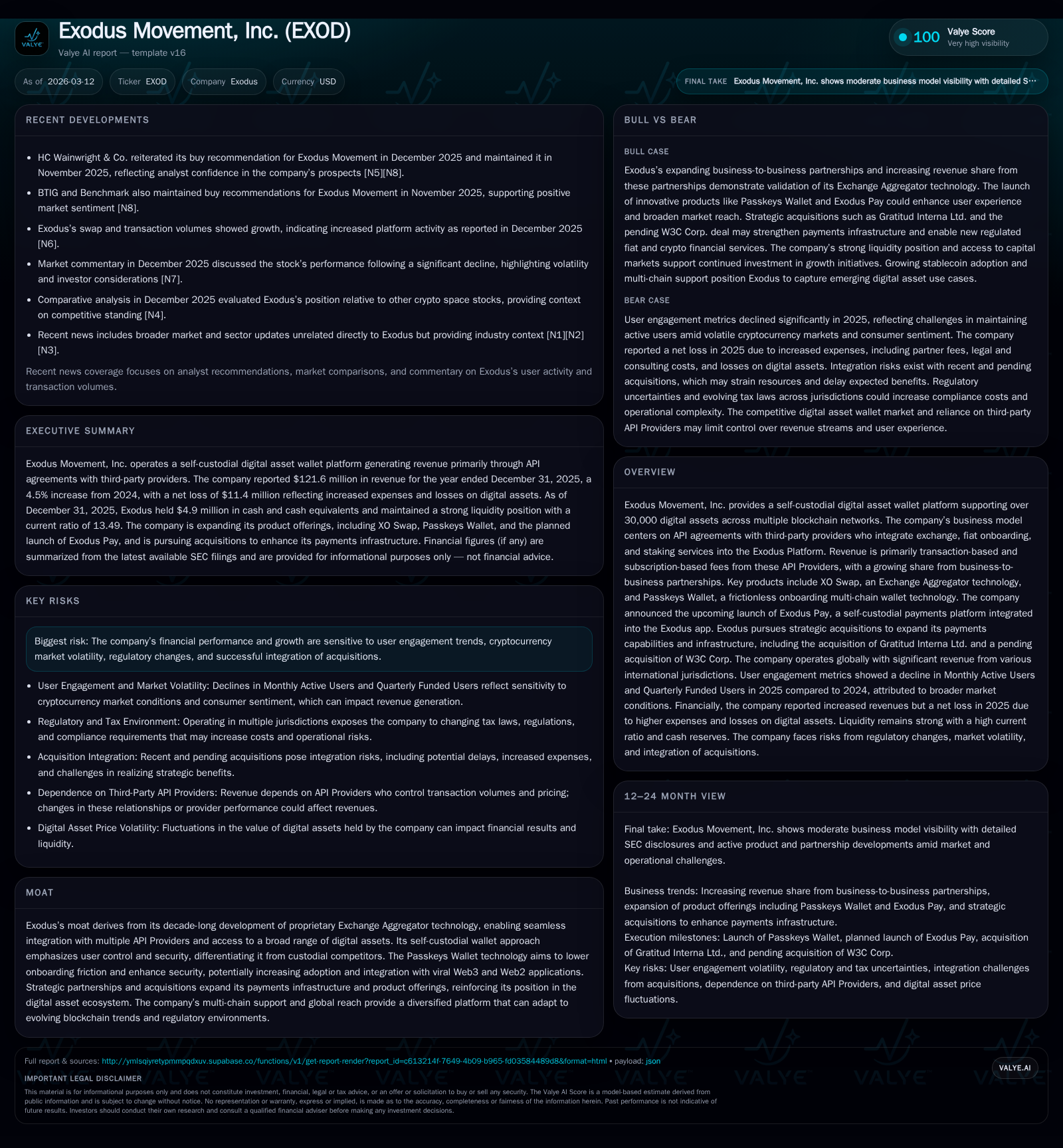

Exodus Movement, Inc. expanded its platform capabilities including multi-chain wallet technology and API integrations during 2025, achieving modest revenue growth driven by exchange aggregation fees. The company reported a net loss of $11.35 million amid impairments on digital assets and elevated operating costs. Operating cash outflows nearly doubled year-over-year, reflecting ongoing investments and increased losses on digital assets. Regulatory compliance remains a key focus after settling an OFAC penalty related to prior inadvertent access by users in sanctioned regions. Despite the challenges, Exodus maintains strong liquidity with a current ratio above 13x and continues strategic capital allocation through share repurchases. Future growth depends on successful product deployments such as Exodus Pay and navigating evolving regulatory landscapes.

Business Overview and Historical Performance

Exodus Movement, Inc. operates a self-custodial digital asset wallet platform supporting over 30,000 tokens across multiple blockchains, leveraging proprietary Exchange Aggregator technology that integrates third-party API Providers offering exchange services, fiat onboarding, and staking functionalities [S1].

For the fiscal year ended December 31, 2025, the company reported revenues of approximately $121.6 million, a modest increase of about 4.5% from $116.3 million in 2024 [F1][S11]. This growth was primarily driven by exchange aggregation fees which accounted for roughly 91% of total revenues.

However, profitability deteriorated markedly with a net loss of $11.35 million in 2025 compared to net income of $112.96 million in the prior year [F1]. The reversal was largely attributable to impairments related to digital assets held at fair value alongside increased operating expenses focused on growth initiatives.

Operating cash flows aligned with this trend, worsening from an outflow of around $12.0 million in FY24 to nearly $25.6 million negative cash flow in FY25 [F1][S8]. Capital expenditures remained modest at approximately $0.27 million annually.

Despite these challenges, Exodus maintained strong liquidity at year-end with current assets near $99.3 million versus current liabilities of $7.36 million, resulting in a current ratio near 13.5x indicating ample short-term financial flexibility [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -11 | -26 | 267000 | -110.1% |

| 2024 | 113 | -12 | 273000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 15 | -26 | -4.6 |

| 2024 | 5 | -12 | 43.9 |

Source: SEC companyfacts cache [F1].

Table: Key financial metrics illustrating revenue growth alongside significant earnings decline and cash flow deterioration.

Business Model and Product Innovations

Exodus's revenue generation is primarily based on fees earned from API Providers integrated into its wallet platform through transaction-based and subscription-based contracts covering digital asset exchanges, fiat onboarding, and staking services [S1][S11]. The XO Swap partnership extends this model by embedding Exchange Aggregator technology into other wallets such as Ledger Live™, thereby expanding market reach.

In July 2024, Exodus launched Passkeys Wallet—a frictionless multi-chain self-custody wallet solution enabling users to create wallets within dApps using device-native authentication without seed phrases or additional software installations—enhancing security and user experience across supported blockchains including Bitcoin and Ethereum [S1].

Looking ahead, the company is developing Exodus Pay—an integrated payments platform designed to embed self-custodial payment capabilities directly within its app ecosystem to increase transactional use cases within decentralized finance environments [S1].

Growth Outlook and Regulatory Considerations

Future growth prospects hinge on sustaining user engagement amid cryptocurrency market volatility which influences transaction volumes driving revenues [S1]. Success depends also on effective execution of new product launches like Exodus Pay along with organic expansion through B2B partnerships leveraging proprietary technologies.

Regulatory risks remain material; the company settled an OFAC enforcement action involving inadvertent service provision to users located in sanctioned jurisdictions including Iran—highlighting ongoing compliance challenges inherent to noncustodial wallet models where geo-blocking effectiveness may be limited [S5][S15]. Continued adaptation to evolving AML/KYC regulations globally is critical.

Additionally, digital asset valuation volatility poses risks that may affect balance sheet integrity through impairment charges beyond operational performance impacts.

Capital Allocation and Financial Position

Despite operational losses and cash burn, Exodus increased share repurchases significantly from $5.35 million in 2024 to $15.1 million in 2025 as part of its capital return strategy while no dividends were declared or indicated during these periods [F1].

Shareholders’ equity stood robustly at approximately $247 million as of December 31, 2025—a slight decrease year-over-year but sufficient relative to operational scale and liabilities profile [F1]. A loan agreement with Galaxy Digital LLC for up to $60 million was entered late-2025 but repaid fully within the same period indicating temporary liquidity support rather than sustained leverage reliance [S10][S8].

What Investors Should Monitor

Market participants should watch closely:

- User engagement trends especially following the launch of Exodus Pay,

- Regulatory developments including any licensing requirements impacting noncustodial wallet providers,

- Financial statement disclosures for recurring impairment or unusual cash flow patterns,

- Progress integrating acquisitions aimed at bolstering payment infrastructure,

- Adoption of AI technologies within products or processes as part of innovation efforts,

- Competitive dynamics reflected in API Provider contract renewals or term changes.

Conclusion

Exodus Movement balances innovative multi-chain wallet technology and an API-driven revenue model against near-term profitability pressures driven by market volatility and regulatory compliance costs. Its strong liquidity position supports ongoing investment phases characteristic of dynamic blockchain ecosystems.

Investors should weigh growth potential linked to new product introductions against risks from regulatory complexities and digital asset price fluctuations.

This analysis is based exclusively on publicly available information as of March 12, 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments