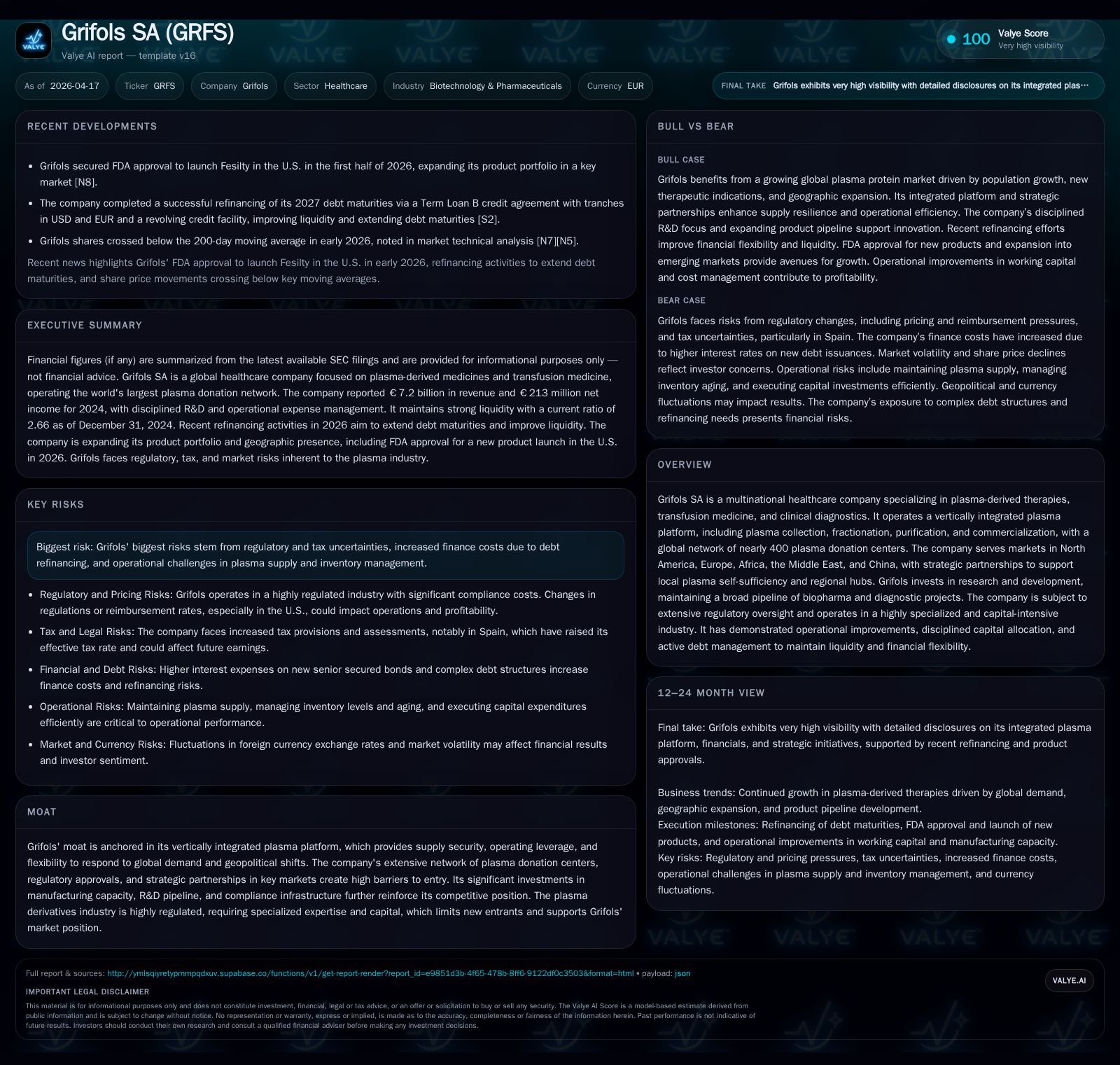

Grifols SA Reinforces Market Edge Through Strategic Refinancing and Portfolio Discipline

Grifols leverages its vertically integrated plasma platform and recent debt refinancing to underpin operational improvements and strategic growth.

Grifols SA has demonstrated consistent revenue growth driven by its comprehensive plasma-derived therapies business, expanding from €4.9 billion in 2021 to €7.2 billion in 2024. Operational efficiency gains and a focused R&D approach helped offset margin pressures despite higher finance costs and rising tax rates in 2024. The company recently secured a strategic refinancing package extending debt maturities through 2033, reducing funded gross debt, and improving liquidity with leverage-based margin step-downs. Looking ahead, Grifols’ extensive plasma collection network and self-sufficiency programs position it well to capitalize on growing global demand, while management’s evaluation of a potential U.S. IPO for its Biopharma subsidiary signals an intent to unlock value amid ongoing capital discipline.

Historical Revenue Growth and Margin Drivers: 2021–2024 Review

Grifols SA exhibited strong top-line momentum over the past four fiscal years, with revenue increasing from approximately €4.9 billion in 2021 to over €7.2 billion in 2024, representing a compounded annual growth near 9.4% [F1]. This consistent advance was supported primarily by its vertically integrated plasma platform encompassing plasma collection, fractionation, purification, and commercialization.

Margins experienced pressure partly owing to raw material cost dynamics typical of the plasma derivatives industry. However, the company’s integrated supply chain helped moderate such cost volatility—a critical advantage given the sector's intense focus on plasma fractionation efficiencies [S1]. Notably, net income fluctuated more markedly: after peaking around €271 million in 2022, it declined sharply to roughly €181 million in 2023 before recovering to over €212 million in 2024 [F1]. This net income variability reflects increased finance costs due to newly issued senior secured bonds bearing notably higher coupon rates compared to prior debt instruments [S1] as well as changes in effective tax rates influenced by non-recurring factors.

The following table summarizes key financial metrics from this period:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 7.2 | 213 | +9.4% | +17.8% |

| 2023 | 6.6 | 181 | +8.7% | -33.4% |

| 2022 | 6.1 | 271 | +22.9% | +2.2% |

| 2021 | 4.9 | 265 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | ROE% |

|---|---|---|

| 2024 | 0 | 2.5 |

| 2023 | 0 | 2.3 |

| 2022 | 3.2 | |

| 2021 | 3.6 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary [F1]

Operational Efficiencies and R&D Focus Shift

In addition to top-line progress, Grifols advanced operational efficiencies during this period. Selling, general & administrative expenses declined by approximately 8.6% from €1.4 billion in 2023 to around €1.28 billion in 2024—primarily reflecting a steep reduction of roughly three-quarters in one-off restructuring costs related to severance payments and consultancy fees tied to an Operational Improvement Plan [S1].

Research and development also saw a controlled recalibration; expenditures decreased modestly by about 2.8%, favoring fewer but more strategically important projects within its specialty plasma therapeutics pipeline [S1]. This approach aligns with industry best practices where pipeline prioritization seeks not only innovative product development but also maximizes capital efficiency in a highly regulated and competitive field.

Capital Structure Overhaul: Debt Refinancing and Liquidity Strengthening

A pivotal development shaping Grifols’ financial profile was its successful refinancing announced April 14, 2026 [S2][S4][S5]. The company replaced maturing facilities with a new Credit Agreement featuring Term Loan B tranches: $2 billion denominated in USD at SOFR plus a spread of approximately +250 basis points with slight original issue discount (OID), alongside €1.25 billion priced at Euribor plus ~300 basis points also exhibiting an OID near par.

Complementing term loans is a revolving credit facility totaling about $2.065 billion expiring October 2032 or potentially earlier subject to springing maturity clauses if earlier debts are not refinanced [S5]. Notably, these facilities include leverage-based margin step-down provisions incentivizing deleveraging over time [S5].

This transaction fully repaid prior First Lien Credit Facilities originated in late-2019 including Term Loans and Notes scheduled for maturity between now and early-2027 while providing fresh liquidity buffers [S5]. The longer tenor—typically seven years plus amortization schedules—and lower blended interest expense reduce near-term refinancing risk exposure.

Both loans are governed by New York law with robust collateral packages including substantial pledges of tangible/intangible assets across core subsidiaries along with restrictive covenants limiting additional indebtedness beyond defined thresholds [S7][S8]. Together these features reinforce Grifols' financial flexibility amidst industry cyclicality.

Navigating Regulatory and Macro Pressures

Grifols faces several embedded challenges particularly regarding taxation and regulatory compliance inherent to pharmaceutical multinationals operating across diverse jurisdictions [S1]. In fiscal year ending December 31, 2024 effective income tax escalated sharply from just under twenty percent in previous years to above fifty percent—driven largely by extraordinary tax liabilities linked to transfer pricing disputes in Spain (increasing uncertain tax provision from €77 million to €137 million) as well as one-time costs related to its Shanghai RAAS transaction (€32 million) [S1].

The company currently does not employ interest rate hedges for variable-rate exposures which could lead to incremental interest expense increases estimated at roughly €22 million for every percentage point rise in benchmark rates given unhedged SOFR/Euribor sensitivities noted [S1]. Additionally macroeconomic inflation impacts are localized mainly toward labor costs and selling/general administration staff expenses impacting cost base though not yet material across core geographies.

These factors require vigilant monitoring given operational intricacies of maintaining compliance while managing earnings volatility.

Future Growth Opportunities Amid Vertical Integration

The core strength underpinning Grifols’ market position remains its vertically integrated platform which spans end-to-end collection through commercialization of plasma-derived therapies [N2][S1]. Operating nearly four hundred plasma donation centers facilitates scale economies critical for operating leverage—allowing better absorption of fixed manufacturing overheads as throughput increases.

Self-sufficiency programs strategically developed target reducing external reliance on third-party plasma sources enhancing supply security especially significant amid geopolitical uncertainties affecting global bio-supply chains [S1]. Such programs support local production hubs aligned with regulatory mandates fostering regional autonomy.

This extensive infrastructure is paired with rigorous compliance standards making new entrants face high barriers due to capital intensity coupled with complex licensing/regulatory timelines characteristic of the sector.

Investment Pipeline and Biopharma Spin-Off Plans

Management continues refining the portfolio mix emphasizing innovation within biopharmaceutical pipelines geared towards next-generation plasmatic proteins and specialty medicines leveraging proprietary fractionation technologies [S1][S3]. Recent disclosure indicated ongoing evaluation of a potential U.S.-based Initial Public Offering (IPO) for the parent entity overseeing its U.S.-focused Biopharma business segment aimed at unlocking shareholder value subject to market receptivity and regulatory clearance [S3].

This contemplated move would permit greater strategic focus while isolating growth trajectories of the specialized unit independently within capital markets—a reflection of disciplined portfolio management congruent with peer industry practices.

Capital Allocation Approach: ROE, Dividends, and Shareholder Returns

Despite solid operational cash generation improving year-over-year (with reported net cash from operations reaching over €900 million recently), Grifols has elected conservative shareholder distribution policies characterized by suspension of dividends since fiscal year-end 2019/20 currently amounting to zero payout through end-2024 per disclosures [F1][S23].

Return on equity remains modest hovering around approximately 2.5% latest year data reflecting heavy reinvestment into capacity expansions along with servicing financial leverage incurred during prior acquisitions such as Biotest Holdings [F1]. Nonetheless reported cash equivalents near €980 million combined with current assets exceeding current liabilities by a factor above two-point six demonstrates sound liquidity positioning supporting ongoing organic investments alongside debt service requirements comfortably [F1].

At present there is no disclosed program of share buybacks which aligns with stated objectives prioritizing balance sheet deleveraging as well as maintaining ample cash reserves within this capital-intensive vertical integration model.

Financial Outlook and Key Performance Indicators to Watch (Analysis)

While explicit forward guidance is not offered within filings nor news releases at this juncture, several KPIs merit close observation going forward:

- Trends in net interest expense particularly against variable-rate loan exposures absent hedging mechanisms;

- Progress or cancellation status concerning proposed U.S IPO for Biopharma entity reflecting potential strategic pivot;

- Milestones pertaining to pipeline commercialization efforts including clinical trial progress or product approvals;

- Resolution or further developments pertaining to tax authority assessments impacting uncertain tax provisions;

- Operational metrics capturing volumes/frequency from plasma donation centers revealing capacity utilization dynamics that drive operating leverage effectiveness.

Given Grifols’ entrenched position reinforced by robust asset base coupled with renewed capital structure resilience amid external macro/microeconomic headwinds it remains positioned cautiously optimistic pending execution outcomes.

This analysis relies exclusively on Grifols SA's regulatory filings up through April 17, 2026 ([F1], [S#]) complemented by reputable news coverage ([N#]) as identified herein without speculative extrapolation beyond evidentiary sources or providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments