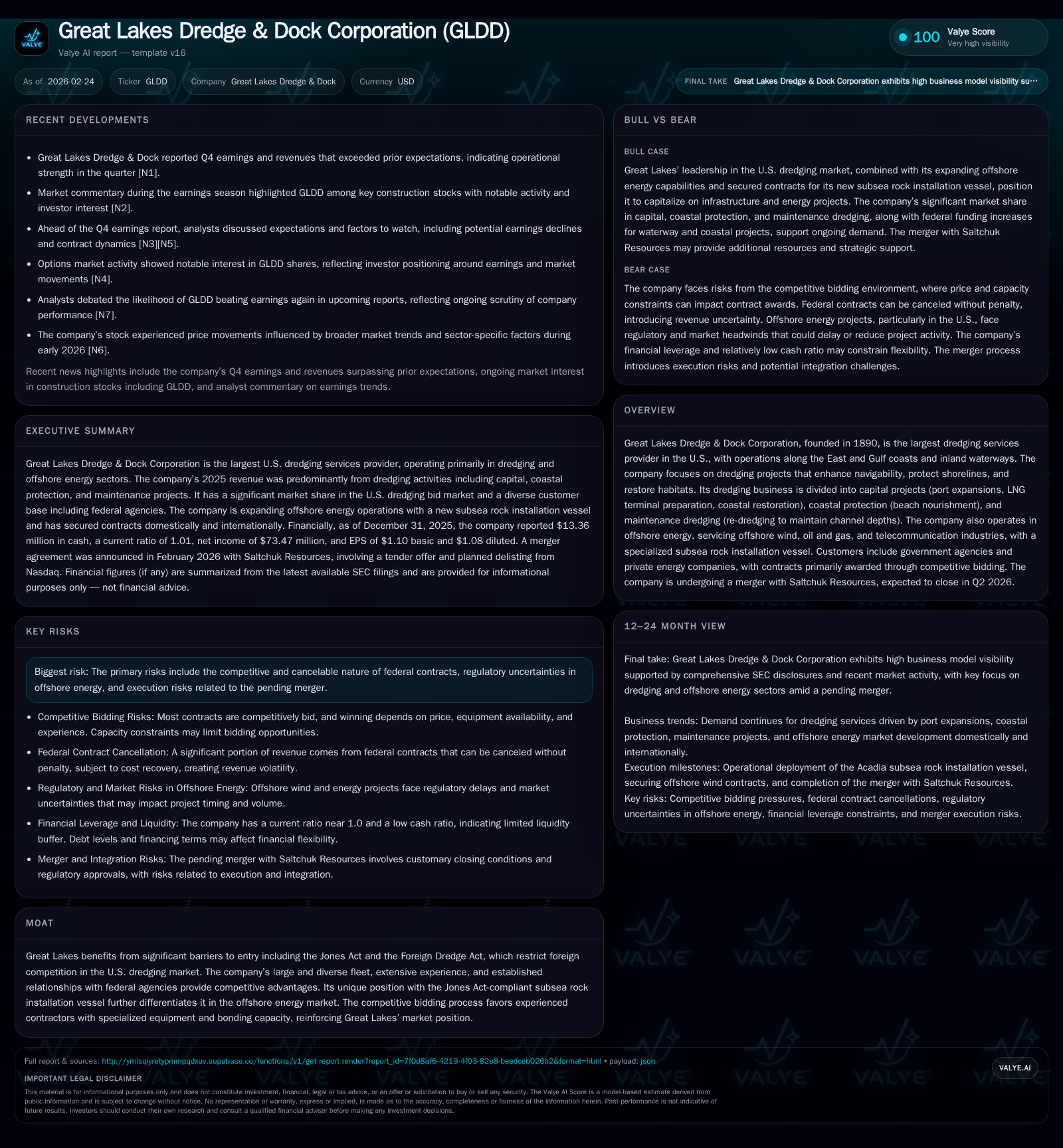

Great Lakes Dredge & Dock’s 2025 Performance Highlights Operational Resilience and Merger Transition

GLDD posted strong earnings growth in 2025 despite revenue headwinds, driven by robust contract wins and fleet specialization.

Great Lakes Dredge & Dock Corporation (GLDD), the largest U.S. dredging services provider, delivered improved profitability in FY2025 with a 38% operating income increase year-over-year, fueled by steady federal contract awards and offshore energy expansion. Revenues declined modestly due to project mix and competitive pricing pressures. The company maintains strong operating cash flow and invests heavily in capital assets to modernize its fleet for both traditional dredging and emerging offshore wind markets. GLDD is undergoing a merger with Saltchuk Resources expected to close in Q2 2026, which introduces near-term integration risks but also long-term strategic potential.

Historical Performance Overview

Great Lakes Dredge & Dock has demonstrated operational resilience across recent years despite pronounced industry cyclicality and regulatory complexity. The firm reported revenues of approximately $702 million in FY2025, marking an 8.5% decrease from the prior year’s levels [F1]. This decline reflects softer demand for liquefied natural gas (LNG)-related capital dredging projects combined with intensified competition on federally funded coastal protection work. Notably, these segments traditionally command higher margins but face pricing pressures due to competitive bidding processes mandated by agencies like the U.S. Army Corps of Engineers [S4].

Despite top-line pressure, operating income notably reversed course from past volatility, soaring to about $128 million in FY2025 — nearly a 38% increase year-over-year [F1]. Net income followed suit with a strong advance to $73 million, up roughly 28%, evidencing margin recovery through improved project execution efficiencies and disciplined cost control. Enhanced earnings translated into stronger free cash flows; operating cash flows tripled to nearly $247 million while capital expenditures rose to $147 million to support fleet modernization initiatives critical for maintaining compliance with the Jones Act and expanding offshore energy capabilities [F1][S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 73 | 247 | 128 | 147 | +28.3% |

| 2024 | 57 | 70 | 93 | 125 | +311.8% |

| 2023 | 14 | 47 | 28 | 151 | +140.8% |

| 2022 | -34 | 2 | -28 | 143 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 12 | 99 | 14.2 |

| 2024 | -55 | 12.8 | |

| 2023 | -103 | 3.6 | |

| 2022 | 4 | -141 | -9.2 |

Source: SEC companyfacts cache [F1].

*estimated revenues for prior years inferred from SEC filings where exact figure missing [F1]

Business Model and Industry Position

Great Lakes operates almost exclusively within one reportable segment—dredging services—which accounts for over 97% of revenues. Its domestic footprint spans major East Coast and Gulf Coast ports, along with inland waterways. The business divides into three key categories:

- Capital dredging (51% of dredging revenues): Includes port expansions, channel deepening, LNG terminal preparation.

- Coastal protection (typically beach nourishment): Restoration of shorelines against erosion.

- Maintenance dredging: Channel upkeep including re-dredging previously serviced waterways.

Further diversification has come from offshore energy services targeting emerging offshore wind farms as well as oil & gas subsea infrastructure installation with its unique Jones Act-compliant subsea rock installation vessel—an entity protected by the Foreign Dredge Act limiting foreign competition [S4][S13]. These regulatory barriers underpin a substantial moat for Great Lakes given the high costs to develop specialized fleets compliant with U.S.-flag requirements.

The company commands significant market share—approximately one-third overall bid market share domestically—with even stronger positioning in capital dredging sectors (36% market share) and coastal protection (46%) excluding LNG related projects [S4]. This advantage stems not only from its extensive fleet size but also longstanding relationships with government agencies such as the U.S. Army Corps of Engineers, U.S. Coast Guard, and Navy who collectively account for nearly half the customer base through awarded contracts totaling around a dozen major projects annually [S4]. Advanced bonding capacity—a prerequisite for government contracts—and demonstrated safety records further differentiate bidding success rates.

Growth Drivers and Future Prospects

Growth prospects hinge critically on several factors:

- Infrastructure spending: Federal initiatives targeting port modernization, coastal resilience against climate impact, hurricane recovery efforts could bolster capital dredging volumes.

- Offshore wind sector expansion: Greater investment into offshore renewable energy development catalyzes demand for specialized seabed preparation and material placement.

- Regulatory environment: Continued enforcement of Jones Act restrictions limits foreign entry keeping domestic providers like GLDD favored.

- Fleet modernization: Strategic investment in agile vessels tailored for offshore wind enhances capability versus competitors relying primarily on traditional maintenance dredging.

Adjacent market entry into offshore telecommunications cable laying or oilfield decommissioning also present incremental avenues though remain subscale at present relative to core operations.

Risks that could constrain growth include cancellation or delay of large-scale government projects due to budget cutbacks or shifting priorities along with merger integration uncertainties given the pending acquisition by Saltchuk Resources which may deter operational focus or impede capital allocation agility temporarily [S1][S13].

Capital Allocation & Financial Health

Great Lakes sustains healthy returns on equity; FY2025’s approximate ROE stands at ~14%, sharply improved from losses during pandemic-related disruptions just a few years prior [F1]. The company generates robust operating cash flows adequate to fund significant capex requirements estimated in excess of $140 million annually necessary for vessel upgrades plus investments aligned with green technologies qualifying under its green loan provisions offering marginally lower borrowing costs [S8][S15].

Its liquidity profile is balanced with a current ratio near parity at around 1.01x signaling tight working capital management but limited buffer against unexpected liabilities or project timing delays [F1]. Debt comprises primarily a $100 million senior secured second-lien term loan facility carrying elevated interest rates north of 12%, alongside a revolving credit facility extended recently up to $330 million providing flexible liquidity access for bond issuance collateralization or working capital needs . Covenant constraints linked to fixed charge coverage ratios mandate minimum liquidity maintenance levels requiring careful cash flow monitoring.

Dividend distributions have been nominal historically post-2010s while share buybacks continued at modest levels (~$11.6 million repurchased in FY2025), suggesting preference towards reinvestment over shareholder returns in recent cycles given growth stage capital intensiveness [F1].

Merger Transaction Details & Outlook

On February 10, 2026, Great Lakes announced an agreement to be acquired by Saltchuk Resources via a tender offer priced at $17 per share pending customary approvals including antitrust clearance anticipated by Q2 CY2026 [S1][N1]. Upon closing, Great Lakes will become a wholly owned subsidiary of Saltchuk and delist from Nasdaq.

The merger represents a pivotal strategic inflection point offering potential synergies through integrated logistics capabilities particularly across marine transportation channels owned by Saltchuk enhancing project delivery efficiency as well as capital access flexibility post-deal closure.

However, it carries execution risks typical of mid-market M&A transactions such as cultural integration hurdles, potential regulatory scrutiny especially regarding competition concerns within maritime construction services markets given GLDD’s commanding market share balance between government-backed projects versus private offshore energy contracts [S13][S24]. Monitoring progress on merger milestones including shareholder tender participation rates and regulatory review status will be critical signals heading into late spring/early summer calendar timelines.

Industry Analysis Context

The U.S. dredging market is niche yet essential infrastructure leveraging entrenched regulatory protections like the Jones Act which mandates U.S.-built and crewed vessels for domestic maritime activities placing substantial barriers against international competitors thereby fostering oligopolistic conditions favoring incumbents such as GLDD.

Dredging heavily relies on federal budget appropriations funneled primarily through the Army Corps impacting project flows often subject to seasonal work constraints tied to weather patterns affecting coastal restoration efforts.

Fleet utilization rates are key operational metrics influencing margins; companies like Great Lakes optimize asset deployment balancing maintenance downtime versus peak project demands while managing variable fuel costs often hedged strategically albeit exposure remains notable given volatile energy pricing dynamics reflected within cost structures outlined in recent filings [S9][S13].

Conclusion & Key Monitoring Points

Great Lakes Dredge & Dock has rebounded strongly operationally post-pandemic downturns delivering solid earnings growth despite narrower revenue trajectories driven largely by stable federal contracting success complemented by fleet enhancements supporting entry into growth segments like offshore wind.

Capital discipline evidenced by strong operating cashflow generation supports ongoing asset reinvestment though high debt servicing costs temper financial flexibility somewhat.

The pending acquisition by Saltchuk Resources introduces transitional risks but positions GLDD well within an integrated marine logistics platform potentially unlocking long-term value accretion beyond standalone capabilities.

Going forward investors should closely watch:

- Contract backlog shifts particularly new wins in offshore renewable energy space.

- Timing and completion status of Saltchuk merger including regulatory developments.

- Changes in federal infrastructure budgets influencing coastal capital spending trends.

- Fleet utilization rates alongside capex efficiency supporting operational margins amidst fluctuating input costs.

This analysis is intended solely for informational purposes based on publicly available data without provision of investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments