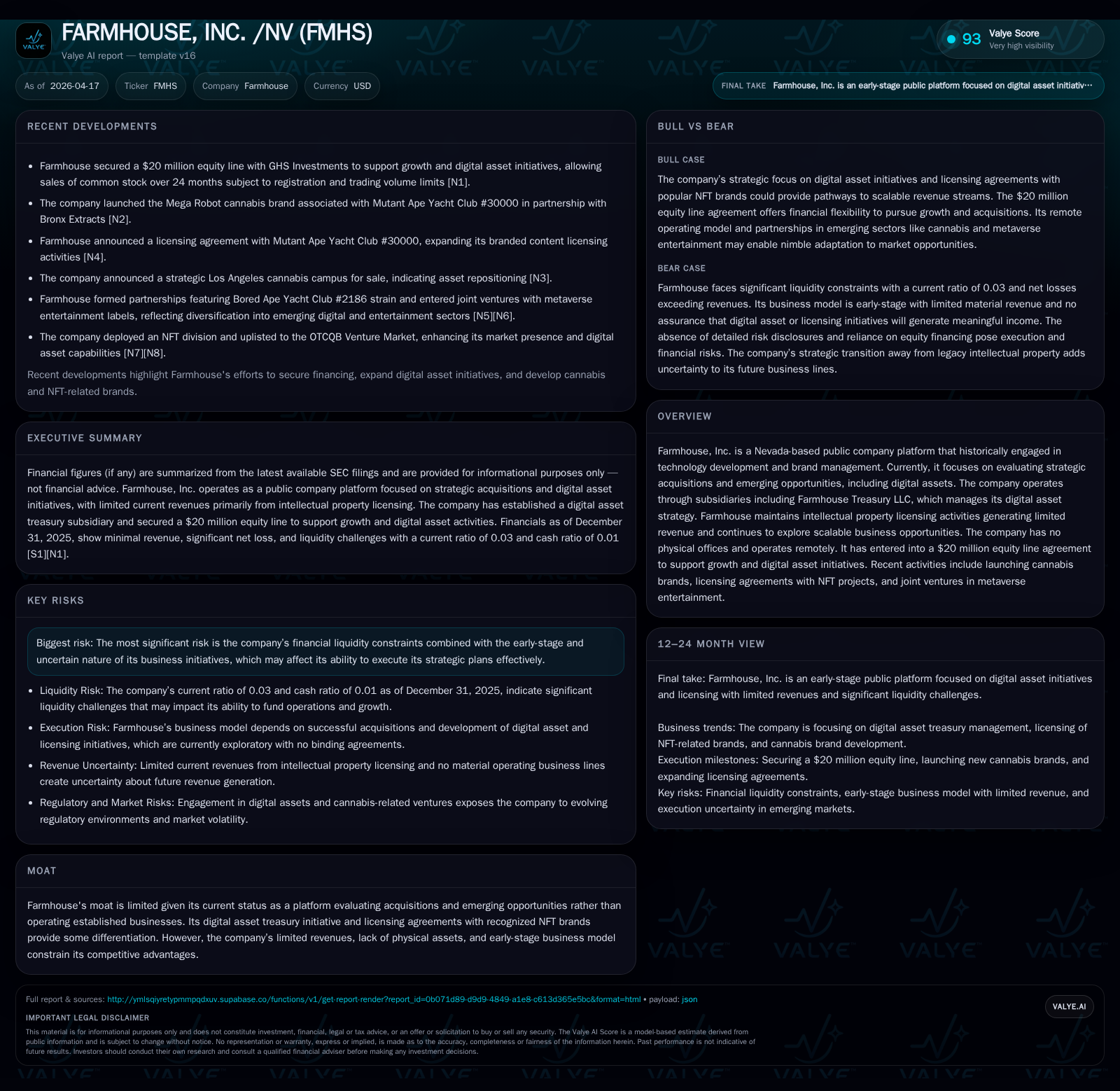

Farmhouse, Inc.’s Shift Toward Digital Assets and Licensing Revenue Challenges

Farmhouse, Inc. pivots from traditional brand licensing to digital asset strategies amid pressing liquidity constraints and limited revenue growth.

Farmhouse, Inc. has transitioned its business focus from historical technology development and brand licensing toward emerging digital asset initiatives managed through its subsidiary Farmhouse Treasury LLC. Despite this strategic pivot, the company’s revenues plummeted by over 85% in FY2025, reflecting the limited scale of its licensing activities and nascent digital ventures. Severe liquidity challenges persist, as evidenced by a 0.03 current ratio and negative equity hovering below $2.7 million at year-end 2025, prompting reliance on a recently established $20 million equity line facility. Going forward, success depends heavily on execution risk related to acquisitions and digital asset deployment within an uncertain financial framework.

From Brand Licensing to Digital Assets: Past Financial Performance Summary

Farmhouse, Inc. has undergone a marked transformation from technology development and brand management toward digital asset initiatives and potential acquisitions. This strategic pivot coincides with a steep decline in reported revenues from intellectual property licensing activities, falling from $4,154 in FY2024 to only $623 in FY2025 — representing an approximate 85% year-over-year contraction [F1]. The plunge underscores the limited scale of licensing endeavors as the company phases out legacy activities.

Operating income remains negative but relatively stable, registering -$410,442 for FY2025 versus -$408,389 in FY2024, indicating that cost structures remain fixed despite lower top-line [F1]. Notably, net losses narrowed by approximately 15% year-over-year to -$393,266 in FY2025 from -$464,343 the prior year. This modest improvement may reflect cost containment or non-recurring adjustments rather than core profitability enhancement.

Cash flows from operations continue adverse trends with an outflow worsening by nearly 68%, amounting to -$179,022 for FY2025 [F1]. The company's balance sheet reveals severe liquidity issues—current assets stand at about $57,163 against current liabilities exceeding $2.27 million as of December 31, 2025 — yielding a critically low current ratio near 0.03 [F1]. Negative shareholders' equity deteriorated further to approximately -$2.67 million at year-end 2025 [F1], highlighting the strained financial health.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 623 | -393266 | -179022 | -410442 | -85.0% | +15.3% |

| 2024 | 4154 | -464343 | -106412 | -408389 | -72.7% | +17.2% |

| 2023 | 15227 | -560789 | -83454 | -509546 | +48.4% | -26.7% |

| 2022 | 10261 | -442782 | -252793 | -779632 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 14.7 |

| 2024 | 19.8 |

| 2023 | 28.3 |

| 2022 | 28.0 |

Source: SEC companyfacts cache [F1].

Current Ratio: ~0.03 (2025) [F1]

Liquidity Constraints and Equity Line Agreement Supporting Growth

Addressing these pronounced liquidity shortages, Farmhouse concluded a Common Stock Purchase Agreement with GHS Investments on November 5, 2025 . Under this agreement—the "equity line"—the company may issue up to $20 million of common stock over two years upon delivery of put notices.

Each put can draw between $10k and $500k depending on share trading volumes capped at twice the average daily dollar volume over the preceding ten days [S13]. Pricing mechanics favor investors purchasing shares at the lesser of 95% of market price or lowest intraday price during the pricing period. Notably, GHS's beneficial ownership is capped at just under five percent to limit dilution impacts on existing shareholders [S14].

As part consideration for entering this facility, Farmhouse issued GHS 500,000 restricted shares registered for resale post-SEC registration statement effectiveness . Proceeds are intended to support growth initiatives including digital asset investments (via Farmhouse Treasury LLC), general working capital needs given tight liquidity measures, and potential strategic acquisitions . Given the company’s extremely weak current ratio (~0.03) and negligible cash reserves ($14k), this facility addresses immediate capital gaps but introduces potential dilution risk if fully drawn [F1],[S7].

Digital Asset Treasury LLC: Strategy Behind the Anti-Debasement Mandate

In September 2025 Farmhouse formed Farmhouse Treasury LLC (FT), a manager-managed Nevada subsidiary designed as a vehicle for managing digital assets under an anti-debasement framework aligned principally with Bitcoin exposure alongside tokenized and physical gold holdings [S1],[S7],[S9].

FT operates under dedicated governance with both CEO and CTO actively involved as managers ensuring transparent oversight consistent with public company compliance standards [S1]. To implement treasury management with enterprise-grade safeguards, FT established custody arrangements through BitGo—an institutional custodian that provides insured custody solutions for cryptocurrency assets; although BitGo’s national trust bank charter remains pending regulatory approval [S1].

At inception FT held no capital nor owned any digital assets so there was no financial impact reported through FY2025’s end [S1],[S7]. Preliminary discussions are ongoing with various counterparties regarding possible financing platforms for digital asset strategies; however no binding agreements exist yet nor definitive plans confirmed [S1]. This places the initiative firmly at exploratory stages embodying high uncertainty about eventual deployment scale or economic impact.

Licensing Revenues: Scale, Trends, and Limitations

Licensing revenues represent residual activity tied principally to intellectual property associated with branded content including social media handles like @420 as well as NFT collaborations referenced in corporate filings [S1],[S7],[F1]. These have historically contributed limited amounts—dropping precipitously from over $4k in FY2024 down to just $623 in FY2025 [F1].

Revenue recognition follows ASC606 including sales-based royalty exceptions applicable when licensees record sales themselves—a conservative accounting treatment underscoring low transactional volumes supporting these licensing fees [S7]. Such minimal income renders licensing non-core operationally or profitably; it supplements but cannot drive meaningful company-wide revenue or earnings given its plateaued trajectory.

Strategic Acquisitions and Emerging Business Lines: Prospects and Risks

Farmhouse maintains a stated focus on evaluating acquisition targets intended to enhance shareholder value through scalable business operations beyond its current digital asset treasury concept.[S1],[S3],[S6] However no recent acquisitions have contributed material revenue or profits according to latest reports [S1].

Risk disclosures explicitly emphasize that significant financial resource limitations impair timely execution of strategic plans which encompass early-stage operational endeavors exposed to uncertainty surrounding their commercial viability. The prosecutable risk includes failure to secure or integrate target entities plus broader market volatility potentially stranding invested capital without returns.[S3],[S6]

This combination challenges investor expectations around platform evolution into profitable segments until operational momentum substantiates fiscal progress beyond exploratory digital assets or incidental licensing royalties.

Capital Structure as a Window into Financial Health and Shareholder Returns

Balance sheet metrics highlight a company hampered by persistent deficits including negative shareholders’ equity nearing minus $2.67 million as recorded at December 31, 2025 ([F1]). Such negative book value inflates reported return on equity roughly calculated near +14%, yet this is a mathematical artifact attributable to shrinking denominator rather than genuine profitability.

With operating cash flows deeply negative (-$179k) and negligible cash reserves ($14k), Farmhouse currently excludes any dividend disbursements or share repurchases from capital allocation priorities given its critical need for recapitalization.[F1],[S7]

Capital returns thus remain absent while structural turnaround requires successful growth platform establishment coupled with improved liquidity either organically or via financing such as the existing equity line facility described above.[S7]

What to Watch: Key Catalysts and Milestones Ahead

Despite lacking explicit guidance or firm milestones,[N/A analysis] key indicators include progress reports on:

- Commercial deployment outcomes for Farmhouse Treasury LLC’s anti-debasement digital asset portfolio,

- Completion of accretive acquisitions that transition FMHS toward sustained revenue generation,

- Utilization pace alongside dilution effects related to draws against the $20 million equity line,

- Improvements in liquidity ratios signaling alleviation of solvency pressures.

Future filings announcing binding agreements or realized strategic pivots away from platform evaluation toward operating business lines will crucially inform assessments of FMHS’s viability beyond its anecdotal licensing revenue patches.

Disclaimer: This analysis reflects data available through April 17, 2026 derived exclusively from public SEC filings ([F1], [S#]) without projections nor investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments