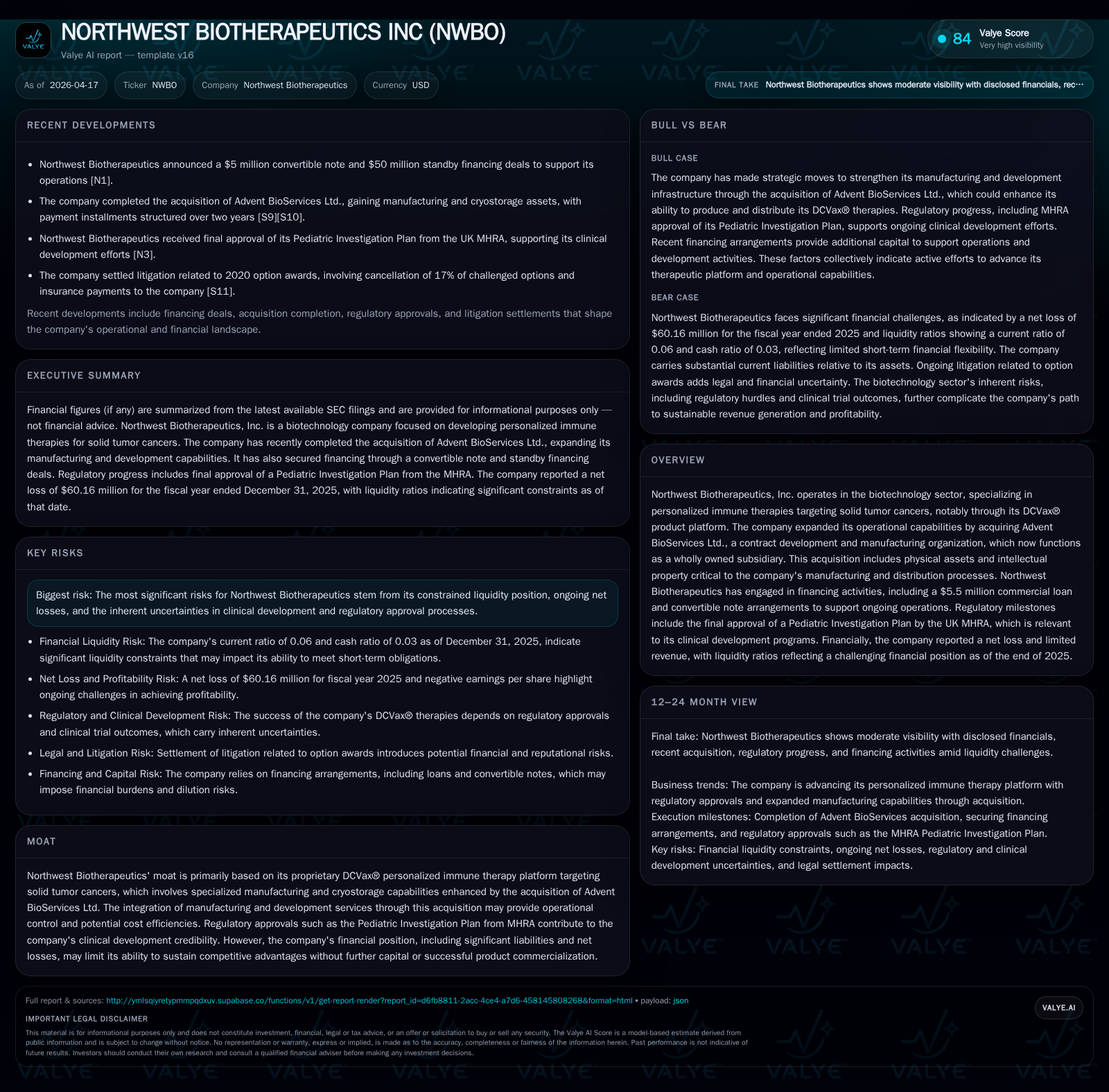

Northwest Biotherapeutics’ Struggle to Translate Immune Therapy Innovation into Profit

NWBO advances personalized cancer vaccine technology and manufacturing but faces substantial financial headwinds.

Northwest Biotherapeutics utilizes its proprietary DCVax® dendritic cell vaccine platform to target solid tumor cancers, aiming for a breakthrough in personalized immunotherapy. The company's strategic acquisition of Advent BioServices Ltd. integrated contract manufacturing and cryostorage capabilities, reinforcing operational control and potential efficiencies. Despite modest revenue growth averaging nearly 15% year-over-year from 2020 to 2023, NWBO continues to incur deep operating and net losses exacerbated by strained liquidity and high current liabilities. The firm’s financial sustainability depends on successful regulatory milestones, capital raises, and managing its steep cash burn.

Unique DCVax Platform: Scientific Promise Meets Clinical Realities

Northwest Biotherapeutics centers its business model on the DCVax® platform — a proprietary personalized immune therapy designed as a dendritic cell vaccine targeting solid tumor cancers. This approach leverages patient-derived dendritic cells programmed to stimulate an immune response against tumor antigens, aiming for precision in cancer immunotherapy that bypasses one-size-fits-all drug formulations [S1]. The complex nature of this personalized therapy demands rigorously controlled manufacturing processes, including cryostorage technology critical for preserving cell viability pre-administration.

The acquisition of Advent BioServices Ltd., a UK-based contract development and manufacturing organization (CDMO), significantly enhances NWBO’s operational moat by embedding manufacturing capacity and associated intellectual property within the company structure [S3][S8]. Advent brings not only physical assets but also the specialized know-how in handling personalized dendritic cell vaccines and supporting qualities like GMP compliance and cold chain logistics — elements indispensable for scaling production without compromising clinical integrity.

Combining discovery-stage clinical technology with CDMO capabilities aligns with industry trends where biotech firms seek vertical integration to reduce outsourcing risks, improve quality control, and potentially lower cost per unit during product scale-up. However, despite these technical advantages, translating such complex therapies from experimental stages to widespread commercial adoption remains fraught with clinical and regulatory challenges.

Growth Trajectory from 2020 to 2023: Revenue Gains amidst Operating Losses

NWBO’s top-line tells a story of gradual traction in sales, albeit on a modest absolute scale characteristic of early-stage biotechs focusing on niche immunotherapies. Revenues rose from $1.29 million in FY2020 to $1.93 million in FY2023, reflecting compound annual growth supported by expanded service offerings linked partially to Advent's prior contracts [F1]. The latest annual growth rate stands at approximately +14.8% year-over-year.

However, these sales figures exist against the backdrop of persistent operating losses which have remained sizable throughout this period: operating income slid between −$55 million to −$67 million annually from FY2022 through FY2024 [F1]. Net income parallels these losses with no indication yet of profitability.

This disparity stems largely from fixed R&D expenditures required for advancing clinical trials combined with the costs of maintaining specialized manufacturing infrastructure—costs that biotechnology companies face before achieving commercialization scale or regulatory approvals that enable market access [F1]. The structural cash burn underscores the heightened risk profile typical for companies developing personalized therapies with long development cycles.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -60 | -45 | -60 | +28.2% | ||

| 2024 | -84 | -57 | -67 | -33.8% | ||

| 2023 | 1932000 | -63 | -54 | -56 | +14.8% | +40.4% |

| 2022 | 1683000 | -105 | -53 | -67 | +67.5% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 99.8 |

| 2024 | 88.7 |

| 2023 | 95.2 |

| 2022 | 82.0 |

Source: SEC companyfacts cache [F1].

Table summarizes NWBO's historical financials emphasizing steady revenue increases amidst ongoing heavy losses.

Advent BioServices Acquisition: Strengthening Manufacturing Capabilities

In October 2025, Northwest Biotherapeutics completed the acquisition of Advent BioServices Ltd., transitioning this previously contracted partner into a wholly owned subsidiary [S3][S10]. This move subsumes Advent’s physical assets—including extensive cryostorage equipment—and their intellectual property portfolio directly under NWBO’s control.

Strategically, owning a dedicated CDMO facilitates tighter integration over product development timelines, critical for personalized vaccines requiring seamless coordination between patient sample collection, cell processing, storage, and delivery [S8]. This vertical integration may enable cost efficiencies through eliminating margin leakage inherent in outsourcing relationships while consolidating quality oversight under one governance framework.

Noteworthy is the related-party aspect of this transaction: the Company's CEO Linda Powers holds controlling interests in the selling entity [S8]. The company procured waivers from SEC regulations concerning financial disclosures typically mandated for such acquisitions — reflecting regulatory acknowledgment of complexities in these interrelated transactions.

The purchase price agreed upon approximates £1.4 million (~$1.9 million), payable via installments over two years post-closing with interest accruing at roughly 7.5% annually [S10]. Further consideration involved settling pre-existing accounts payable owed to Advent totaling about $8.3 million [S10].

This acquisition consolidates critical supply-chain elements pivotal for NWBO’s immunotherapy lifecycle management while tying up significant financial commitments amid already strained liquidity metrics.

Clinical and Regulatory Milestones Supporting Future Prospects

Regulatory progress anchors NWBO’s pathway forward as they seek to translate their DCVax® platform’s promise into commercial success. An important milestone includes final approval by the UK Medicines and Healthcare products Regulatory Agency (MHRA) for a Pediatric Investigation Plan related to their clinical pipeline [S1]. This approval validates aspects of NWBO's methodology aligning with pediatric oncology trial requirements — an encouraging signal regarding regulatory alignment.

While pediatric indications represent an extension rather than the core adult oncology market focus, such approvals enhance NWBO’s credibility within regulatory frameworks across jurisdictions and could streamline later-stage trial design.[S1]

No explicit near-term commercialization forecasts are presented; progress remains heavily contingent on ongoing trials’ outcomes and broader regulatory clearance decisions essential before billable products can be commercialized at scale.

Liquidity Constraints and Capital Structure Pressures

NWBO faces acute liquidity stress as reflected in its financial position as of December 31, 2025: current assets stand at approximately $5.5 million against current liabilities nearing $91.7 million — yielding a razor-thin current ratio near 0.06 [F1]. Cash reserves are limited at about $3 million [F1], insufficient to cover a meaningful fraction of impending obligations without fresh capital influx or improved cash flows.

To support ongoing operations amid tight liquidity, NWBO secured a commercial loan facility totaling $5.5 million from Streeterville Capital LLC at an annual interest rate of 8%, signed October 27, 2025 [S7]. Principal repayments do not begin until June 26, 2026; following which amortization spreads across fourteen monthly installments at slightly elevated amounts (110% pro rata), including accrued interest — evidence of tight but structured debt servicing conditions.

Additionally, related metrics reveal sizeable accrued liabilities likely tied to timing mismatches between expenses incurred for pivotal development activities versus receipts under contracts or financing arrangements.

This imbalance poses significant refinancing risk typical among biotechnology firms pre-profitability stage — with very limited operating cash inflows heavily reliant on external financing or milestone-triggered payments.

Operating Cash Flow and Capital Expenditure Trends

Cash flow statements mirror the challenging operational landscape: fiscal year ended December 31, 2025 saw net cash used in operating activities reach −$44.76 million compared to −$53.64 million just two years prior [F1], highlighting continued cash consumption inherent in sustaining R&D intensity alongside operational demands.

Capital expenditure increased notably around FY2025 to approximately $1.5 million — a substantial rise relative to minimal capex levels reported historically [F1] likely attributable to investments for integrating Advent BioServices’ fixed assets or upgrading manufacturing infrastructure tailored for DCVax® production scalability.

Consequently, free cash flow mirrors this large negative gap approaching −$46 million when subtracting capex from operating cash flow – underscoring formidable capital intensity requirements amid nascent commercialization prospects [F1].

Management must carefully calibrate investment pacing with runway extension strategies given the rapid depletion profile typical for CDMO-driven personalized therapy producers where upfront costs precede any licensed product revenue generation.

Shareholder Returns and Capital Allocation Strategy

NWBO currently does not distribute dividends nor engage in share repurchase programs as its capital allocation focuses squarely on growth investments necessary for drug development progression and operational continuity [F1][S8].

Notably post-Advent acquisition activity included cancellation of approximately 5.5 million stock options previously issued as compensation for services rendered by Advent personnel — retirement actions intended to optimize treasury stock holdings without dilution expansion [S8].

Such maneuvers demonstrate prioritization of prudent share capital management alongside maintaining sufficient incentive alignment tools within constrained financing environments that typify early-stage biotech enterprises devoted primarily to innovation pipelines rather than shareholder yield generation.

Key Risks and Litigation Impact on Strategic Direction

With clinical pipelines inherently uncertain and near-term profitability distant, network effects rely heavily on successful trial outcomes coupled with continuous funding availability — both sensitive risk factors highlighted extensively by NWBO’s SEC filings [S4][S10][S19].

Litigation risks materialized around option awards distributed in fiscal year 2020 led to settled disputes filed against management and directors regarding equity compensation practices [S5][S6]. A settlement agreement reached end-2025 resulted in insurance payments amounting to $2.25 million credited back to the company alongside cancellation of contentious option tranches approximating seventeen percent of those awards issued [S5][S6].

While removing lingering legal uncertainty improves governance clarity moving forward, such episodes reinforce governance-related challenges amid tight resource allocation balancing acts across board oversight responsibilities within small-cap biotechs navigating rapidly evolving corporate structures paired with complex acquisitions like Advent BioServices.

Looking Ahead: Milestones to Watch and Financial Sustainability

Absent explicit financial guidance or detailed milestones disclosed publicly beyond regulatory updates like MHRA approvals or clinical trial advancements (e.g., interim efficacy data releases), observers should focus attention on:

- Progression status of DCVax®-L pivotal trials especially those influencing US FDA or EMA review timelines;

- Timing and conditions triggering accelerated payments related to Advent acquisition installment obligations;

- Quarterly liquidity metrics signaling changes in cash runway length considering current debt amortization schedules;

- Potential new financing rounds or partnerships mitigating refinancing risks inherent under current capital structure constraints;

- Adjustments or expansions in commercial manufacturing capacity facilitated by Advent subsidiary integration impacting cost structure efficiency.

Collectively these indicators will frame whether Northwest Biotherapeutics can reverse entrenched loss trends toward eventual self-sustaining operations centered around its innovative immunotherapy platform — an outcome still uncertain given prolonged losses exceeding tens of millions annually coupled with scarce liquid resources currently reported.

Disclaimer: This report synthesizes public SEC filings up through April 17, 2026; it does not constitute investment advice or an endorsement but intends analytical commentary based solely on disclosed data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments