Brand Power and Capital Strategy Define Gambling.com’s Battle for Market Share in Online Gambling Affiliates

Gambling.com leverages its domain portfolio and acquisitions for growth, facing headwinds from regulatory risks and search engine dependency.

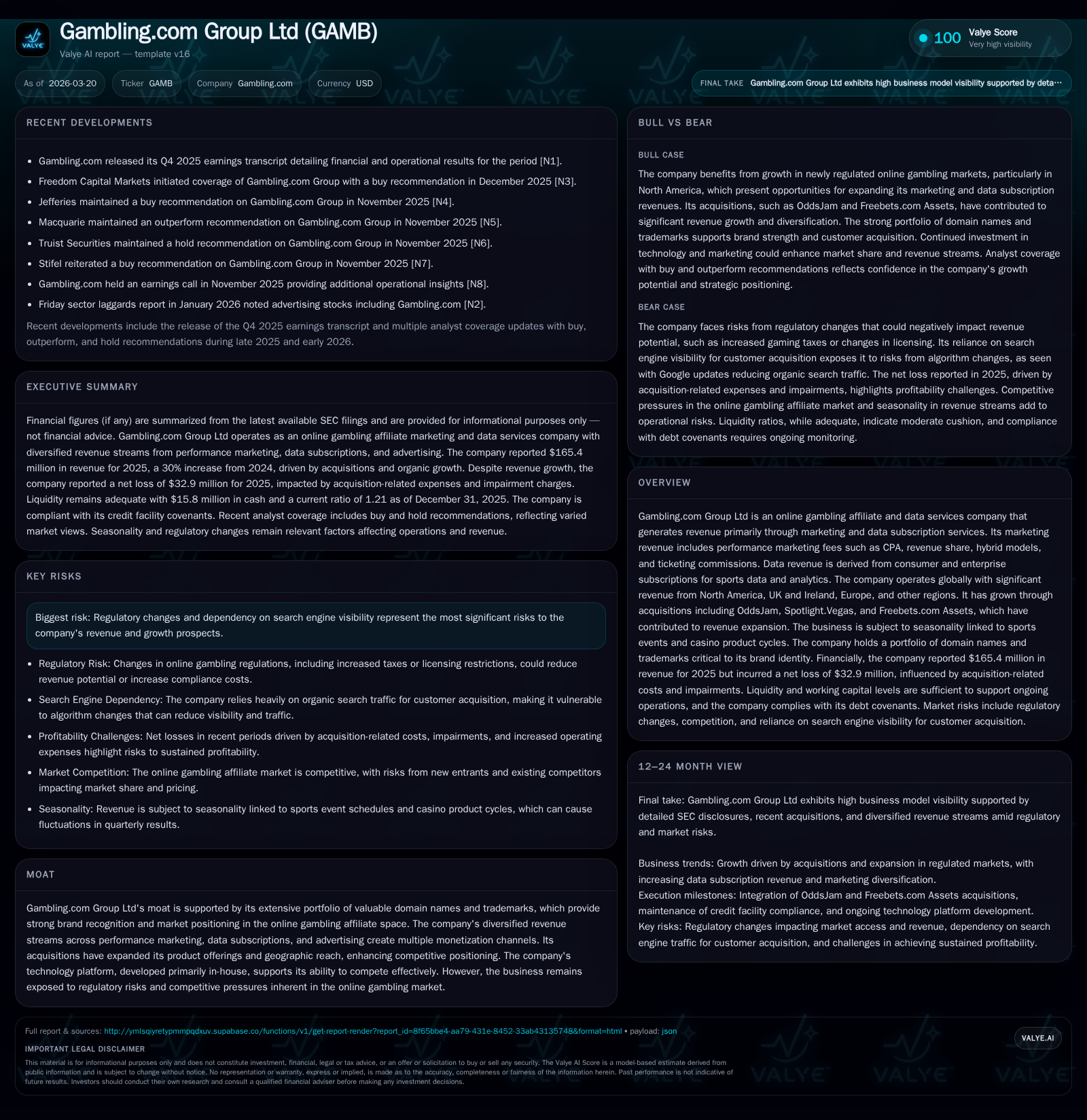

Gambling.com Group Ltd experienced robust revenue growth of 30% in 2025, driven by strategic acquisitions and expanding subscription services. Despite top-line gains, profitability pressures emerged from increased operating expenses and declining organic customer acquisition tied to Google algorithm changes. The company’s strong brand assets and technology platform underpin its competitive moat but its returns declined amidst rising regulatory uncertainties and dependency on search visibility. Capital structure enhancements, including a $165 million syndicated credit facility, provide flexibility to support operations and acquisitions. Key metrics to watch include organic customer trends, operating leverage realization, and covenant adherence amid market variability.

Historic Performance Trends: Growth Engines and Margins in Review

Gambling.com Group Ltd recorded a pronounced top-line acceleration in 2025 with revenues climbing 30% year-over-year to $165.4 million [F1][S1]. This expansion was primarily fueled by growth in performance marketing fees—encompassing CPA (Cost Per Acquisition), revenue share arrangements, hybrid models—and a striking surge in data subscription revenues following acquisitions that broadened the company's analytics footprint.

Gross profit improved by 26%, reaching $150.2 million, underpinning the business' core revenue-generating activities. However, cost structures escalated sharply: sales and marketing expenses swelled by 50% ($63 million), reflecting intensified efforts to sustain customer acquisition amid increasingly competitive channels [S1]. Technology investments also intensified with a near doubling (+78%) of related expenses ($24.8 million), indicating a strategic push into proprietary platform development aiming at long-term scalability [S17]. These upward cost pressures weighed heavily on operating profit which swung from a $35.7 million gain in 2024 to an $31.8 million loss in 2025 [F1][S1]. Net income followed suit, collapsing into a $32.9 million net loss for the year—a stark reversal from prior profitability [F1].

Overall, while adjusted EBITDA climbed by 19% to $58 million with a margin contraction to 35%, the aggregate financials reveal early-stage investment pains characteristic of rapid growth combined with elevated acquisition integration costs [S10]. The following table consolidates key financial series:

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | -33 | -207.3% |

| 2024 | 31 | +68.0% |

| 2023 | 18 | +664.0% |

| 2022 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -30.5 |

| 2024 | 24.9 |

| 2023 | 15.4 |

| 2022 | 2.7 |

Source: SEC companyfacts cache [F1].

Table notes: ROE is approximated as net income divided by average equity per year-end figures sourced from [F1]. Negative ROE in 2025 highlights profitability compression.

Revenue Mix Dynamics: Dissecting Sports vs Casino Earnings Shifts

Revenue segmentation reveals pronounced shifts favoring sports betting product lines which now constitute an increasing portion of total revenue—39% in 2025 up from just 26% two years prior—driven by growing consumer engagement with sportsbook offerings enhanced by acquired analytics capabilities from OddsJam [S1][S14]. Conversely, casino-related revenues declined proportionate to sports’ ascent but remain sizable at roughly 59%. This shift reflects an evolving client base behavior with more volatile yet potentially lucrative sports betting cycles influencing quarterly performance.

Notably, sports revenue exhibits greater seasonality linked closely with major sporting calendars which explains quarter-to-quarter volatility observed across gaming verticals [S15]. The second and third quarters typically show negative seasonality while first and fourth quarters strengthen—a pattern Gambling.com navigates through its diversified product mix.

Impact of Google Algorithm Updates on Customer Acquisition Metrics

A critical vulnerability for Gambling.com lies in its dependency on organic search traffic driven by Google’s algorithms—a core traffic source funneling New Depositing Customers (NDC) essential for performance marketing commissions. In 2025, NDCs shrank by approximately 5%, decreasing from 479k in the prior year to 454k due predominantly to Google’s algorithm update reducing visibility for affiliate links [S1][S9]. This drop constrains top-line growth potential since many marketing revenues are contingent upon converting these referrals into depositing players under CPA or revenue share terms.

SEO visibility risk implies elevated volatility within customer acquisition costs (CAC) impacting CPA fees earned per player referral—a central KPI for affiliate operators like Gambling.com [S21]. This necessitates continuous investment in SEO optimization tactics and possible diversification away from single-channel dependency.

Strategic Role of Acquisitions: OddsJam, Spotlight.Vegas, and Freebets.com Assets

Gambling.com has pursued targeted bolt-on acquisitions as part of its go-to-market expansion strategy—a tactic aimed at both geographic extension and product line deepening [N1][S1]. Acquisitions such as OddsJam injected advanced sports data subscription services enabling the company to offer enterprise-level analytics beyond traditional affiliate marketing fees.

Similarly, Spotlight.Vegas augmented the North American footprint while Freebets.com Assets expanded consumer-facing offers within Europe further diversifying monetization levers beyond pure performance fees. These moves also create incremental EBITDA opportunities through cross-selling synergy between data subscriptions and marketing units.

The company’s ability to integrate newly acquired platforms onto its proprietary technology stack enhances operating leverage potential albeit with upfront integration costs currently weighing on margin expansion prospects.

Platform Development, Technology Investment, and Operating Leverage

Underpinning Gambling.com’s competitive position is substantial investment in its technology platform which grew ~78% YoY reflecting deeper R&D commitment toward proprietary software solutions powering customer targeting algorithms and betting analytics [S17][S20]. Such investments aim not only at improving user experience but also at technological differentiation crucial in competing for organic search rankings and broader market visibility.

While this expense ramp compresses near-term profits it lays groundwork for scalable operating leverage as fixed platform costs amortize over growing subscriber bases—key for transitioning from margin pressure toward improved profitability profiles.

Liquidity Profile and Debt Structure: Wells Fargo Credit Facility Analysis

To finance expansions—including acquisitions—and ongoing operations Gambling.com negotiated an amended Wells Fargo credit facility increasing total capacity from $100 million to $165 million split between a $75 million term loan fully drawn as of Dec ‘25 and a revolving credit facility with borrowings of $57.5 million leaving $32.5 million available liquidity [S3–S6].

The syndicated credit facility matures February 2028 carries interest tied to Base Rate or SOFR plus margins around 2.50%, with mandatory quarterly principal repayments beginning mid-2025 capped by financial covenants including leverage ratio ≤3x EBITDA and minimum liquidity thresholds above $15 million all currently achieved [S4–S6].

Working capital stood positive at $7.3 million supporting operational funding along with adjusted free cash flow generation albeit below prior years owing largely to acquisition payments settled during the period [S13][S16][S24].

Capital Allocation, Returns, and Dividend Policy under Regulatory Constraints

Despite revenue gains ROE plunged deeply into negative territory (-30.5%) driven by increased net losses amplifying on impairment charges related to intangible assets [F1][S17]. Management elected not to issue dividends while securing shareholder repurchase authorization up to $20 million conditional on covenant maintenance under the Wells Fargo amendments—indicating prudent capital discipline prioritizing liquidity preservation amid regulatory uncertainties [S3][S11].

Free cash flow reported was $36.3 million down modestly reflecting growth-related capex primarily directed at internally developed intangibles improving platform capabilities rather than shareholder distributions [S18][S25].

Regulatory Risks and Dependencies: Market Access and Affiliate Visibility

The online gambling affiliate business intrinsically faces regulatory complexity due to varying jurisdictional controls over online wagering activities impacting license availability, tax regimes, advertising restrictions, and market access barriers [N1][S15]. Changes such as increased gaming tax rates could directly erode win margins or reduce operators’ promotional budgets allocated toward affiliates like Gambling.com.

Compounding this is the digital dependency risk whereby search engine algorithm updates alter organic referral flows abruptly—highlighting dual exposure not only to regulatory tolls but also SEO-driven traffic volatility undermining commission streams.

Outlook & Key Performance Metrics to Watch in Upcoming Reports

While formal forward guidance remains limited management commentary invites close monitoring of KPIs tied to recovery trends in New Depositing Customers post-Google algorithm shifts plus margin trajectory influenced by operating expense control amidst ongoing platform investment [N1][S2].

Further scrutiny on quarterly adjusted EBITDA margins will reveal if scale benefits can offset cost ramps while covenant ratios under the credit agreements will indicate financial resilience amid M&A pursuits or market fluctuations.

Investors should track diversification progress within data subscription revenues versus traditional performance marketing income as indicative of sustainable growth pathways beyond SEO-dependent channels.

This analysis relies exclusively on publicly filed financial statements (forms 20-F & 6-K) and verified earnings transcripts without speculation or forecasts beyond documented management disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments