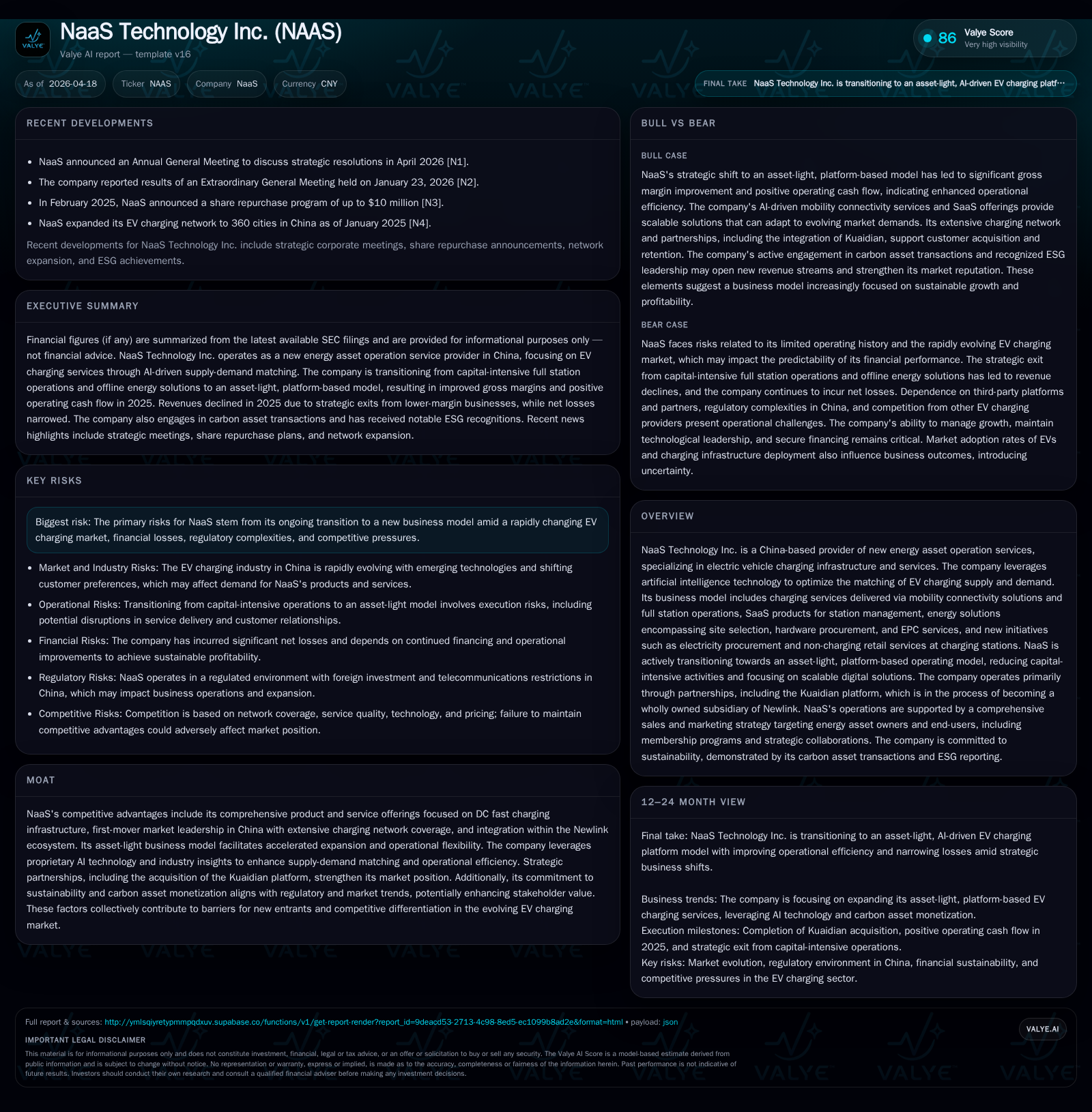

NaaS Technology’s Transition to Asset-Light Model Drives Margin Expansion Despite Revenue Decline

The company’s ongoing shift toward platform-based EV charging services improves gross margins and cash flow but challenges remain in scaling revenue.

NaaS Technology Inc. operates as a key provider of EV charging infrastructure and services in China, leveraging AI-driven platform solutions and partnerships like the Kuaidian platform. Historically, its revenue has declined from RMB233 million in 2023 to RMB125 million in 2025 amid a strategic pivot from capital-intensive operations toward asset-light models. This transition fueled significant gross margin expansion to 86% in 2025 and generated positive operating cash flow for the first time, marking operational progress. However, losses persist with net losses of RMB450 million (USD 64 million) in 2025, reflecting ongoing investments and market risks tied to EV adoption and regulatory uncertainties.

Company Background and Business Evolution

NaaS Technology Inc., based in Beijing, China, provides new energy asset operation services centered on electric vehicle (EV) charging infrastructure. The company leverages artificial intelligence (AI) technology for intelligent matching of EV charging supply and demand. Its offerings include mobility connectivity services primarily delivered through Kuaidian—a third-party operated platform expected to become a wholly owned subsidiary by mid-May 2026—as well as full station operations under an asset-light model [S6]. NaaS also provides SaaS products for digitalizing charging station management alongside integrated energy solutions covering site selection, hardware procurement, EPC services, electricity procurement, and other non-charging services.

Following a reverse acquisition completed June 10, 2022, NaaS became a wholly owned subsidiary of RISE Education Cayman Ltd., which changed its name to NaaS Technology Inc. The company has since restructured aggressively away from capital-intensive hardware operations toward scalable digital platforms aiming for improved operational efficiency and profitability within China's evolving EV market [S1].

Historical Financial Performance

NaaS's financial results show volatility over recent years ending December 31, 2025. Total revenues declined materially by nearly half—from RMB233 million in 2023 to RMB125 million (~USD17.9 million) in 2025—primarily due to exiting capital-heavy energy solutions such as hardware procurement and EPC services where revenues dropped from RMB100 million to under RMB1 million over the same period [S2][S10][S12]. Charging services remained the dominant segment with approximately 95% share of total revenues by value in 2025, mainly driven by mobility connectivity via Kuaidian and full station operations; however, absolute revenues also decreased year-over-year [S10]. New initiatives related to electricity procurement and non-charging services contributed modestly but are still nascent.

Despite revenue contraction, gross margins expanded sharply—from roughly 27% (gross profit of RMB63 million over revenues of RMB233 million) in 2023 to around 86% (gross profit of RMB108 million over revenues of RMB125 million) in 2025—reflecting benefits of shifting towards asset-light platform services with higher profitability [S2]. Operating expenses decreased substantially but remained large relative to revenues due to ongoing investments and legacy inefficiencies.

Net losses narrowed significantly from RMB1.31 billion in 2023 to RMB450 million (USD64 million) in 2025 [S2]. Operating cash flow improved markedly: after substantial negative cash flows exceeding RMB567 million in 2023, NaaS achieved slight positive operating cash flow of approximately RMB0.5 million (~USD0.07 million) for full-year 2025 [S9]. Investing activities shifted from heavy cash outflows into small net inflows mainly from disposal of financial assets and subsidiaries [S9]. Financing activities continued supporting operations through equity raises and debt financing.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2021 | -39 | -85 | -5 | -92.1% | ||

| 2020 | 147 | -20 | -32 | -21 | -33.1% | -195.4% |

| 2019 | 220 | 21 | -6 | 32 | +18.8% | +2.3% |

| 2018 | 185 | 21 | 55 | 30 | +24.2% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2021 | 278.8 | ||

| 2020 | -35 | -26.7 | |

| 2019 | 7 | -13 | 24.3 |

| 2018 | 3 | 46 | 31.4 |

Source: SEC companyfacts cache [F1].

Note: Operating income figures post-reverse acquisition are not explicitly reported; gross profit used as proxy for margin analysis [S2].

Growth Outlook and Strategic Initiatives

Key growth drivers include accelerating EV adoption rates combined with expanding fast-charging infrastructure optimized via AI-powered platforms [S1][S6]. Full ownership consolidation of Kuaidian by mid-May 2026 is expected to enable tighter operational control and monetization through membership programs offering discounts and loyalty incentives [S6]. This integration aims to boost end-user engagement, strengthen network effects, and increase charging volume throughput.

Additional growth avenues include monetization of carbon assets linked to EV charging activities exemplified by a recent carbon credit transaction involving approximately 21,000 metric tons related to Wuhan's EV fleet charging operations [N1][S1]. These sustainability-linked initiatives align with China's broader carbon neutrality goals.

However, growth is tempered by risks including intense competition within China's EV charging sector; regulatory uncertainties especially concerning payment service licensing frameworks; intellectual property enforcement challenges; evolving consumer charging behaviors; macroeconomic factors affecting vehicle sales; and transitional risks associated with business model shifts [S4][S8][S11][S19].

Capital Allocation and Financial Returns

NaaS has prioritized reinvestment over distributions given sustained net losses throughout recent years [F1][S9]. Capital expenditures have declined consistent with reduced focus on physical infrastructure investments—capex halved approaching low single-digit millions USD equivalent compared with prior periods dating back through FY2017–FY2020 [F1]. The recent positive operating cash flow marks initial progress controlling cash burn while continuing technology investments.

Equity remains deeply negative due primarily to accumulated losses incurred during rapid expansion phases funded through debt and equity issuance [F1][S15]. Liquidity appears improving with current assets exceeding current liabilities as per latest filings indicating manageable short-term obligations [F1][S7][S15]. No dividends or share repurchases have been declared recently; capital allocation emphasizes technology development, platform acquisitions such as Kuaidian, marketing efforts expanding user base via memberships, and enhancing SaaS offerings aimed at operational efficiencies for charging station operators [S6][N1]. Ongoing access to capital markets through registered direct offerings supports funding during this transformational phase [S13].

Industry Context

China remains the world's largest EV market supported historically by government subsidies promoting new energy vehicles (NEVs). Following subsidy phase-out at end-2022, industry dynamics now favor sustainable commercial models for EV charging infrastructure providers. High installation costs for DC fast chargers coupled with changing customer usage patterns create challenges balancing upfront capex against payback timelines. Asset-light platforms like NaaS that leverage digital connectivity tools plus AI optimization theoretically offer scalable returns but face fierce competition from state-backed operators alongside emerging independent players leveraging localized relationships.

Regulatory complexities around third-party payment licensing introduce compliance risks potentially constraining pricing innovation critical for customer retention while adding scrutiny on cross-border cash transfers impacting group liquidity management [S8][S23]. Intellectual property protections carry inherent enforcement uncertainties affecting technology providers specializing in proprietary AI matchmaking systems [S11].

Conclusion

NaaS Technology Inc.'s financial profile reflects a platform-oriented firm transitioning away from legacy CAPEX-heavy operations toward digital-first service models. The considerable contraction in top-line revenue alongside sharply expanding gross margins highlights strategic refocus yielding operational leverage despite short-term scale reduction. Slight positive operating cash flow signals improved financial discipline underpinning longer-term sustainability if growth initiatives succeed.

Key uncertainties include managing intensifying competition within China's complex regulatory environment while scaling proprietary AI capabilities integrated into customer-facing mobility connectivity anchored by imminent Kuaidian ownership consolidation. Investors should monitor execution on platform integration milestones, evolving regulatory compliance particularly relating to payment service licensing frameworks, EV adoption sustaining network throughput, plus further monetization of carbon assets.

Given sizeable accumulated losses offsetting equity base though improving sequentially without explicit ROE disclosure post-IPO transition phase still reflects high-growth but high-risk profile common among specialized EV infrastructure solution providers globally.

Note: This report is based solely on publicly available SEC filings up to April 17, 2026 ([F1],[S#]) and recent news ([N#]). It does not constitute investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments