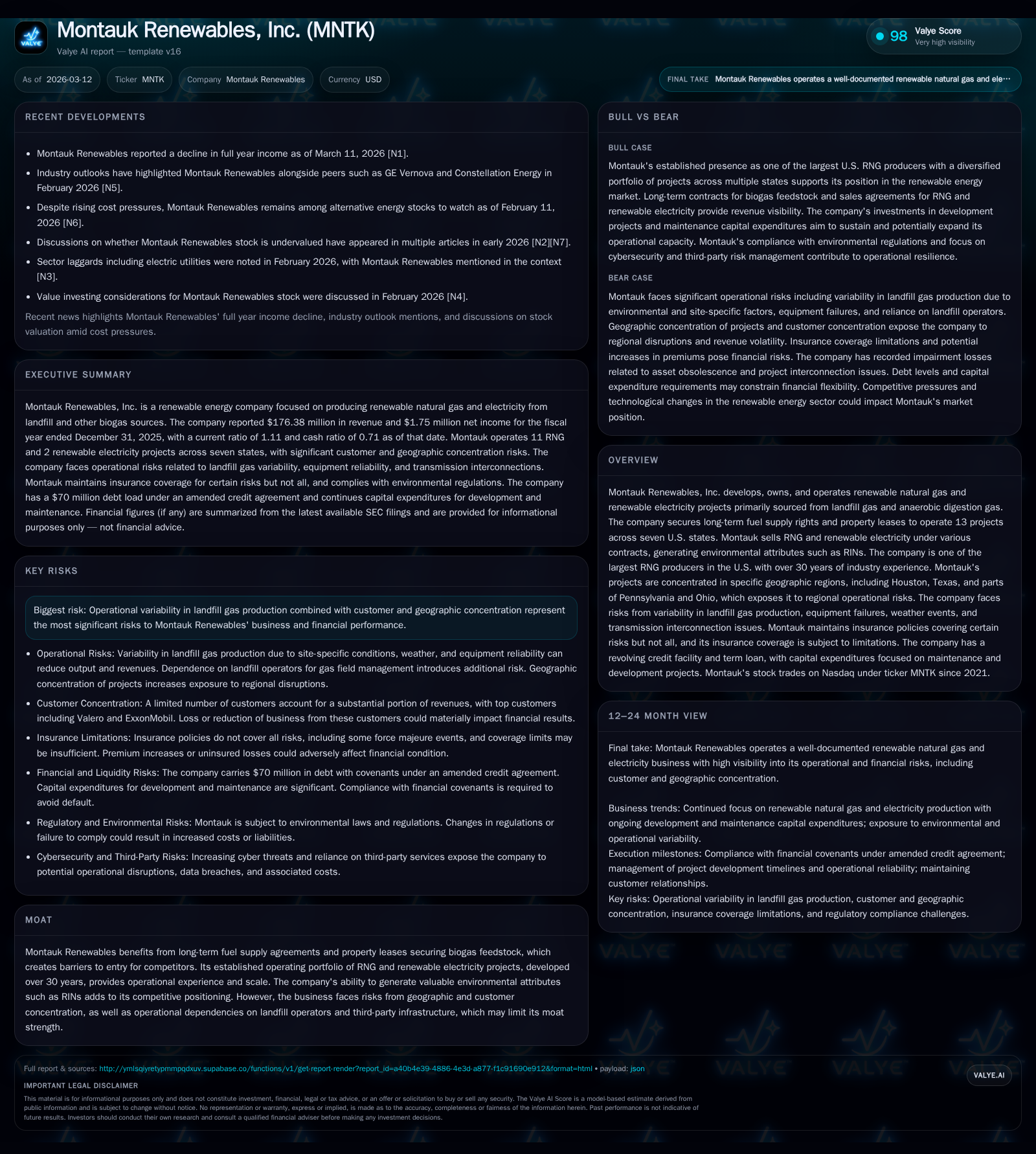

Montauk Renewables Faces Operational and Financial Pressures While Pursuing Growth in RNG Sector

Montauk Renewables' revenue growth is flat, challenged by operational variability and heavy capital expenditures amid evolving renewable natural gas markets.

Montauk Renewables, a prominent U.S. renewable natural gas and electricity producer with more than 30 years of experience, reported nearly flat revenue growth in 2025 but saw operating income compress sharply due to operational challenges and increased costs. The company's future growth hinges on expanding its project portfolio and navigating risks tied to landfill gas variability and customer concentration. Capital allocation remains heavily weighted toward development capex, resulting in negative free cash flow despite positive net income.

Company Overview

Montauk Renewables operates as a leading player in the U.S. renewable natural gas (RNG) and renewable electricity sector, leveraging long-term feedstock arrangements for landfill gas (LFG) and anaerobic digestion gas across multiple projects spanning seven states [S1]. With over three decades of industry experience, Montauk positions itself as one of the largest RNG producers in the United States, generating not only RNG but also valuable environmental attributes such as Renewable Identification Numbers (RINs) [S1].

A critical aspect of its business model is securing long-term fuel supply rights alongside property leases which provide competitive barriers by limiting entry opportunities for rivals [S1]. However, geographic concentration notably in Houston, Texas, and parts of Pennsylvania and Ohio creates vulnerability to localized risks.

Historical Financial Performance

Montauk's recent financial results reflect a stable top line juxtaposed with significant margin compression due primarily to operational disruptions and intensified capital investments.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 176 | 2 | 30 | 1 | +0.4% | -82.0% |

| 2024 | 176 | 10 | 44 | 16 | +0.5% | -34.9% |

| 2023 | 175 | 15 | 41 | 24 | -14.9% | +150.4% |

| 2022 | 206 | 6 | 81 | 9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -86 | 0.7 |

| 2024 | -19 | 3.8 |

| 2023 | -22 | 6.0 |

| 2022 | 76 | 2.6 |

Source: SEC companyfacts cache [F1].

Revenue increased modestly by just under half a percent from 2024 to 2025 but was down significantly compared to the pre-2024 peak notably influenced by changing production dynamics at landfill sites [F1]. Operating income experienced dramatic decline (-94.7%) due to higher maintenance costs, impairment losses related to project interconnections no longer accepted by utilities, and delays in key developments [S5][S20]. Net income mirrored this trend though stayed positive.

Operating cash flow declined about one-third reflecting working capital changes and higher operating expenses [F1]. Capital expenditure nearly doubled as Montauk ramped investment across multiple new development projects including Montauk Ag Renewables (North Carolina), Bowerman RNG upgrade, Rumpke relocation project, and Apex RNG facility expansion [S9][F1].

The surge in capex outpaced cash flow generation leading to an estimated negative free cash flow near $86 million in FY2025.

Future Growth Prospects

Montauk aims to expand its footprint by developing new RNG projects predominantly focused on landfill gas monetization while optimizing existing operations for improved output [S1]. Pipeline projects such as Bowerman RNG and EENA CO2 represent immediate growth catalysts with substantial development capital committed [S4][S9].

However, several factors temper growth prospects:

- Landfill Gas Variability: LFG production is inherently volatile influenced by waste composition, weather conditions (extreme heat or drought), equipment availability, and operator practices leading to uptime unpredictability [S1][S16]. For example, Houston sites were impacted by Hurricane Beryl outages in mid-2024.

- Customer Concentration: Reliance on a limited number of large customers (e.g., Valero and ExxonMobil accounted for roughly one-quarter of revenues combined in recent years) exposes Montauk to risk if these contracts are renegotiated or terminated [S11][S10].

- Regulatory & Market Risks: The value realization from environmental credits like RINs depends on regulatory frameworks which can introduce pricing volatility affecting revenue sustainability.

- Geographic Concentration: Clustering within specific states increases exposure to localized operational or regulatory disruptions.

While the company has endeavored to mitigate some risks through insurance policies and maintaining close relationships with landfill operators Waste Management and Republic Services—who jointly represent about half of revenue—uncertainties remain [S16][S27].

Forecasts and Key Milestones

Montauk has outlined capital expenditure plans projecting total development capex between $90 million and $120 million for ongoing projects in year ahead periods complementing non-development capex around $14-$17 million annually focused on maintenance and small expansions [S4]. The recent refinancing establishing a sizable senior credit facility of up to $200 million (with $155 million drawn as of March 2026) improves financial flexibility for these initiatives but imposes covenants requiring minimum leverage ratios and fixed charge coverage metrics [S7].

Financial covenant thresholds include maintaining total leverage ratio below four times EBITDA and fixed charge coverage above 1.2x; failure could constrain access to financing or trigger defaults [S7]. Investors will likely monitor operating income recovery post-impairments alongside project commissioning milestones such as completion timing at Montauk AG Renewables.

Returns and Capital Allocation

Despite positive net income in FY2025 ($1.75 million), Montauk’s return on equity remains modest at approximately 0.7%, reflecting elevated asset bases from aggressive capital expansion coupled with compressed profitability [F1]. Operating cash flows have diminished relative to recent years while capex requirements surged materially leading to sustained negative free cash flow positions.

The company has not paid dividends during the period nor engaged significantly in share repurchases beyond an authorized program capped at $5 million without definitive purchases made yet [S21][S12]. Capital allocation clearly prioritizes reinvestment into growth projects rather than shareholder returns currently.

Long-term fuel supply agreements underpin foundational asset security helping protect operating margins albeit exposure persists given external operational dependencies on landfill operators’ performances and third-party infrastructure reliability [S13][S16].

Conclusion: Navigating Opportunity Amid Constraints

Montauk Renewables presents a compelling yet challenging case in the evolving RNG industry—its established platform grants scale advantages while tethered risks could limit upside visibility near term. Record-high development capital investment signals strong growth ambitions but has compressed financial results noticeably as operational setbacks play out.

Success hinges on stabilizing production across existing assets, advancing key development projects efficiently under tight credit covenants, diversifying customer base more effectively, and adapting proactively to variable landfill gas inputs exacerbated by climate-driven weather events.

Stakeholders should watch closely how environmental credit prices evolve given their pronounced impact on revenue streams as well as how management balances heavy investment cycles against improving margin profiles going forward.

This analysis is based on publicly filed SEC reports and recent disclosures without offering investment recommendations or price guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments