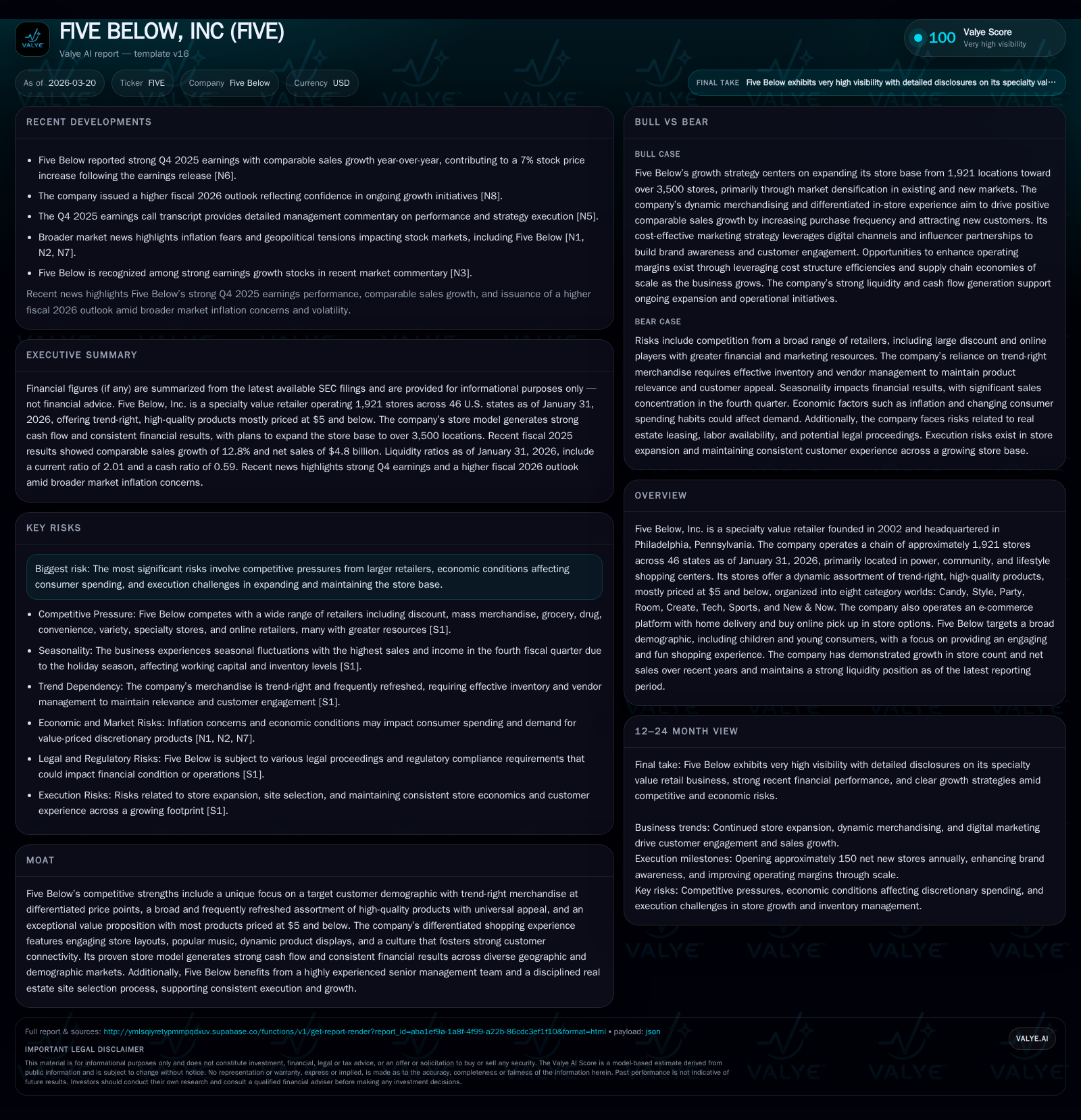

Five Below’s Store Growth and Profit Surge Reset Retail Expectations

Five Below’s blend of trend-savvy merchandising and rigorous capital management has driven a robust earnings leap enabling ambitious expansion.

Five Below posted a remarkable 19.4% revenue increase in fiscal 2025 alongside an 85.4% surge in operating income and a near doubling of net income, affirming the strength of its dynamic, 'trend-right' product strategy and engaging store experience. The company operates nearly 2,000 stores nationwide with a disciplined site selection process supporting plans to scale beyond 3,500 locations. Fiscal 2025 free cash flow topped $400 million, buttressed by a sharp reduction in capital expenditures despite ongoing network growth. Competitive pressures and inflationary headwinds pose challenges, while monitoring new store openings, comparable sales trends, and margin resilience will be key to gauging progress.

Strong Historical Growth Catalyzed by Dynamic, Trend-Right Merchandising

Five Below has demonstrated exceptional top-line and bottom-line growth in recent fiscal years underpinned by its unique retail concept. Fiscal year 2025 revenue reached approximately $4.8 billion—a substantial advance of 19.4% over the prior year—driven by both increased store count and positive comparable sales performance [F1][S7]. Operating income leapt by an even more pronounced 85.4%, reflecting effective cost controls and leverage from expanding scale [F1]. Net income soared by over 90%, reaching $358.6 million [F1].

This financial momentum owes much to Five Below's "dynamic" merchandising philosophy that emphasizes frequent refreshes of high-quality products closely aligned with current trends—the so-called "trend-right" merchandise [S4]. The company's curated assortment spans eight distinct category worlds: Candy, Style, Party, Room, Create, Tech, Sports, and New & Now [S4], providing broad appeal particularly to youth-oriented demographics while fostering repeat customer visits through an element of discovery.

The physical retail environment is crafted with intention—easy-to-navigate floor layouts with sightlines enabling shoppers to locate category worlds efficiently; lively music playlists; novel display fixtures like wheelbarrows and oil drums; colorful signage—all together creating an engaging ‘fun’ shopping destination [S4][S12]. This experiential approach differentiates Five Below from traditional discount formats and builds strong brand affinity.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 359 | 586 | 457 | 175 | +91.3% |

| 2024 | 187 | 431 | 247 | 324 | -7.3% |

| 2023 | 202 | 500 | 268 | 335 | +18.0% |

| 2022 | 171 | 315 | 345 | 252 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 412 | 16.4 |

| 2024 | 40 | 107 | 10.4 |

| 2023 | 81 | 165 | 12.8 |

| 2022 | 40 | 63 | 12.6 |

Source: SEC companyfacts cache [F1].

Data sourced from latest fiscal filings representing robust growth across key financial metrics [F1].

Strategic Expansion: From Proven Store Model to Nationwide Footprint

The company’s expansion strategy is anchored by disciplined real estate site selection targeting high-visibility malls primarily categorized as power, community, or lifestyle shopping centers ranging from urban to semi-rural trade areas [S4][S7][S12]. As of January 31, 2026, Five Below operated about 1,921 stores across 46 states with a new store model averaging roughly 9,500 square feet [S7][F1].

Site selection entails rigorous evaluation of demographics—including minimum population density thresholds—and negotiation for attractive lease terms approved centrally by a committee comprising senior management executives [S7]. This structured approach aims not only at geographic diversification but also market densification through cluster openings within existing trade areas to amplify brand presence and operational efficiency.

Investment payback periods at the store level average approximately one year on initial outlay [S4], indicating potent unit economics which underpin the confidence to pursue enlargement toward a potential network exceeding 3,500 locations over time [S1][S25]. This nearly doubling of the footprint hinges on successfully navigating some execution risks such as availability constraints for prime retail sites and securing customer traction in newer regions where brand recognition remains developing or competitive dynamics differ materially [S1][S5].

Earnings Upswing Supports Aggressive Store Addition Ambitions

Recent fiscal results reflect both improved comp store sales alongside the steady addition of net new stores—150 net openings accomplished in fiscal year 2025 following an even larger batch opened in fiscal year 2024—and guidance indicating another approximate target of ~150 new stores in fiscal year 2026 [N3][N5][S25].

Positive comparable sales gains reported during the fourth quarter reaffirmed consumer engagement amidst inflationary headwinds, with management highlighting successful inventory replenishment strategies that align closely with trending consumer preferences [N3][N4]. Gross margin resilience partially stems from leveraging both domestic sourcing advantages facilitating swift product turnover as well as opportunistic purchases of excess vendor inventory allowing price competitiveness without sacrificing quality claims [S8][S15].

To keep pace with growth ambitions, Five Below is investing in the expansion of its supply chain via newly commissioned 'shipcenters' enhancing distribution capacity—in particular facilities opened recently in strategic locations such as Buckeye, AZ—to support faster replenishment cycles critical for rapid assortment changes [S17][S25].

Capital Allocation Focus: Cash Flow Generation, Reduced Capex, and Buyback Trends

Five Below's financial stewardship manifests clearly in strong cash flow generation exceeding half a billion dollars ($586 million for FY2025), significantly outpacing capital expenditures which were curtailed by over forty percent year-over-year to approximately $175 million despite ongoing network build-out [F1]. Resulting free cash flow thus approximated $412 million—a level affording flexibility for reinvestment or other shareholder return initiatives [F1][S21].

Share repurchases were halted entirely during fiscal year 2025 after moderate buybacks totaling $40 million—already down from higher activity previously—indicating possible prioritization of balance sheet liquidity or alternative deployment uses given capital structure covenants limiting leverage expansion below revolving credit facility thresholds [F1][S14][S21]. Dividends remain nonexistent reflecting management’s decision to conserve cash within growth capex envelopes for now [F1][S21]. Return on equity stood around an estimated mid-teens range (~16.4%) signaling efficient equity use amid profit gains relative to equity base growth over recent years [F1].

The company’s diligent control over capex coupled with robust operating margins derived from its proven store economics suggests a sustainable model scalable without diluting returns excessively—a critical factor considering anticipated doubling of store counts over time requires continued capital discipline [S21][F1].

Risks on the Horizon: Competition, Inflationary Pressures, and Execution Challenges

Five Below faces notable risks that could impede or erode progress if unmanaged. Increased competition looms large as many discount chains and larger retailers aggressively vie for value-oriented consumers across physical and digital outlets—with competitors sometimes wielding greater marketing budgets or distribution reach posing margin pressure via price wars or elevated promotional spends [S18][S27].

Inflation remains a salient threat affecting product costs—including commodities and freight—that may resist complete pass-through given the company’s firm sub-$5 pricing commitment; this constraint creates inherent tension with gross margin maintenance amid cost volatility attributed to supply chain disruptions or macroeconomic factors like geopolitical conflicts raising transportation expenses [S5]. Furthermore, sustained inflation could dampen consumer discretionary spending patterns particularly among younger demographics sensitive to price increases.

Expanding into less familiar markets introduces execution complexity encompassing leasing delays or unfavorable terms due to constrained commercial development environments influenced by landlord capital limitations as well as difficulties ramping operational capabilities including crew recruitment/training essential for replicating customer experience standards at scale [S1][S5]. Additionally, over-saturation risk exists when increasing density within existing markets potentially cannibalizing sales amid finite customer bases altering store-level profitability metrics transiently or persistently.

Legal exposures such as pending securities class action litigation related partly to historic statements pose contingent expense risks though currently considered immaterial by management reflecting ongoing defense commitments without predictably adverse outcome at this stage [S9][S16][S22].

What Investors Should Monitor: New Store Openings, Cost Management, and Customer Engagement Metrics

Forward-looking guidance is limited explicitly though the company aims for roughly consistent store opening cadence (~150 stores annually) based on executed leases as well as positive comparable sales trajectories supporting expansion economics [N3][N5][S25]. Market watchers should prioritize tracking quarterly reports detailing:

- Monthly/quarterly net new store count alongside geographic distribution,

- Comparable store sales fluctuations including category-wise performance insights,

- Gross margin stability reflecting cost absorption tactics or commodity-driven pressures,

- Supply chain enhancements evidenced through incremental shipcenter openings and logistics efficiency,

- Digital engagement metrics integrating e-commerce penetration complementing brick-and-mortar,

- Operating cash flow trends against capex spend ensuring sustainable free cash flow generation.

Additionally, scrutiny toward labor market developments affecting crew hiring/training effectiveness will inform execution risk assessments given recent retail sector-wide staffing volatility challenges. Commentary on inflation mitigation initiatives or innovative merchandising mix shifts provides further insight into margin sustainability.

This analysis synthesizes publicly available financial data from SEC filings dated March 2026 ([F1], [S#]) alongside recent earnings calls ([N3], [N5]) without issuing investment advice but aiming to elucidate Five Below’s operational trajectory underpinning financial strength amid evolving retail landscapes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments