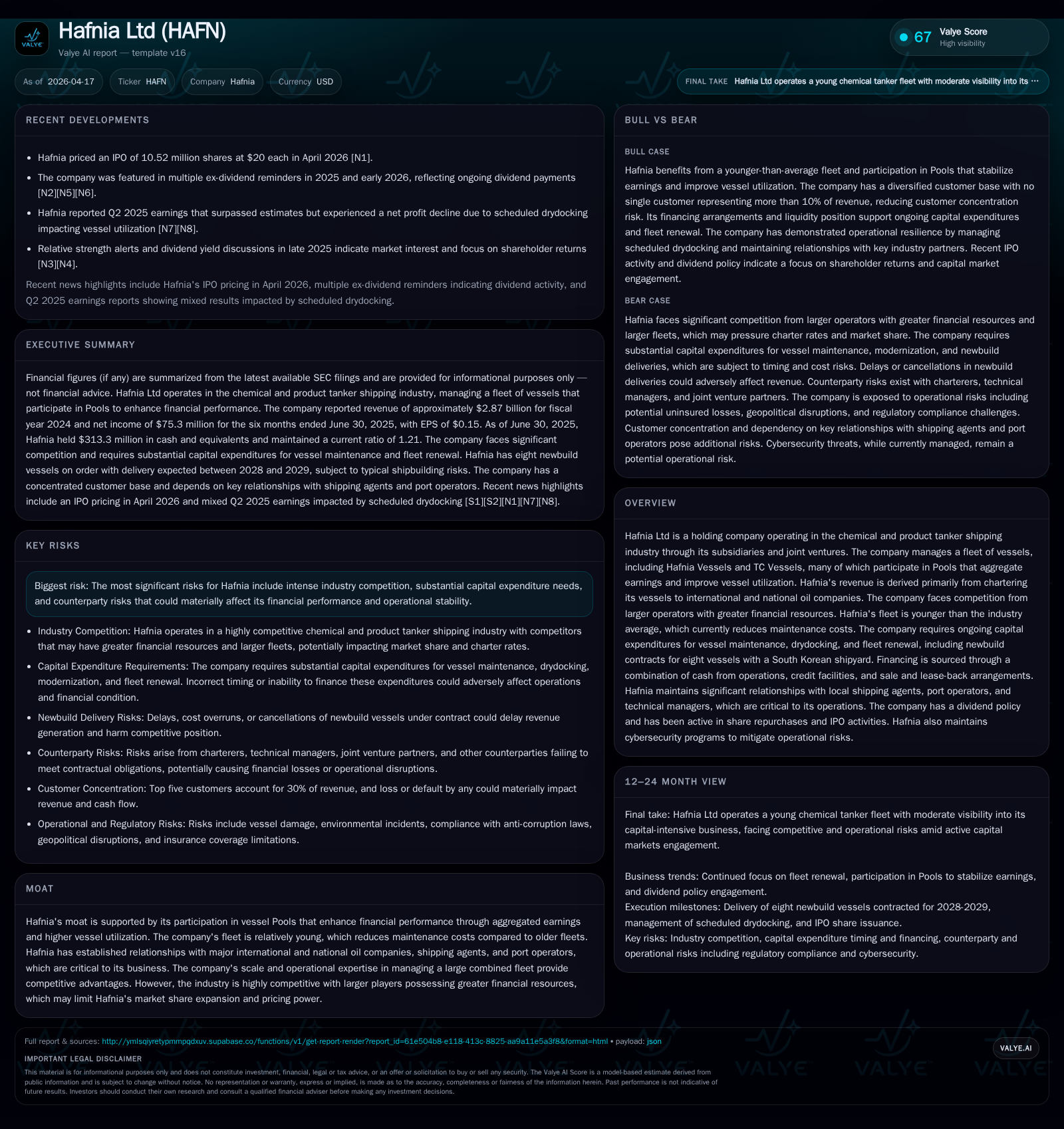

Hafnia Ltd's Strategic Moves in the Chemical and Product Tanker Market

Hafnia leverages a young fleet and pooling partnerships to sustain growth amid capital-intensive industry challenges.

Hafnia Ltd operates a relatively young fleet of chemical and product tankers, benefiting from lower maintenance costs and engaging in Pools that aggregate earnings and stabilize utilization. The company’s revenue growth through 2024 was driven by fleet expansion, pool participation, and favorable post-2022 tanker market conditions. While market volatility and geopolitical disruptions pose risks, Hafnia manages its capital structure with diversified credit facilities and sale-and-leaseback arrangements. Shareholder returns are supported by strong ROE and consistent dividends, though future growth depends heavily on newbuild deliveries and evolving freight rate dynamics.

Fleet Expansion and Revenue Growth Trends Through 2024

Hafnia Ltd has demonstrated significant historical growth through fleet expansion and operational efficiency. The company reported annual revenues of approximately $2.87 billion for the year ended December 31, 2024, accompanied by net income of about $774 million [F1]. This performance reflects the combined contribution of an expanding fleet—comprising Hafnia Vessels and TC Vessels—and participation in vessel Pools that collectively enhance earnings stability.

A key competitive advantage for Hafnia is its relatively young fleet, which reduces maintenance costs compared to the industry average. This younger age profile helps lower operational expenditure on drydocking cycles and repairs, positively impacting net margins [S1]. The growth trajectory over recent years has also been supported by favorable tanker market conditions post-March 2022, when elevated freight rates manifested amid tightening global supply-demand balances [S1].

Historical performance (annual)

| FY |

|---|

| 2024 |

Source: SEC companyfacts cache [F1].

Note: Latest full-year figures available as of end-2024.

Market Dynamics Influencing Hafnia’s Operational Performance

Tanker freight rates historically exhibit cyclicality driven by global fuel demand fluctuations, vessel supply, and geopolitical factors. Hafnia's cash flows have been influenced notably by disruptions in major trade lanes such as the Red Sea route closures in early 2025 stemming from regional conflicts [S1]. These events led to temporary shifts in sailing routes towards shorter intra-hemispheric paths, impacting vessel positioning strategies.

Additionally, the crude tanker segment saw a transition in mid-2024 where certain crude tankers shifted into trading clean products due to depressed crude freight rates. Such transitions exerted short-term pressure on Hafnia’s cash flow streams. However, recovery was evident in H2 2025 as crude production increased and sanctioned crude tankers declined in number, allowing LR2 vessels to revert predominantly to crude trades—a movement beneficial to freight rate realization [S1].

Pooling Partnerships: Enhancing Utilization and Income Stability

Central to Hafnia’s business model is its active participation in shipping Pools—collective management entities that aggregate revenues and expenses among member vessels. This arrangement obscures individual vessel volatility by averaging out day-to-day rate swings inherent in the spot market while blending income from longer-duration time charter contracts.

Pools employ revenue-sharing formulas that allocate net earnings based on agreed parameters factoring vessel size, age, utilization, and cargo type carried [S1]. By integrating assets into Pools alongside proprietary managed vessels (the Hafnia Vessels), the company maximizes overall utilization rates—an essential metric given the perishable nature of voyage earnings in this sector.

This Pooling approach shields Hafnia somewhat from exposure to abrupt spot market downturns but maintains access to upside when market conditions improve. It also enables more predictable cash flow timing critical for managing capital-intensive obligations.

Capital Structure and Liquidity Deep Dive: Managing Debt & Credit Facilities

As of December 31, 2025, Hafnia’s total outstanding debt under its principal credit facilities was approximately $1.06 billion [S5]. This group of secured revolving credit facilities and term loans supports vessel acquisitions, drydocking commitments, working capital needs, and general corporate purposes.

Key facilities include:

- A $715 million reducing revolving credit facility maturing July 2032 with a current outstanding balance of $637 million [S7].

- A $473 million senior secured term loan facility maturing September 2026 with a balance near $50 million at year-end [S7].

- A recently arranged $303 million undrawn revolving facility maturing February 2029 [S4].

Interest rates across these facilities are floating based on daily non-cumulative compounded SOFR plus margins that adjust depending on utilization levels. Notably, sustainability-linked margin adjustments can reduce or increase loan costs up to five basis points depending on adherence to defined Fleet Sustainability Score metrics verified by DNV [S4].

Hafnia held cash and equivalents of about $313 million as of June 30, 2025 [F1], complementing its liquidity position alongside these committed credit lines. The company also employs sale-and-leaseback arrangements effectively reducing upfront cash CAPEX burdens but obligating future lease liabilities accounted under IFRS standards.

Financial covenants across loans include liquidity ratios, maximum leverage thresholds, collateral maintenance via first-priority mortgages over specific vessels, earnings assignments from those assets, account pledges for collection accounts related to pools’ freight receivables, and limitations on dividend payments conditional on covenant compliance . As at the date of reporting, Hafnia was compliant with all covenants.

Returns to Shareholders: ROE, Dividends, and Share Repurchase Strategy

Hafnia reported an approximate Return on Equity (ROE) of 34.2% for the latest full-year period ending December 31, 2024 [F1], signaling substantial capital efficiency relative to industry norms. This robust profitability arises from disciplined cost management combined with operational leverage inherent in tanker charters during tight market conditions.

Dividend policy remains intact with regular payouts; although exact dividend amounts are not detailed publicly for this period [N2], ex-dividend dates have been announced consistently. There is no explicit confirmation regarding active share repurchase programs within recent filings or disclosures [N2][S1].

Navigating Geopolitical Disruptions and Industry Competition

Hafnia operates within an industry acutely sensitive to geopolitical developments. The ongoing ramifications of the Russia-Ukraine conflict have introduced sanctions affecting Russian crude oil exports and forced rerouting that disrupted traditional trade flows [S1]. More recently, tensions in the Middle East have led to intermittent interruptions in critical maritime chokepoints like the Red Sea corridor.[S1]

These factors compel nimble deployment decisions across their fleet spectrum between clean chemical products and heavier crude cargos while exposing revenue streams to counterparty risks among major oil companies dependent on shifting supply chains.

Competition remains fierce as larger shipping conglomerates wield greater financial muscle enabling volume discounts or absorbing freight rate downturns more flexibly than mid-sized players like Hafnia [S1]. Nevertheless, Hafnia leverages operational expertise from managing pooled vessels combined with customer relationships predominantly comprising international/national oil companies.

Outlook: Investment Commitments, Fleet Renewal, and Market Indicators to Monitor

Looking forward into 2026 onwards: Hafnia has active contracts for eight newbuild chemical/product tankers being constructed at a South Korean shipyard—a strategic move aimed at maintaining fleet modernity while curbing long-term maintenance CAPEX pressures [S1].

Recent equity issuance via IPO raised approximately $210 million [N1], likely earmarked for further debt reduction or newbuild financing supporting fleet renewal ambitions.

Key indicators warrant monitoring include:

- Progression in delivering newbuild vessels expanding capacity or replacing older tonnage.

- Freight rate trends distinguishing spot versus time charter segments affecting revenue mix volatility.

- Evolution in geopolitical stability impacting trade route accessibility.

- Market absorption capacity vis-à-vis increasing regulatory environmental demands influencing tanker design specs.

- Impact from potential consolidation or partnerships arising from Hafnia’s stake acquisition in TORM plc as per SEC commentary shaping shareholder value creation pathways [S1].

In sum, while capital-intensive requirements persist along with exposure to volatile tanker markets exacerbated by geopolitical uncertainties, Hafnia’s strategic focus on pooling partnerships combined with disciplined financial management appears well positioned to sustain competitive presence within its niche segment.

This analysis synthesizes information solely available through cited filings ([F1], [N#], [S#]) as of April 17th, 2026. It does not constitute investment advice but aims to provide comprehensive insight into Hafnia Ltd's operational context and financial positioning within the chemical/product tanker shipping sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments