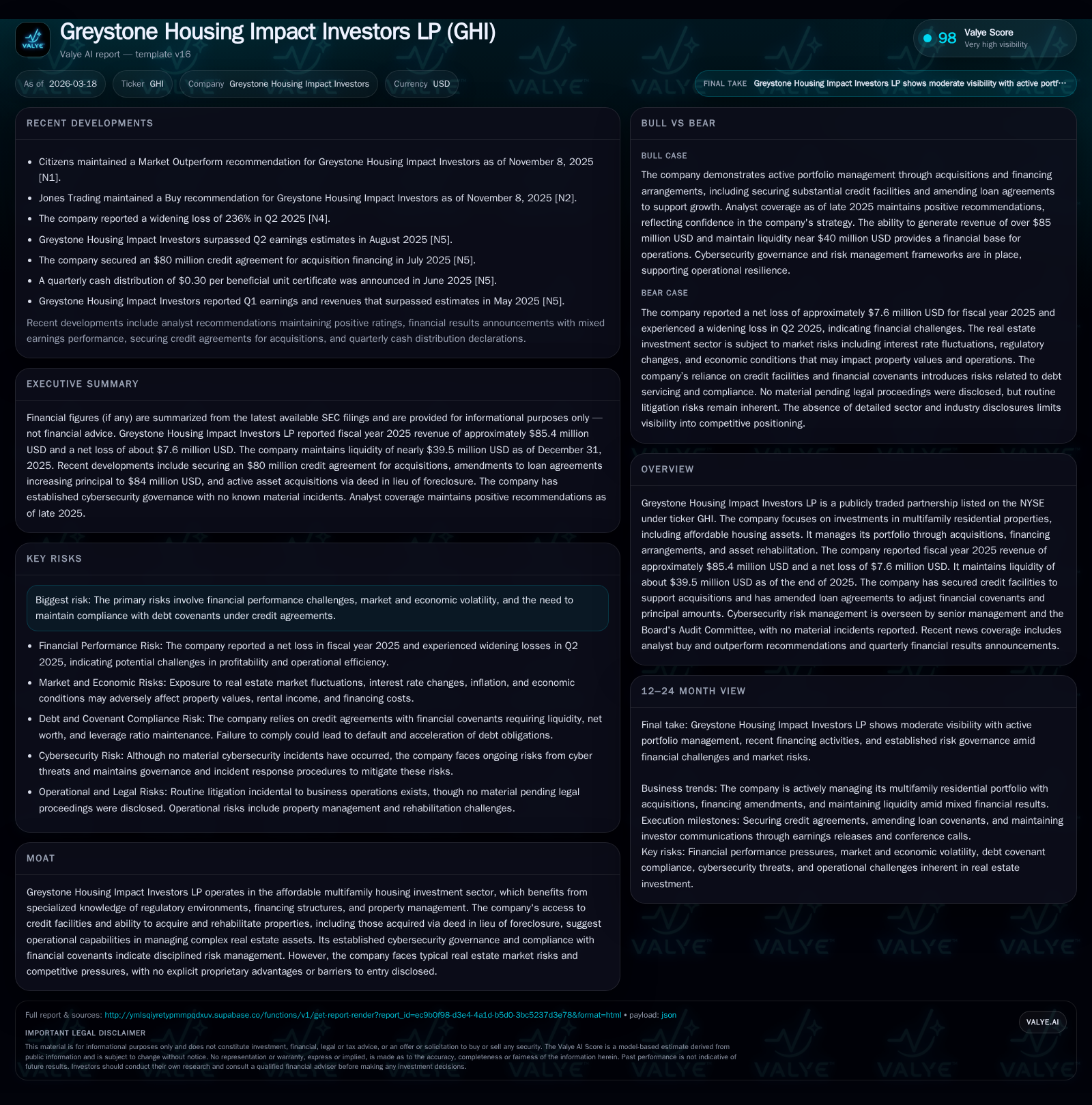

Greystone Housing Impact Investors LP’s 2025 Surge and Financial Realignment

A dramatic increase in 2025 revenue contrasts with a net loss, highlighting strategic capital deployment and credit management in affordable multifamily housing.

Greystone Housing Impact Investors LP recorded an exceptional 278% revenue surge to approximately $85.4 million in fiscal year 2025, following steady growth in prior years. Despite this top-line leap, the company reported a net loss of $7.6 million, reflecting intensified financing costs and non-cash charges amid expanded portfolio acquisitions through deed-in-lieu of foreclosure transactions. Strong operating cash flow growth and active credit facility amendments underpin the company's capital structure realignment, aiming to sustain its impact-driven multifamily affordable housing strategy amid evolving market and regulatory conditions.

From Steady Gains to Revenue Leap: Historical Growth Trajectory and Performance Drivers

Greystone Housing Impact Investors LP demonstrated extraordinary top-line growth in fiscal year 2025, catapulting revenue from $22.6 million in 2024 to approximately $85.4 million — a striking +278% year-over-year increase [F1]. This surge contrasts with more moderate fluctuations in prior years; revenue fell slightly from $25.2 million in 2023 to $22.6 million in 2024 before the jump in 2025. Operating income data is partially available, showing a steady rise from $3.17 million in 2022 to over $10.1 million in 2024, though operating income figures for 2025 are not reported explicitly [F1].

This revenue acceleration correlates with the company’s strategic acquisition activity involving multiple affordable multifamily properties initially owned by non-profit entities. These acquisitions often occurred via deed in lieu of foreclosure at the start of 2026 (i.e., properties did not achieve required operating results under mortgage revenue bond agreements), underscoring Greystone's operational capability to manage complex asset restructurings [S11][S16][S28]. The portfolio expansion also involved converting market-rate units into rent-restricted affordable housing post-rehabilitation.

Capital expenditures remained relatively consistent historically; comparing available figures implies a focus on property improvements rather than development of new assets [F1], as capex was stable around earlier years’ levels without spikes commensurate with acquisition scale.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 85 | -8 | 38 | +278.1% | -135.7% | |

| 2024 | 23 | 21 | 18 | 10 | -10.3% | -60.5% |

| 2023 | 25 | 54 | 25 | 6 | +14.3% | -17.6% |

| 2022 | 22 | 66 | 21 | 3 |

Source: SEC companyfacts cache [F1].

Table: Greystone Housing Impact Investors LP Annual Financial Summary FY2022-FY2025 [F1]

Decoding the 2025 Profitability Decline Amid Robust Operating Cash Flows

In stark contrast with its soaring revenues and strong operating cash flow (CFO), Greystone reported a net loss of approximately $7.6 million for fiscal year 2025 [F1]. This pivot from positive net income ($21.3 million in FY24) likely reflects elevated interest expenses due to increased leverage employed for acquisitions and non-cash charges such as asset impairments or deferred financing costs related to newly acquired foreclosed properties [S1][S9].

The company’s ability to generate operating cash flows climbing +109% YoY to over $37.5 million demonstrates robust underlying asset performance and operational liquidity despite bottom-line pressure [F1]. The divergence signifies that while accrual accounting impacts profitability through amortization or mark-to-market effects on derivatives or impairments, the actual cash generation remains sound.

Leveraging Credit Facilities: Navigating Debt Covenants and Amended Loan Agreements

Greystone’s acquisition growth has been underpinned by sizeable credit facilities—up to $84 million principal—with BankUnited as administrative agent and ServisFirst Bank as lender [S4][S6][S8]. The original Loan Agreement entered December 31, 2025 was amended February 27, 2026 (First Amendment), confirming additional advances totaling $42 million used for further property acquisitions [S12][S16][S28].

Financial covenants were refined through these amendments:

- Debt Service Coverage Ratio (DSCR) requirements set at minimums of 1.00x by February 15, 2027 rising to 1.05x by June 30, 2027 [S16]. Failure triggers options such as mandatory partial prepayments or posting collateral.

- Minimum total liquidity must be maintained at no less than $30 million quarterly for the guarantor entity (Greystone Select Incorporated) [S4][S6].

- Partnership-wide net worth floors exceed $200 million quarterly [S6].

- Leverage ceilings capped at a maximum of 4.50:1 ratio [S4].

Interest is charged at one-month Term SOFR plus a fixed spread of 2.75%, resetting monthly; derivative swap agreements hedge floating rate exposure across principal amounts totaling $84 million [S8][S10]. Prepayment fees were waived starting end-December 2026 providing optional refinancing or extinguishment flexibility [S8]. Administrative agents hold cure rights extending up to approximately three months post-default before taking enforcement action providing operational breathing space [S4].

These covenant structures reflect typical real estate finance discipline yet demand prompt adherence given semiannual DSCR test dates commencing early-mid calendar year following acquisition cycles.

Capital Deployment Priorities: Asset Acquisitions, Rehabilitation, and Working Capital

Capital outlay priorities have been strategically channeled toward acquiring multifamily residential assets transitioning under rent restriction programs from previous non-profit owners who rehabilitated the properties but defaulted on mortgage revenue bond terms [S11][S16][S28]. Notable properties include complexes such as The Park at Sondrio Apartments and Century Plaza Apartments located in South Carolina.

Despite the large-scale addition of these assets via deed-in-lieu foreclosure mechanisms facilitating portfolio scale-up without outright market purchases at premium prices — capital expenditures have remained relatively flat compared to previous years suggesting focused rehabilitation over new development or expansion capex investments [F1]. This allocation preserves working capital aiding liquidity comfort mandated under loan covenants.

Such rehabilitation work alongside lease-up efforts within affordable housing frameworks typifies sector practices aiming for long-term value creation while managing upfront operational risks.

Risk Oversight Through a Cybersecurity and Compliance Lens

Governance regarding cybersecurity is managed primarily by the CFO alongside internal staff experienced over two decades in IT risk audits supported by consultation with the Chief Information Security Officer of affiliated Greystone entities [S1][S29]. An Information Security Committee oversees ongoing initiatives ensuring controls meet evolving threat landscapes including penetration testing and third-party audits.

Incident response protocols require immediate CEO and CFO notification upon detection of any breach reports with escalation procedures culminating in Audit Committee review for material events ahead of public disclosure responsibilities [S1]. To date no material cybersecurity incidents have impaired operations or financials.

Such proactive risk management is vital given increasing digital integration across asset management platforms amid sector norms emphasizing rigorous control frameworks.

Forward-Looking Markers: Metrics, Covenants, and Strategic Expectations

Looking ahead investors should monitor regular compliance with semiannual DSCR thresholds starting February and June of calendar year following acquisitions per amended loan terms [S16]; triggers that could precipitate prepayments or collateral postings remain critical liquidity signals.

Optional maturity extension rights through December end-2028 provide flexibility contingent on covenant status including DSCR and loan-to-value safeguards plus payment of nominal extension fees (~0.25%) maintaining debt cost control [S8][S16]. Portfolio valuation dynamics and macroeconomic interest rate trends (given floating rate nature notwithstanding swaps) will shape financial outcomes.

The partnership's public disclosures around quarterly covenant adherence updates—including any press commentaries around asset operational results or refinancing efforts—will be key monitoring points absent explicit forward guidance.

Evaluating Returns: Operating Cash Flow Strength Versus Net Income Volatility

Absent detailed ROE disclosures typical for partnerships focusing on real estate investment margin nuances can be inferred through cash flow proxies: operating cash flows more than doubled to ~$37.5m providing ample free cash flow when adjusted against modest capex spends supporting reinvestment capacity despite negative net income outcomes impacted by accounting items such as amortization or impairment reserve build-ups related to acquired foreclosed assets [F1].

No dividends or buybacks have been disclosed indicating reinvestment emphasis consistent with growth stage profile; meanwhile prudent leverage use under credit covenant guardrails signals disciplined capital returns strategy balancing portfolio scale ambitions against solvency risks.

Key Sector Terms: Loan-to-Value, Debt Service Coverage Ratio Dynamics

Within Greystone's operational context:

- Debt Service Coverage Ratio (DSCR) defines ability of property-level net operating income plus other cash inflows measured against total debt service obligations; ratios below 1.0x indicate insufficient cash earnings which trigger lender remedial actions including repayment demands or collateralization enhancements [S7][S16].

- Loan-to-Value (LTV) ratios govern collateral adequacy relative to outstanding loan principal; maintaining LTV caps mitigates lender risk exposures upon property valuation swings common during macroeconomic shifts.

- Property Rehabilitation vs Redevelopment: Rehabilitation involves refurbishing existing structures aiming at improving function/value primarily within affordable housing stock often constrained by regulatory rent limits; redevelopment implies ground-up new construction generally requiring larger capital outlays—and complexity—which Greystone appears less engaged with currently given steady capex levels amid aggressive acquisitions through foreclosure scenarios.

Mastering these metrics ensures compliance discipline necessary for sustaining access to capital markets tailored for impact-oriented multifamily portfolios amidst tightening lending standards.

This analysis synthesizes currently available audited financial data and regulatory filings through March 18th, 2026 strictly adhering to documented disclosures without speculative assumptions regarding future initiatives or unrealized operational shifts. Investors seeking deeper technical insight should align due diligence efforts with evolving quarterly covenant reports once published alongside periodic management commentary from upcoming investor calls referenced within SEC filings.

Disclaimer:

This report is prepared solely for informational purposes using publicly available data sources cited herein. It does not constitute investment advice or recommendations regarding securities of Greystone Housing Impact Investors LP or any other entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments