Eline Entertainment Group: From Dormancy to Deal-Maker Ambitions

Examining EEGI’s revival from halted operations toward merger-driven growth amid financial fragility.

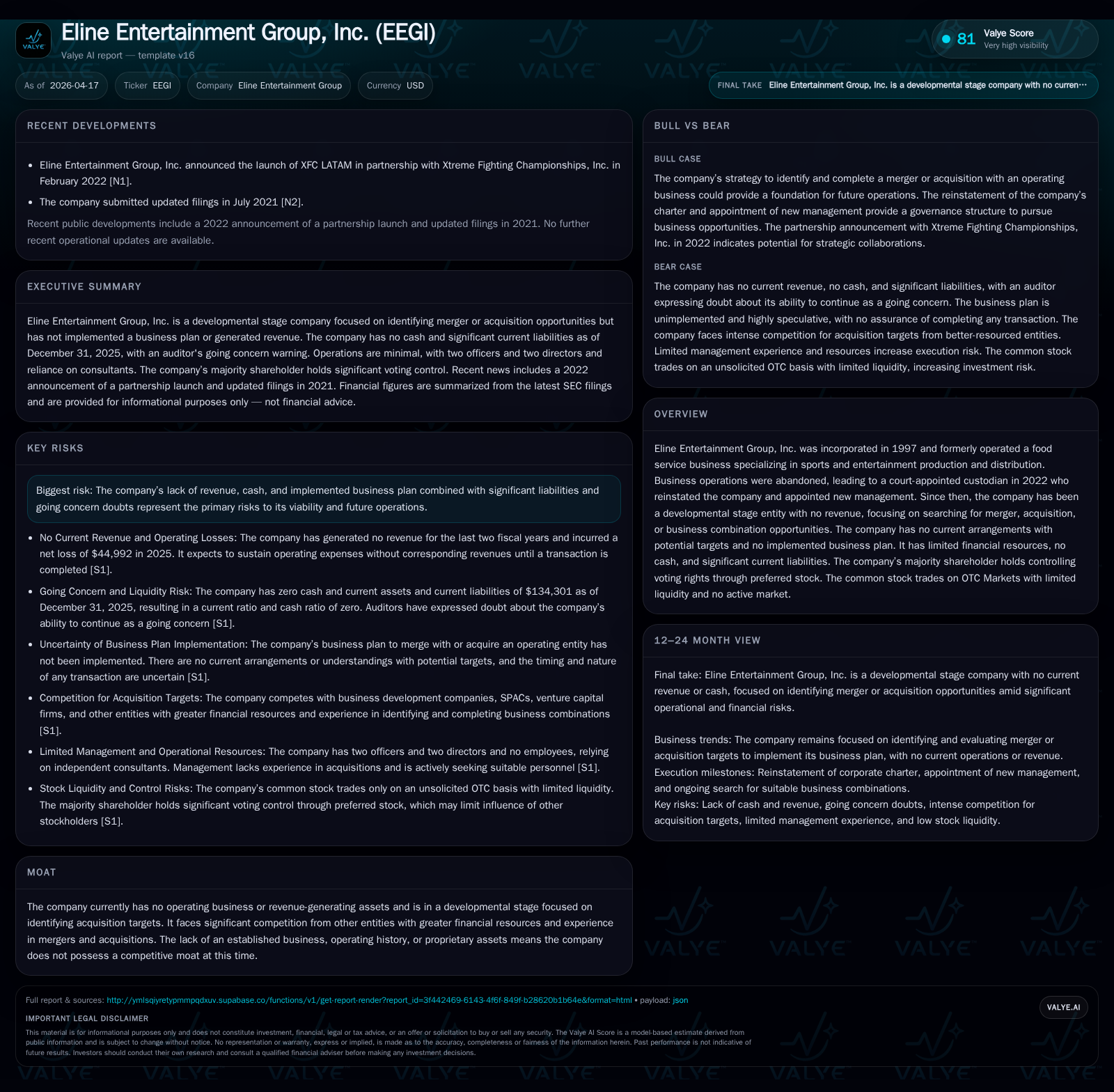

Eline Entertainment Group, Inc. (EEGI) transitioned from business abandonment and court-appointed custodianship in 2022 to a developmental-stage entity focused on sourcing merger or acquisition opportunities. The company currently has no revenue, active business operations, or formal targets, operating under severe liquidity constraints and significant liabilities that cast doubt over its viability. Management’s strategic outlook hinges on successful capital raises and deal completions to transform the company’s prospects, yet competition and resource limitations pose substantial challenges. Monitoring key milestones such as funding events and transaction announcements will be critical for assessing progress.

Historical Performance and Financial Decline: The Road to Custodianship

Eline Entertainment Group, Inc.'s financial narrative since 2022 substantiates a company grappling with operational cessation and financial deterioration. Historically engaged as a food service provider specializing in sports and entertainment production, the company abandoned operations prior to custodianship in 2022 [S1], [S16]. This abandonment triggered a court-appointed custodian's intervention due to the absence of a functioning board and revocation of the corporate charter [S1], [S16].

The company's financials reveal consistent zero revenues over the past four fiscal years ending 2025 [F1]. Operating income declined from -$21,214 in 2022 to -$44,992 in 2025, evidencing worsening losses by mid-double-digit percentages annually (-26.3% YoY operating income decline in the latest reported year) [F1]. Net income mirrors this trend with losses amplifying similarly [-$21k in 2022 to -$44k in 2025; -36.8% YoY decline] [F1]. Operating cash flow has remained negative throughout this period, reaching nearly -$49k at the end of 2025 [F1]. No capital expenditures have been recorded since at least FY2022, underscoring the lack of reinvestment into ongoing operations or assets [F1].

This financial trajectory reflects not only operational dormancy but also an intensification of liabilities over assets culminating in custodianship. The custodian engaged to rectify corporate governance vacuums undertook actions such as reinstating the company's charter and settling outstanding debts through self-funding measures [S11]. Nonetheless, historical financial attrition shaped the necessity for such judicial oversight.

Historical performance (annual)

| FY | Rev | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -44992 | -49191 | -44992 | -36.8% |

| 2024 | 0 | -32877 | -37220 | -35627 | +39.0% |

| 2023 | 0 | -53931 | -26035 | -53931 | -154.2% |

| 2022 | 0 | -21214 | -2501 | -21214 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 33.5 | |

| 2024 | 36.8 | |

| 2023 | -26035 | 95.6 |

| 2022 | -2501 | 848.2 |

Source: SEC companyfacts cache [F1].

Current Operational Status: A Developmental Stage Company with No Revenue

Post-custodianship, EEGI describes itself as a "developmental stage company" without active business operations or revenue streams [S1], [S16]. Management's efforts have pivoted exclusively toward identifying potential mergers, acquisitions, or other business combinations—a strategic shift away from their historical food service roots.

Despite this strategic realignment commenced since May 2022 [S3], the company has yet to enter into any binding agreements or arrangements concerning target acquisitions [S10]. The absence of an implemented business plan concretizes the developmental nature of current operations [S1]. It anticipates that any future business combination may take multiple legal forms—including mergers, joint ventures, or asset purchases—without definitive indications at this time regarding sector focus or geographic restrictions [S3].

Such a stage imposes significant challenges in forecasting performance with all growth prospects contingent on consummating suitable transactions—a probabilistic task given the landscape. As EEGI lacks an operating business model presently generating cash flows or profits, monitoring future progress depends highly on executed transactions.

Capital Structure and Liquidity Constraints: A Thin Financial Cushion

According to combined SEC filings and financial data up to December 31, 2025 [F1], [S4], [S14], liquidity remains critically strained. End-2024 cash balances were effectively nil while year-end current assets dropped to zero against current liabilities exceeding $134k—resulting in a zero current ratio signaling acute short-term solvency risk.

The company’s equity base is negative approximately $134k as of FY2025 reflecting accumulated deficits consistent with ongoing losses [F1]. These structural imbalances provoke going concern qualifications noted by independent auditors for fiscal years ended in 2024 and 2025 [S1], [S18]. The company explicitly states that without substantial capital infusion it risks operational curtailments or cessation altogether.

Governance is notably influenced by its majority shareholder holding Convertible Series D Preferred Stock granting significant voting rights—up to twenty times that of common stockholders—thus centralizing control which can affect future capital raising strategies and shareholder dilution considerations [S10], [S13]. The authorized but largely unissued share capacity allows flexibility for issuing stock during acquisitions but risks severe dilution.

Strategic Outlook: Acquisition Search Amidst Uncertain Prospects

EEGI’s stated strategic outlook centers on deal sourcing for mergers or acquisitions targeting entities possibly possessing established operational histories [S3], [S10], [S16]. Due diligence efforts are expected to involve rigorous analysis including meetings with incumbent management at target companies and comprehensive review of financials and operational metrics prior to commitments [S5].

However, company disclosures highlight several hurdles inherent to this business development model: intense competition from better-funded entities such as SPACs, private equity firms, venture capitalists, investment banks, and experienced business development companies limit EEGI’s competitive positioning within M&A markets [S19]. The lack of immediate access to funds restricts engagement capability.

The potential utilization of finder’s fees payable via cash or newly issued securities underscores early-stage operating costs accruing before deal closure [S3], [S20]. Additionally, no engagement agreements exist currently with brokers or specialized advisors—suggesting resource constraints and nascent deal infrastructure architecture.

Risks and Challenges: Going Concern, Competitive Pressures, and No Operational Moat

Multiple risk dimensions emerge distinctly. Foremost is the going concern risk underscored by repeated audit reservations given chronic operating losses exceeding $40k annually alongside near-zero liquidity levels threatening continuity absent fresh financing activities [S1], [F1], [S18].

Additionally, EEGI confronts direct competition for acquisition targets from entities bearing substantially greater capital reserves and transaction expertise—compounding difficulties identifying viable opportunities consistent with intended growth pathways [S19]. This weak competitive position is compounded by an absence of proprietary technologies or established assets resulting in no defendable moat.

Investor exposure is magnified by the speculative nature inherent in delimited management experience within acquisition-led growth strategies; failure in securing satisfactory transactions could precipitate value erosion or business discontinuation [S6].

Market trading environment risks also materialize given OTC trading status characterized by low liquidity and volatile pricing unlikely reflective of intrinsic value relevant for shareholder decision-making dynamics.

Capital Allocation and Shareholder Returns: Absence of Dividends and Buybacks

Given persistent negative free cash flow (operating cash outflow approximated at -$49k annually per FY2025) devoid of capex investments observed over recent years ([F1]), Eline Entertainment does not allocate capital toward dividends or share repurchase programs ([S3], [S10]). There is no indication this dynamic will shift absent operational turnaround.

Equity structure adjustments linked to possible issuance during acquisitions may significantly dilute existing shareholders as authorized shares remain plentiful relative to outstanding volumes ([S13]). Capital deployment presently favors operational compliance costs (e.g., audit fees borne by custodianship), corporate reinstatement expenses alongside pre-deal investigative expenditures rather than direct returns ([S11]).

Shareholder influence remains concentrated principally under major stockholder Ms. Chi Ching Hung empowered via preferred stock voting rights controlling corporate policy direction limiting influence from other common shareholders ([S10], [S13]).

What to Watch: Key Milestones in Transaction Identification and Capital Raising

Looking forward from an objective analytical standpoint critical indicators signaling meaningful progress for EEGI will include public announcements regarding:

- Definitive purchase agreements consummating mergers/acquisitions;

- Raised capital tranches addressing immediate liquidity needs;

- Adjustments in capital structure including new equity issuance or debt arrangements;

- Improvements in working capital ratios evidencing alleviated short-term solvency pressures;

- Appointment of specialized deal-making personnel augmenting management expertise;

- Compliance milestones ensuring ongoing regulatory filings without qualification notes.

Due diligence periods typically spanning up to three months post-target identification suggest transaction cadence will be gradual without precipitous developments anticipated imminently ([S20]). Monitoring shareholder meeting disclosures might also illuminate shifts affecting control dynamics consequential for governance stability.

This analysis presents an overview grounded strictly on verified public filings through April 2026 without speculative forecasts beyond stated disclosures. Eline Entertainment Group remains a high-risk developmental entity dependent entirely on infusion of new capital combined with successful acquisitions operating against structural deficiencies highlighted herein.

Disclaimer: This report is prepared solely for informational purposes based on available public data as of April 2026. It does not constitute investment advice nor an endorsement of any security.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments