Golden Growers Cooperative Approaches Liquidation Amid Lease Expiration and ProGold Sale

The cooperative plans to dissolve following the sale of its ProGold interest to Cargill, concluding over three decades of member value creation.

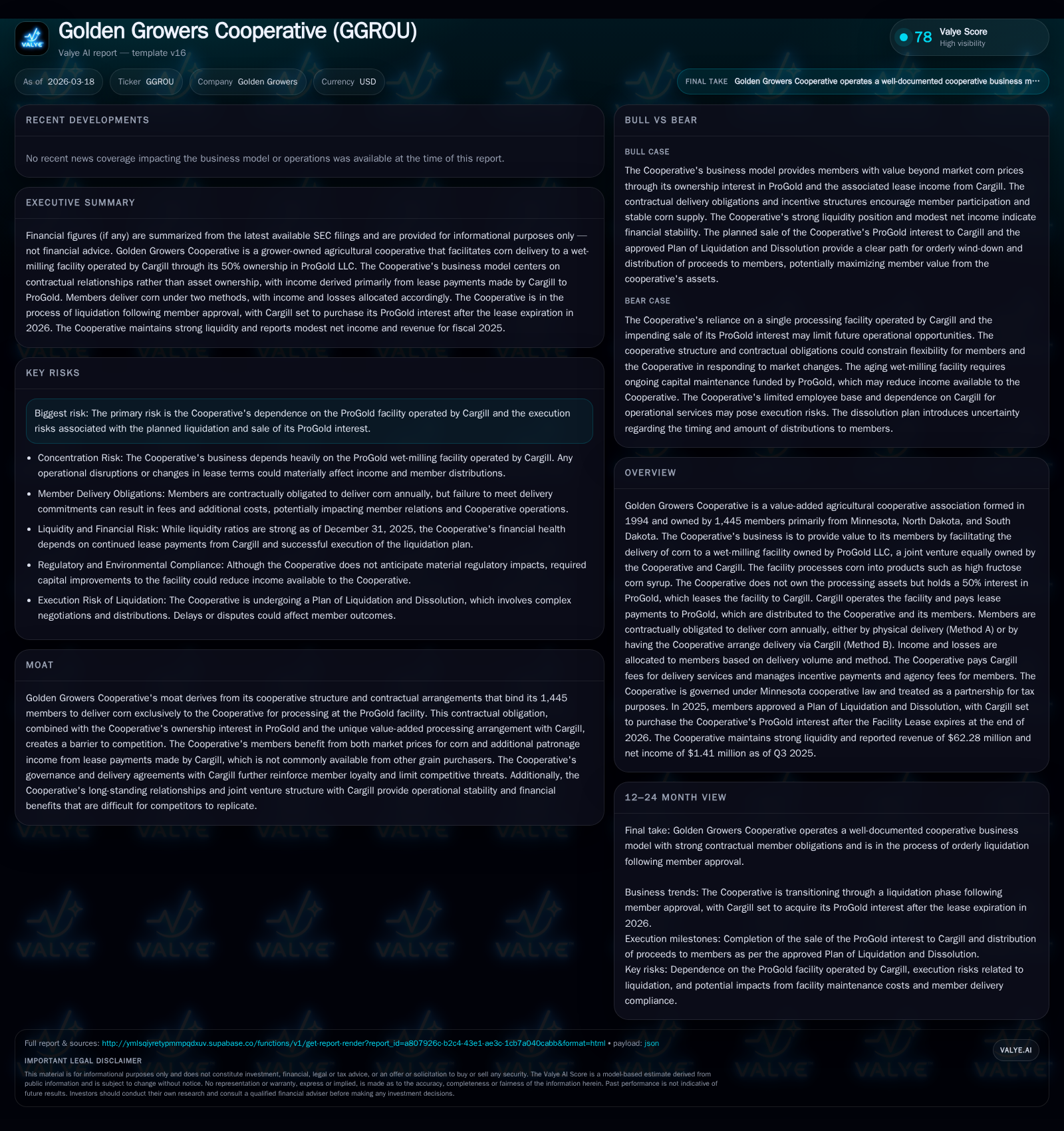

Golden Growers Cooperative (GGROU), a unique agricultural cooperative owned by over 1,400 members in the Upper Midwest, operates through a joint venture structure with Cargill tied to the ProGold corn wet-milling facility. Over recent years, revenue stabilized after declining from peak levels earlier in the decade. The cooperative generates income primarily through lease payments from Cargill’s operation of the ProGold facility and value-added patronage credit distributions to its members. With the imminent expiration of the lease and a failed joint venture renewal, GGROU is executing a formal Plan of Liquidation and Dissolution approved by members in March 2025, selling its ProGold interest to Cargill. Key risks include execution complexities of the liquidation and dependency on Cargill's facility operation, while near-term cash flow remains pressured given operational and capital constraints.

Company Overview

Golden Growers Cooperative was established in 1994 as a grower-owned agricultural cooperative focused on extracting additional value from corn grown primarily in Minnesota, North Dakota, and South Dakota. Its formation centered on creating an exclusive channel for member-delivered corn processed into high fructose corn syrup and co-products at the ProGold wet-milling facility located in Wahpeton, North Dakota.

The cooperative does not directly own physical processing assets but maintains a 50% ownership stake in ProGold LLC — a joint venture originally formed with American Crystal Sugar Company but now equally owned with Cargill Incorporated. This entity owns the mill property which is leased under long-term agreements exclusively to Cargill who operates it. In turn, lease payments made by Cargill flow back through ProGold to Golden Growers and its members.

Golden Growers operates within tightly defined contractual terms that legally bind its membership base of roughly 1,445 growers to deliver their corn output exclusively for processing via the Cooperative’s arrangement. Members can choose between two delivery methods: physical delivery directly (Method A) or authorizing Cooperative-arranged acquisition and delivery via Cargill (Method B). This hybrid system facilitates efficient logistics management while maintaining price incentives tied to delivery methods.

Historical Performance Drivers

The cooperative’s revenue is predominantly lease-based income derived from annual rent payments made by Cargill for operating the ProGold facility. Historically, this steady stream complemented by patronage distributions has underpinned consistent financial returns for members beyond standard commodity sale prices for corn.

Financial data spanning recent years illustrates this dynamic:

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 62 | 1406000 | -396000 | 6 | +0.5% | -9.9% |

| 2024 | 62 | 1561000 | -396000 | 6 | -29.6% | |

| 2023 | 88 | -281000 | 5 | -18.1% | ||

| 2022 | 107 | -410000 | 6 |

Source: SEC companyfacts cache [F1].

Source: Golden Growers Cooperative SEC filings analyzed [F1].

The precipitous revenue drop post-2022 corresponds with reduced lease payment scale and long-term operational adjustments at the aging wet-milling facility first built in 1995. Notably though operating income has shown modest stability or slight improvement recently despite revenue fluctuations.

Operating cash flows have persistently hovered negative owing largely to working capital timing differences and minimal capex spend due to the leased nature of physical assets.

Operational Structure & Business Model

The core asset providing income generation is Golden Growers' membership interest in ProGold LLC which captures lease revenues after costs incurred running or maintaining the plant.

Members are each issued Units proportional to their required corn delivery commitments (about 15.49 million bushels annually). Allocation of income or loss is similarly proportional, with a minimum allocation threshold ensuring compensation advantages for Method A deliverers who physically transport their own corn versus those relying on contracted delivery services provided by Cargill.

Cargill acts as the Cooperative's appointed agent handling delivery coordination and payments to members based on market prices plus incentive schemes — including $0.05 per bushel bonuses for Method A deliveries contrasted with $0.02 per bushel agency fees for Method B deliveries subject to board discretion.

This distinctive arrangement creates a moat that limits competition: members are contractually obligated not only by governance documents but also incentivized financially to stay within this ecosystem rather than seek external buyers or processors.

Lease Agreement & Facility Operations

ProGold entered into an operating lease agreement with Cargill commencing November 1, 1997 which has been amended several times with current term expiring December 31, 2026.

Under this lease:

- Annual rent rose modestly over time: $15.5 million in 2023 shifting to $16 million annually starting in 2024 through lease end.

- Cargill assumes operational risk and responsibility including infrastructure projects valued near $25 million.

- Cost sharing for infrastructure maintenance reduces distributable earnings proportionally between owners.

Facility age was noted as increasing maintenance risk though ongoing capital projects financed largely by Cargill aim to sustain operability.

Recent Strategic Developments & Liquidation Plans

In December 2024 Golden Growers and Cargill publicly announced that economic conditions over prior years impeded establishing a renewed long-term joint venture agreement beyond existing lease terms [S4]. Consequently:

- Per operating agreement provisions if no new joint venture is concluded following triggering events by end-2026, Cargill will purchase Golden Growers' entire membership interest in ProGold for a fixed price of $81 million plus half remaining lease payments due through end-2026.

Following this announcement:

- At the March 2025 annual meeting members overwhelmingly approved a Plan of Liquidation and Dissolution including authorization for orderly sale execution and asset distribution [S18].

- Board holds authority to finalize all necessary agreements required to wind down operations.

This marks an existential shift as Golden Growers prepares to exit its value-added business model after more than three decades.

Capital Allocation & Financial Returns

Golden Growers maintains a lean headcount (one executive vice president serving as CEO/CFO) reflecting its cooperative agency role rather than direct operations [S13].

The cooperative pays nominal fees annually (approximately $60K) to Cargill for administrative services related to member corn deliveries alongside penalty fees for member shortfalls covering handling costs [S16].

Dividends or direct capital returns are essentially patronage distributions linked closely to net income allocations from ProGold profits deriving mainly from facility lease payments.

While explicit return on equity or free cash flow metrics are limited given negative operating cash flows approximating -$400K despite reasonable profitability margins (~9% operating margin), returns manifest as incremental value passed back directly through member patronage credits rather than stock repurchases or typical dividend payouts [F1][S18].

Industry Context & Competitive Positioning (Analysis)

Corn wet milling facilities represent critical nodes linking raw agricultural production with industrial food ingredient markets such as high fructose corn syrup suppliers. Most cooperatives face intensifying pressures from large vertically integrated agribusinesses typically controlling processing assets outright rather than through joint ventures.

Golden Growers’ model—member ownership paired with strict delivery obligations—forms a barrier rarely matched elsewhere because it embeds economic incentives aligned between farmer-suppliers and processor operations elegantly coordinating supply chain risks.

Local competitors lack these alignment features often leading farmers into spot sales without patronage-style value capture beyond commodity pricing alone.

However aging infrastructure combined with complex joint venture governance involving major industry players like Cargill may constrain reinvestment appetite and strategic flexibility moving forward.

Risks & Uncertainties

Key risks primarily stem from:

- Dependency on ongoing operational performance of the aging ProGold wet-milling facility under sole control of Cargill.

- Execution risk associated with liquidation process complicated by member expectations and regulatory compliance during dissolution phases.

- Potential adverse effects if environmental regulations mandate expensive upgrades reducing distributable earnings from lease income [S3][S9].

- Market risks related to corn pricing volatility impacting member deliveries although mitigated somewhat via contractual arrangements enforcing delivery commitments.

Outlook & What To Watch (Analysis)

With active liquidation underway post-member approval:

- Monitoring progress toward completion of sale agreement settlements is crucial including any negotiated amendments delaying or accelerating dissolution timelines.

- The impact on member liquidity resulting from distributed proceeds relative to invested capital will inform overall success of legacy investment thesis held since inception.

- Potential secondary markets form around remaining contractual rights or residual assets could develop but would likely be limited given cooperative dissolution intent.

Absent further disclosures no formal guidance exists; investors should focus on final reporting filings documenting wind-up status milestones within forthcoming fiscal cycles.

Summary

Golden Growers Cooperative stands as an archetype of crop producer empowerment leveraging joint venture structures that combine shared ownership benefits with operational outsourcing leveraging agribusiness expertise. While recent years have seen revenue contraction corresponding with broader challenges—and culminating now in planned exit—the cooperative has delivered steady economic rents distributed among its dedicated membership base over decades.

Its trajectory highlights inherent tradeoffs for cooperatives engaging complex asset partnerships: robust contracting provides moats yet can also limit strategic renewal options when market conditions shift unfavorably or capital needs arise unexpectedly.

This impending closure phase marks both an endpoint for Golden Growers’ original vision and a case study moment illustrating cooperative industrial participation dynamics writ large within agricultural commodity supply chains.

Disclaimer: This report is prepared solely for informational purposes based on publicly available data as of March 18, 2026. It does not constitute investment advice or recommendations regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments