Travelzoo’s 2025 Profit Decline Highlights Growth and Liquidity Tradeoffs in Subscription-Driven Model

Stable membership fees underpin recurring revenue, but sharp operating profit contraction and negative working capital pose challenges.

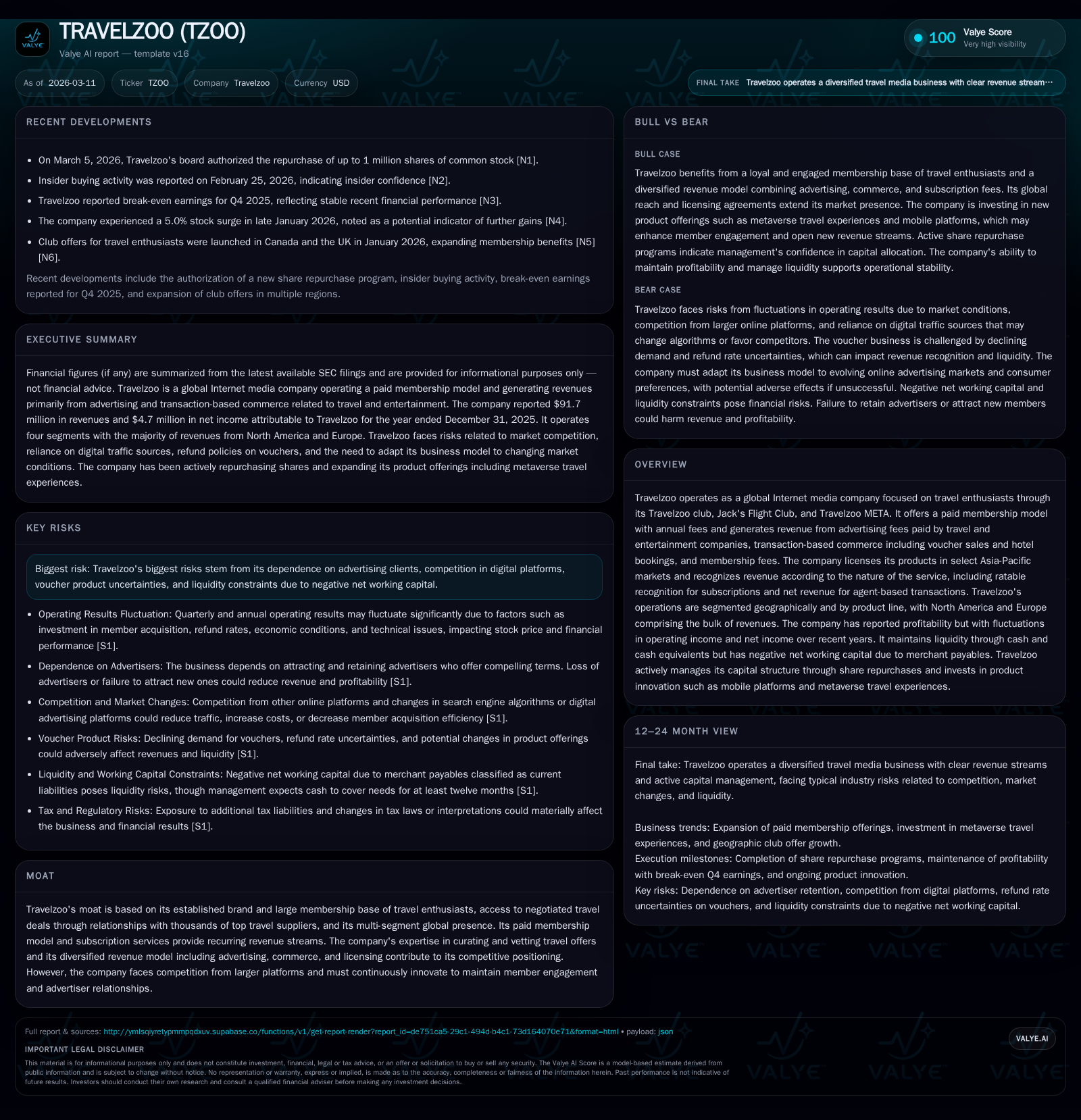

Travelzoo operates a global Internet media platform offering travel deals and memberships, with revenues split across advertising, commerce, and subscriptions. The company reached $6.9 million operating income in 2025 but experienced a steep 63% decline year-over-year amid investments in paid membership growth and new initiatives like Travelzoo META. Liquidity remains sufficient with $10 million cash, though current liabilities exceed current assets by over $10 million due to merchant payables linked to voucher liabilities. Aggressive share repurchases continue as part of capital allocation. Future growth depends on member acquisition efficacy, renewal rates, and monetization of emerging Metaverse offerings, but competition and regulatory risks persist.

Company Background and Business Model

Travelzoo is a global Internet media company targeting travel enthusiasts primarily through its flagship Travelzoo club, Jack's Flight Club flight deal subscription service, and the emerging Travelzoo META platform focusing on metaverse travel experiences [S1][S24]. Historically membership was free but transitioned in 2024 to a paid subscription model with annual fees, initiating at approximately $40 USD annually, increasing to $50 USD effective January 2026 for new U.S. members [S24]. The company generates revenues via three main streams: advertising fees from travel entertainment partners; direct commerce via voucher sales and hotel bookings; and increasingly through membership subscription fees [S8][S24].

Travelzoo maintains licensing partnerships for key Asia-Pacific territories (Australia/New Zealand/Singapore and Japan/South Korea) yielding royalty revenues contributing marginally below $100k annually [S26]. The company's geographic focus centers on North America (66% of revenues) and Europe (28%), with Jack's Flight Club accounting for about 6% [S11][S14]. New Initiatives segment includes Travelzoo META subscriptions and legacy retail/fashion business which are small contributors presently [S14].

Historical Financial Performance

The financial trajectory over recent years demonstrates modest top-line expansion alongside notable volatility in profitability metrics [F1]. Total net revenues increased from approximately $83.9 million in 2024 to $91.7 million in 2025, representing an approximate 9.3% increase primarily supported by broader adoption of the subscription model in North America and growth at Jack’s Flight Club [S11][F1]. Operating income contracted markedly by almost two-thirds to about $6.9 million in 2025 from $18.5 million the prior year, highlighting increased sales & marketing investments alongside ongoing expansion of product offerings like META [F1][S1]. Net income mirrored this decline falling from nearly $13.6 million attributable to Travelzoo in 2024 to under $4.7 million in fiscal 2025 [F1][S1].

Operating cash flows have fluctuated substantially; after a significant cash outflow of over $23 million in 2022 related presumably to investments or working capital swings, the company returned positive operating cash flow that peaked at around $21 million in 2024 before dropping again to about $5.7 million for fiscal year 2025 [F1]. Capital expenditures are minimal relative to revenues, falling below $100k most recently indicating limited fixed asset intensity [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 5 | 6 | 7 | 65000 | -65.4% |

| 2024 | 14 | 21 | 18 | 177000 | +9.7% |

| 2023 | 12 | 11 | 16 | 255000 | +86.4% |

| 2022 | 7 | -23 | 8 | 462000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 13 | 6 | -62.5 |

| 2024 | 19 | 21 | -2935.9 |

| 2023 | 17 | 10 | 295.4 |

| 2022 | 2 | -24 | 155.9 |

Source: SEC companyfacts cache [F1]. *Note: Prior years’ revenue data not fully available.

Revenue Mix and Segment Analysis

The company’s revenue mix divides broadly into three categories: Advertising & Commerce (encompassing travel publications, voucher sales including Getaways and Local Deals), Membership Fees from subscription services at Travelzoo club, Jack’s Flight Club, and META, plus Other smaller components including licensing fees [S8][S24].

Segment-wise operating performance is concentrated heavily in Travelzoo North America which comprises two-thirds of revenue but saw operating income decline significantly by approximately two-thirds from prior year levels due principally to elevated sales/marketing spending aimed at customer acquisition during the transition to paid memberships [S11][F1]. European operations grew revenues moderately but posted an operating loss of around $2.3 million reflecting investments yet to yield scale benefits [S11]. Jack's Flight Club showed incremental operating profits signaling stable subscriber engagement despite competitive pressures.

A key element weighing on near-term profitability is the ratable recognition of subscription revenue over typically one-year terms combined with elevated upfront costs for member acquisition leading to lumpy quarterly earnings patterns [S1][S25]. This delaying effect means recent gains in membership may not be fully reflected immediately on the P&L.

Capital Allocation and Returns

Travelzoo has actively pursued share repurchases as a component of capital return; the Board authorized multiple buyback programs cumulatively covering up to several million shares since late-2023 [S2][S17][F1]. In aggregate, nearly $13 million was spent on repurchases during fiscal year 2025 alone, continuing an aggressive program balanced against preserving cash resources given ongoing investments and negative net working capital conditions [F1][S17].

Despite reported net income positive results, the company's equity position declined sharply into negative territory as of December 31, 2025 (-$7.5 million), fueled by accumulated deficit impacts in part driven by share retirements reducing additional paid-in capital balances alongside retained earnings deductions [F1]. Return on equity was consequently negative at approximately -62%, underscoring limited return generation on book equity given capital structure dynamics.

On the liquidity front, cash plus equivalents totaled about $10 million at year-end with restricted cash adding nominal amounts, yet current liabilities exceeded current assets by roughly $10.8 million principally due to merchant payables linked directly to outstanding voucher liabilities—these represent amounts owed upon voucher redemption which can mature up to a year beyond expiration dates [F1][S6]. This balance sheet profile demands careful working capital management amid inherent consumer refund policies tied to vouchers.

Strategic Outlook: Growth Drivers and Constraints

Looking ahead, Travelzoo seeks to leverage its solid base of some millions of members worldwide with incremental growth targeted through new product innovation such as integrating immersive travel experiences via Travelzoo META within the metaverse environment starting in 2026—a first mover step aiming to diversify membership benefits beyond traditional deal aggregation [N4][S24][S14]. Continued refinement of its paid membership model including adjusted pricing increases aims at boosting recurring revenue stability.

However, sustaining growth will hinge on several factors: ability to recruit new paying members efficiently without eroding margins; maintain high renewal/retention rates especially as pricing rises; deploy marketing spend effectively amidst macroeconomic headwinds possibly dampening discretionary travel budgets; competitive pressures from large digital platforms offering expansive super-app integrations that can bundle travel offers alongside other consumer services; evolving regulatory requirements particularly concerning voucher products classified potentially as gift cards subject to restrictive legislation such as the CARD Act or expanding data privacy mandates requiring operational changes or added compliance costs [S18][S19][S21][S25].

Subscription-based models introduce deferred revenue timing effects making short-term volume dips less visible immediately but impactful over ensuing periods requiring disciplined forecasting.

Risks Summary

Key risks encompass dependence on advertising clients whose budgets may fluctuate cyclically or due to geopolitical/tourism disruptions; competitive displacement by larger technology ecosystems capable of capturing customer mindshare more broadly; uncertainties tied to voucher inventory pre-purchase risking unsold stock impairments that could hit profitability; liquidity pressure arising from negative net working capital posing potential constraints if redemption patterns accelerate unexpectedly or marketing spending fails to generate proportional returns; legal exposure related to intellectual property protection efforts or litigation resulting from consumer claims or securities volatility; cybersecurity threats requiring continuous investment; all layered atop macroeconomic volatility affecting travel demand globally [S7][S9][S20][S27].

What To Watch Next

Absent explicit short-term guidance disclosed publicly, observers should monitor upcoming quarterly results for trends in:

- Member acquisition volumes post recent membership fee increase,

- Renewal rates trending under higher pricing,

- Advertising/commerce revenue resilience amid competition,

- Voucher redemption cycles impacting payable balances,

- Progress updates on METAA initiative launches,

- Management commentary on expense scaling relative to revenue,

- Cash flow stability considering buyback pace. Given the operational cadence of deferred subscription revenue recognition lagging sales cycles by quarters, delayed results are expected before clear inflection points emerge.

This report synthesizes publicly filed SEC documents alongside recent market disclosures without providing investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments