Oncotelic Therapeutics' Financial Volatility and Clinical-Stage Pipeline Dynamics

Oncotelic’s heavily JV-dependent model and rare oncology pipeline are challenged by liquidity constraints and valuation uncertainties.

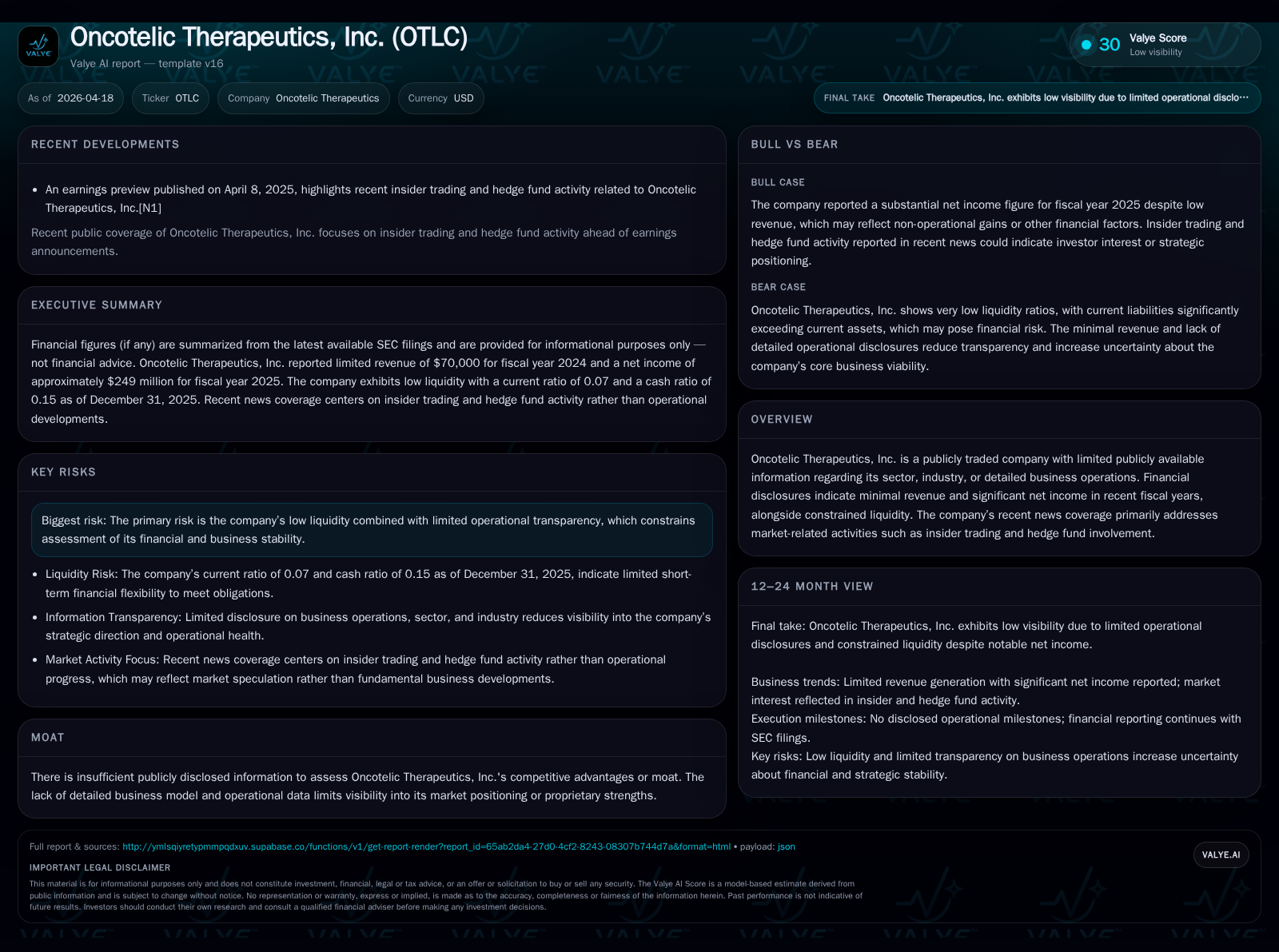

Oncotelic Therapeutics reports minimal revenue alongside significant net income driven by fair value gains on its minority stake in the GMP Bio joint venture, which is developing multiple oncology candidates including OT-101 with FDA Rare Pediatric Designation for DIPG. The company faces acute liquidity pressures with a low current ratio and reliance on convertible notes. Future value hinges on JV clinical progress, regulatory milestones, and capital raises amid valuation volatility tied to management assumptions and market conditions.

Historical Financial Performance and Operating Trends

Oncotelic Therapeutics exhibits minimal revenue generation with annual revenues steady at $70,000 since FY2023 despite prior higher levels in FY2021 [F1]. Operating losses have narrowed from approximately -$9.7 million in FY2022 to -$3.2 million in FY2025 but remain substantial, reflecting ongoing investment in R&D and operations.

A notable feature is the sharp increase in net income to about $249 million in FY2025 driven entirely by fair value gains related to Oncotelic's minority interest in its joint venture GMP Bio rather than core business operations [F1][S1]. These gains are non-cash and subject to reversal depending on future developments.

Operating cash flow remains negative at over -$1.3 million for FY2025, indicating continuing cash burn without offsetting operational cash inflows [F1]. Capital expenditures remain negligible historically.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 249 | -1383145 | -3 | +5610.2% | ||

| 2024 | 70000 | -5 | -740267 | -4 | 0.0% | +42.8% |

| 2023 | 70000 | -8 | -1321047 | -7 | -255.1% | |

| 2022 | 5 | -1452562 | -10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 94.9 |

| 2024 | -54.8 |

| 2023 | -65.2 |

| 2022 | 26.3 |

Source: SEC companyfacts cache [F1].

Table: Core financial metrics highlight flat revenues alongside narrowing operating losses but extreme net income volatility driven by investment revaluations [F1].

Business Model Centered on GMP Bio Joint Venture

Oncotelic's primary asset is its minority stake in GMP Biotechnology Limited (GMP Bio), a joint venture with Dragon Overseas Capital Limited focused on developing antisense therapeutics for rare pediatric cancers including diffuse intrinsic pontine glioma (DIPG), leveraging the OT-101 candidate [S1].

The company does not consolidate GMP Bio's financials but reports its investment using fair value accounting under ASC standards. Valuations incorporate third-party appraisals based on developmental progress and market assumptions but lack direct operational transparency [S1]. This structure complicates assessment of Oncotelic's underlying business performance.

Valuation Methodology and Asset Quality

Valuation of Oncotelic hinges on assumptions embedded in ASC-compliant fair value measurements of GMP Bio’s clinical-stage assets without revenues or approved products. The recent increase in carrying value reflects management estimates of development milestones, regulatory success probabilities including FDA designations such as Rare Pediatric Disease Designation for OT-101, market potential assessments across regions, discount rates reflecting risk factors, and comparable transactions [S1].

These subjective inputs expose Oncotelic to potential material impairment charges if adverse clinical or market developments occur.

Pipeline Overview: Rare Oncology Indications

Through GMP Bio ownership, Oncotelic pursues clinical advancement of OT-101 targeting DIPG—an orphan oncology indication granted FDA Rare Pediatric Disease Designation—and five additional compounds addressing various cancers along with an Artemisinin program for COVID-19 therapy development [S1]. Regulatory pathways leverage orphan drug incentives including priority review vouchers that may provide commercial advantages upon approval.

Liquidity Challenges and Capital Structure

At December 31, 2025, Oncotelic reported current assets around $1.2 million versus current liabilities exceeding $18 million resulting in a critically low current ratio near 0.07. Cash balances were approximately $409K at September-end 2025 [F1].

To address liquidity needs the company issued secured convertible promissory notes aggregating nearly $400K principal amount with terms including a 10% original issue discount and annual interest rate of approximately 10%, convertible into common stock at fixed prices near $0.07 per share plus attached warrants exercisable at higher prices [S6][S18]. These instruments underscore reliance on dilutive financing amid short-term funding challenges.

Corporate Governance and Legal Environment

There are no material pending legal proceedings disclosed currently; however risk factors emphasize limited transparency due to the JV arrangement and dependency on external financing and successful clinical progress within GMP Bio as critical risk vectors [S4][S7][S9].

Capital Allocation and Shareholder Returns

Operating cash flows have been consistently negative exceeding $1 million annually including -$1.38 million for FY2025 despite positive net income driven by non-cash valuation gains [F1]. No dividends or share repurchase programs have been reported indicating capital deployment focuses on sustaining operations and funding pipeline progress via the joint venture structure [S19][S25].

Return-on-equity calculated from net income over equity stands near 95%, reflecting distortions from unrealized non-cash gains rather than sustainable operational profitability [F1].

Outlook: Milestones and Value Drivers

Key upcoming catalysts include clinical data readouts supporting regulatory filings primarily managed by GMP Bio alongside possible monetization of priority review vouchers granted under orphan drug frameworks that could enhance commercial prospects for OT-101 [S1].

Liquidity improvements through capital raises or strategic partnerships remain essential given working capital constraints. Monitoring JV developmental milestones will be critical to evaluate trajectory.

Investment Risks Summary

The principal risks include:

- Valuation uncertainty tied to fair value accounting of a pre-revenue joint venture reliant on clinical trial outcomes;

- Acute liquidity constraints reflected by low current ratios and dependence on dilutive convertible debt;

- Lack of direct operational revenue necessitating continued external financing;

- Potential adverse impacts from clinical setbacks or regulatory delays;

- Limited disclosure limiting investor insight into underlying fundamentals.

These factors advise caution when assessing Oncotelic Therapeutics' financial health given inherent volatility embedded within its joint venture-based business model focused on orphan oncology indications.

This analysis is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments