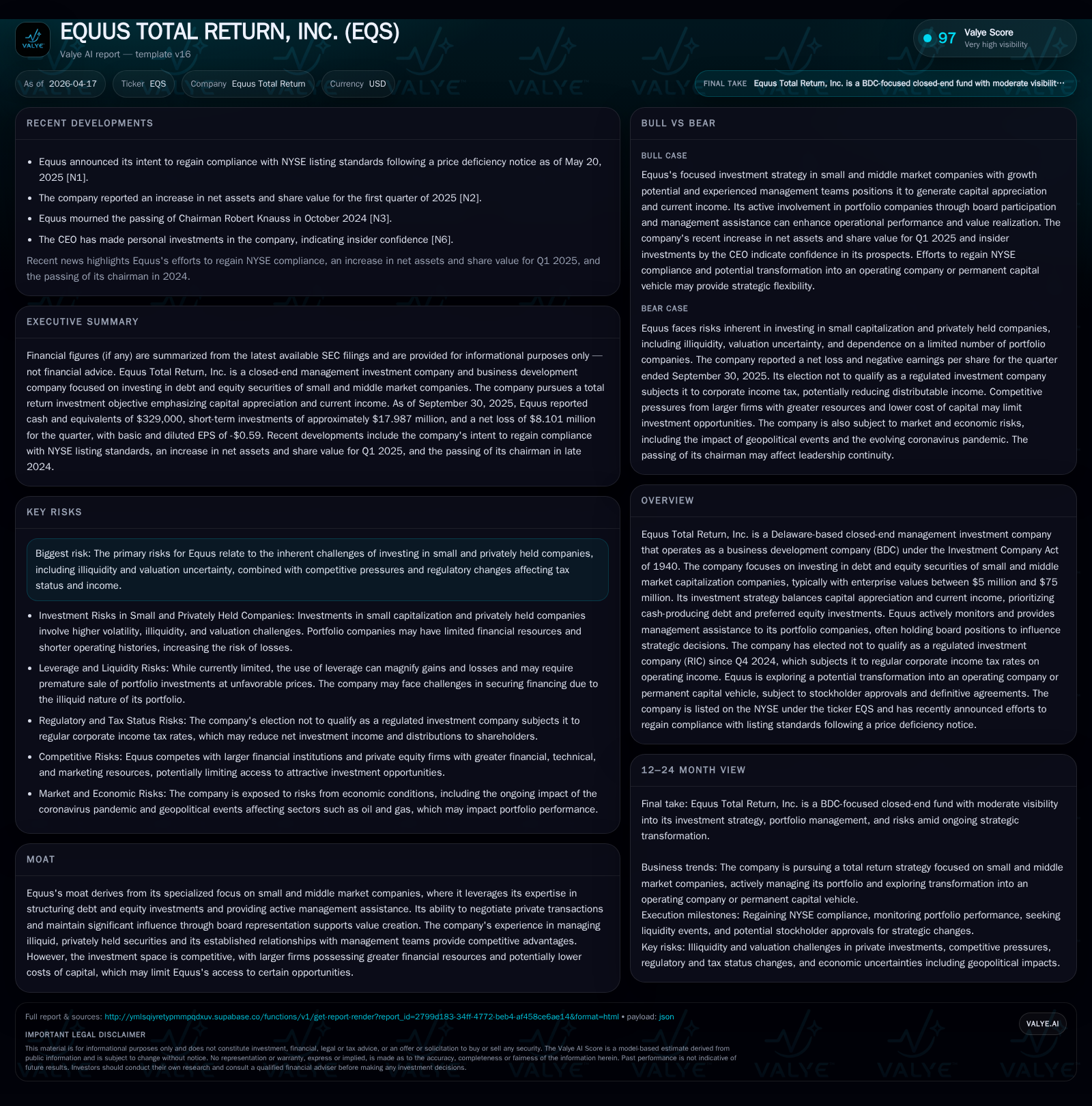

Equus Total Return’s Financial Reversal: From Net Income Losses to Operating Cash Flow Strength

An in-depth analysis of Equus Total Return's shifting financial dynamics, tax regime change, and strategic repositioning in the small-to-middle market investment space.

Equus Total Return, Inc. has experienced a pronounced financial reversal from positive net income in 2023 to significant losses in 2024, juxtaposed with a remarkable recovery in operating cash flow over the same period. This discrepancy underscores nuanced shifts in earnings quality driven by portfolio performance, valuation methods, and the company's strategic investment approach focused on small and mid-cap private companies. The election to forego regulated investment company status since late 2024 introduces corporate income tax implications that could pressure net returns amid liquidity constraints and competitive financing challenges. Active governance and management assistance remain key components of Equus's value creation model, yet risks persist around illiquidity, valuation uncertainty, and intensifying competition. The company's pending transformation into an operating entity marks a critical inflection point to watch.

Financial Performance Turnaround: Decline in Net Income Amid Operating Cash Flow Growth

Equus Total Return’s recent financial results display a striking divergence between net income and operating cash flow over the past three years. According to company filing data [F1], net income plummeted from a positive $12.95 million at fiscal year-end (FYE) 2023 to a loss of $18.77 million in FYE 2024—a decline of approximately 245%. Despite this sharp net income deterioration, operating cash flow strengthened markedly by 174%, rebounding from negative cash flows of -$51.36 million in 2023 to positive $38.23 million by end of 2024.

This dissonance signals considerable volatility in earnings quality that stems primarily from fair value adjustments on illiquid private equity and debt investments—a typical feature in BDC portfolios lacking liquid market pricing [S1][S28]. Management adopts a fair value framework that incorporates internal valuations possibly without broad third-party appraisal consensus [S12], catalyzing substantial unrealized losses or gains recognized in net income but not immediately reflected in cash flows. Hence, while the company’s operational cash generation capacity shows recovery—likely improving interest collection and preferred dividends—the headline accounting earnings remain under pressure due to mark-to-model impairments or reversals.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2024 | -19 | 38 | -245.0% |

| 2023 | 13 | -51 | +1248.0% |

| 2022 | -1 | -8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2024 | -51.6 |

| 2023 | 26.8 |

| 2022 | -3.2 |

Source: SEC companyfacts cache [F1].

Source: [F1].

The approximately -51.6% ROE calculated for 2024 further highlights operational strains compounded by diminished equity base relative to losses sustained [F1]. Such financial behavior illustrates the complexities BDCs face reconciling accrual accounting volatility with actual cash-generative performance.

Investment Approach Targeting Small and Middle Market Companies

Equus Total Return explicitly targets investments within private companies exhibiting total enterprise values ranging broadly from $5 million up to $75 million [S1][S6]. Its portfolio combines debt instruments—including subordinated loans convertible into equity—and preferred equity securities structured through bespoke private market transactions [S6]. This specialization allows Equus to participate in niche segments often underserved by larger public funds or traditional lenders.

A defining feature of Equus’s strategy encompasses active management assistance and governance involvement to safeguard capital appreciation prospects while maintaining recurring income streams from coupon payments or preferred dividends [S7]. Management routinely secures board representation or equivalent governance rights enabling influence over strategic direction such as capital structure optimization or acquisition strategies—a mechanism described as management-assisted governance [S6][S7]. Equity co-investment alongside other private equity groups reflects additional syndication typical within middle market deals.

This hands-on approach necessitates rigorous due diligence protocols incorporating background checks on management teams’ track records alongside assessments of market positioning and growth potential within target sectors [S5][S6]. The company also prioritizes portfolio companies demonstrating prospective returns or historical profitability sufficient to support reliable distributor payments [S6].

Impact of Election to Forego RIC Status and Tax Implications

A pivotal development in Equus’s structural dynamics is its Q4 2024 election to discontinue qualification as a regulated investment company (RIC) under tax code provisions [S1][S27]. Previously aligned as a RIC benefiting from pass-through taxation that exempted most investment income from federal corporate taxes (absent retained earnings), this change triggers exposure to standard corporate income tax rates going forward.

This decision introduces material tax expense burdens affecting net investment returns available for distribution or reinvestment. Consequently, distribution policies face pressure since taxable income reduces retained cash flows post-tax for dividend sustainability [S27]. While the firm retains discretion regarding potentially seeking requalification as a RIC later—subject to satisfying applicable diversification and distribution criteria—this transition differentiates its investment return profile versus peer BDCs maintaining RIC status.

From an operational perspective, this new tax treatment may influence future capital allocation decisions including increased focus on tax-efficient investment vehicles or consideration of more frequent realization events [S27]. It further complicates leverage usage economics since interest expenses become more consequential when offset against taxable earnings.

Leverage Usage and Liquidity Challenges in an Illiquid Portfolio

Equus operates under stringent regulatory leverage limitations codified under the Investment Company Act Section governing BDCs: specifically maintaining minimum asset coverage ratios of at least 150% post-borrowings [S4][S11][S20]. However, leveraging private-market securities collateral remains fraught given inherent illiquidity and valuation uncertainties hindering conventional credit underwriting.

Historically reliant on revolving credit facilities—recently expiring—and margin accounts facilitating quarterly diversity requirements for pass-through tax qualification [S3], Equus currently pursues alternative financing avenues including asset sales and incremental debt/equity issuances to sustain liquidity [S3][S23]. The expiration of prior credit lines elevates refinancing risk amidst ‘spread compression’ conditions documented across credit markets where borrowing costs rise while yields tighten on new investments [S4][S20]. Such compression detracts from net interest margins fundamental to the BDC model.

Additionally, many portfolio companies carry senior secured debt with intercreditor agreements subordinating Equus’s liens thereby diminishing collateral control upon borrower distress scenarios [S18]. This structurally caps recovery expectations limiting downside protection measures inherent with secured loan positions.

Capital Allocation: Dividends, Buybacks, and Return on Equity Evaluation

Capital stewardship reveals constrained flexibility amid operating losses disclosed for FY24 [F1][S19]. Dividend distributions are contingent on realized income flows complicated by newly imposed corporate taxes reducing distributable earnings pool [S27]. Buybacks occur opportunistically aiming to counteract share-price discounts relative to NAV but are not mandated or extensive given liquidity priorities [S19].

The negative ROE underscores persistent unprofitability suppressing meaningful capital returns absent sizable portfolio exits or valuation recoveries [F1]. Meanwhile, robust CFO figures imply solid operational cash inflows suggesting dividend sustainability depends heavily on ongoing portfolio interest/dividend collection rather than accounting profits.

Capital return capacity remains vulnerable pending resolution on structural reforms including the transformation strategy discussed below.

Management Assistance and Active Governance Driving Portfolio Value

Active management sets Equus apart within the middle market private equity universe where institutional hands-off models prevail [S6][S7]. Officers frequently hold board seats enabling direct influence over pivotal business decisions encompassing strategic acquisitions, budget oversight, capital raising initiatives and executive incentive alignment via stock-based compensation plans.

Such managerial engagement enhances downside risk mitigation through proactive problem resolution at portfolio companies while fostering alignment around growth objectives enhancing long-term appreciation prospects—hallmarks of ‘‘management-assisted governance.’’ This modality also facilitates nuanced monitoring unattainable via purely passive holdings given limited public disclosure among private firms.

Through contractual rights embedded in investment terms—as well as practical board oversight—Equus strives to shape enterprise trajectories consistent with shareholder interests while providing value-add beyond mere capital provision.

Risks Surrounding Valuation, Illiquidity, and Competitive Pressures

Risk factors loom prominently given the intrinsic challenges investing predominantly in small privately held businesses fraught with volatility stemming from limited operating histories constrained product lines heightened sensitivity to economic downturns plus sparse public information availability [S1][S16].

Valuation is particularly subjective—the company acknowledges that fair value estimates can materially deviate from realizable exit prices due to absence of widely accepted market evidence or trading activity necessitating modeling assumptions prone to bias or error [S12][S28]. These factors amplify NAV fluctuations disproportionately affecting reported earnings volatility.

Illiquidity intensifies funding constraints contributing to difficulties meeting leveraged borrowing covenants if spreads narrow or refinancing options diminish prompting potential forced sales at depressed prices adversely impacting asset values [S22][S24]. Compounding pressures arise from increasingly crowded competition featuring larger institutions possessing lower cost capital enabling aggressive bidding thereby compressing yields available for Equus targeting same segment niches [S9][S21].

Regulatory uncertainties related principally to tax qualification morph election outcomes represent additional headwinds potentially exacerbating periodic underperformance risks until transformation plans materialize fully [S25][S26].

Future Outlook: Strategic Initiatives and What Investors Should Watch

Management continues exploring options focused on transformative initiatives designed either around merging/acquiring operating companies primarily within energy/natural resources/technology/financial services sectors or converting the fund into a permanent capital vehicle ceasing BDC categorization entirely subject again to shareholder approval votes prior to any execution steps [S11][S17][S27].

While no formal guidance or forecast milestones are disclosed outright beyond these ongoing strategic reviews—in line with prudent reporting practices—key areas warrant close observation:

- Progress towards securing shareholder authorization enabling BDC election withdrawal;

- Identification or announcement of definitive transaction counterparties;

- Movements towards expanded liquidity sources easing refinancing pressure;

- Stabilization or improvement trends within portfolio valuations influencing net income trends;

- Initiation of renewed dividend resumption programs signaling confidence revival;

- Potential requalification applications for RIC status reducing tax drag impacts. These factors collectively will provide directional clarity regarding whether current structural headwinds facing Equus can abate sufficiently enabling durable financial recovery aligned with original shareholder total return objectives.

Disclaimer: This analysis is based solely on information contained within publicly filed SEC documents dated April 2026 and CompanyFacts data snapshots up through September 2025. No projections or investment recommendations are offered herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments