Eightco Holdings Inc.: Strategic Shift to Digital Asset Treasury and E-commerce Challenges

Eightco pivots towards digital asset investments while managing risks inherent in its concentrated e-commerce revenue and operating losses.

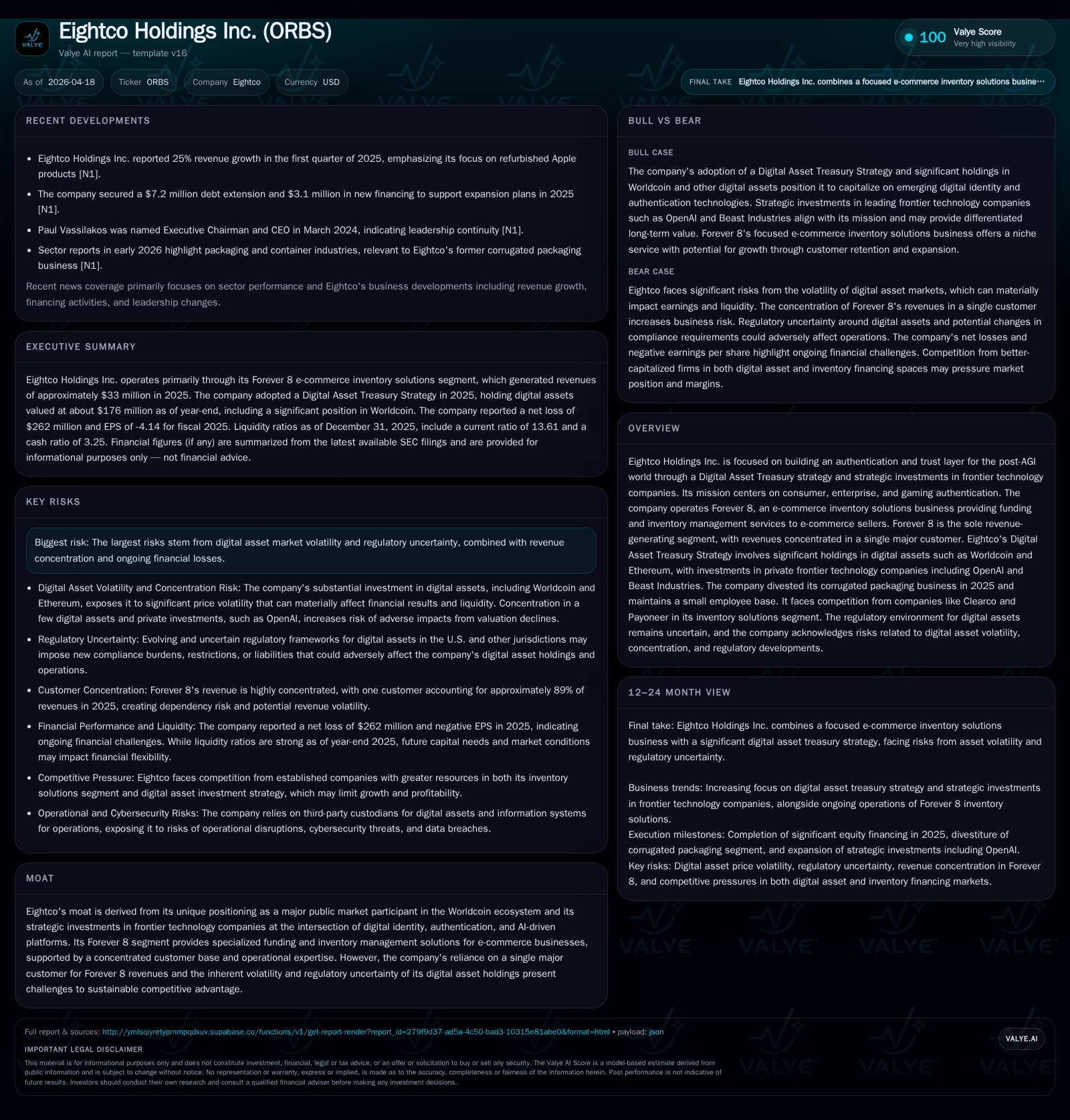

Eightco Holdings Inc. has transitioned sharply towards a Digital Asset Treasury (DAT) strategy since September 2025, allocating significant capital into digital assets such as Worldcoin and Ethereum. Concurrently, its sole revenue-generating segment, Forever 8, has faced headwinds with declining sales and heightened dependency on one major customer. The company's financials reflect steep operating losses and volatile earnings increasingly influenced by fair value adjustments of digital assets under ASU 2023-08. While Eightco's strategic investments in frontier technologies aim to build a post-AGI authentication layer, concentrated revenues, regulatory uncertainties around digital assets, and liquidity pressures underscore considerable challenges ahead.

A Historical Look: Revenue Decline and Mounting Operating Losses

Eightco Holdings has experienced notable pressures over the fiscal years through 2025. Its sole operating revenue driver remains Forever 8, an e-commerce inventory solutions subsidiary acquired in late 2022. Reported revenues from Forever 8 declined from approximately $39.6 million in FY2024 to about $33.0 million in FY2025, marking a significant contraction reflective of market challenges faced within this segment [F1].

This top-line shrinkage coincides with sharply worsening operating income results: Eightco's operating loss expanded drastically by roughly 598% year-over-year from -$8.2 million in FY2024 to -$57.2 million in FY2025 [F1]. The surge largely stems from the introduction of fair value assessments on volatile digital assets held under the company’s newly adopted Digital Asset Treasury strategy as well as underlying operating performance deteriorations.

Net income similarly worsened markedly, plunging from a modest profit of about $0.7 million in FY2024 to a massive net loss exceeding -$262 million in FY2025 [F1]. This discrepancy between operating losses and net losses is substantially attributable to unrealized losses on digital asset revaluations flowing through earnings as per updated accounting standards (ASU 2023-08) applied beginning January 2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -262 | -11 | -57 | -37079.3% |

| 2024 | 1 | -7 | -8 | +101.0% |

| 2023 | -68 | -6 | -10 | -44.6% |

| 2022 | -47 | -17 | -16 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | -112.6 | |

| 2024 | 5.9 | |

| 2023 | 49455 | 1736.9 |

| 2022 | 49455 | -771.2 |

Source: SEC companyfacts cache [F1].

Values are rounded; percentages calculated where data allows [F1]

Forever 8’s Revenue Concentration and Its Sustainability Challenge

Forever 8 functions as Eightco’s lone revenue-generating unit, providing funding and inventory management services primarily for e-commerce sellers aiming to optimize stock without capital constraints [S1]. However, the business is highly concentrated with an estimated single customer representing approximately 89% of Forever 8’s total revenues for FY2025, up from about 75% in FY2024 [S4,S9]. This extreme dependence exposes the segment to material customer concentration risk that can imperil consistent cash flow if that relationship deteriorates.

The company reports no material backlog of orders, suggesting limited visible future revenue visibility beyond current contracts [S4]. Competitive pressures intensify risk: competitors Clearco (specializing in revenue-based financing for startups) and Payoneer (global payments platform) directly challenge Forever 8’s space with differentiated scale and technology platforms that could erode market share or compress margins [S10]. Furthermore, macroeconomic headwinds such as inflationary cost increases for materials and labor have strained operational profitability despite management efforts to offset these impacts [S5].

The Digital Asset Treasury Strategy: Ambitions Meet Market Realities

On September 8, 2025, Eightco adopted its distinctive Digital Asset Treasury (DAT) strategy which directs substantial liquidity raised through capital markets towards acquiring crypto assets within emerging ecosystems like Worldcoin (WLD) and Ethereum (ETH), alongside stablecoins and other tokens used for operational purposes [S1,S14]. As of December 31, 2025, the company held approximately $176 million of digital assets measured at fair value per new accounting standard ASU 2023-08 that requires changes in asset prices to be recognized through net income each period—amplifying earnings volatility unrelated to core operational results [S1,S7,S17].

Of particular note is Eightco’s position as the largest public market participant holding about a tenth of Worldcoin’s circulating supply at period end—a unique moat but also a concentrated exposure subject to price swings and regulatory scrutiny given Worldcoin's disputed compliance with global KYC/AML standards [S1,S25,S28]. The company acknowledges risks tied to market illiquidity, trading halts, custody failures via third-party providers like Kraken and Coinbase, and challenges converting crypto holdings into fiat currency amidst periods of stress or regulatory intervention [S1,S15,S20].

Capital deployment activities supporting this strategy included a significant $270 million private investment round (PIPE) completed concurrently with DAT approval plus additional proceeds via the at-the-market (ATM) equity offering program—all enabling the funding ramp-up for acquisitions yet potentially tethering future financing capacity closely to crypto valuations [S6,S14,S25].

Investments in Frontier Technology: Building a Post-AGI Trust Layer

Complementing its treasury holdings, Eightco sponsors strategic long-term equity stakes in frontier technology companies integral to its vision of authentication within AI-driven economies—among them OpenAI (~30% representation within total treasury allocations), developer of ChatGPT; and Beast Industries, owned by content creator MrBeast aligning with next-gen consumer distribution channels [S1,S10].

These investments reflect a deliberate capital allocation philosophy targeting blockchain infrastructure, Proof of Human verification technologies that underpin emerging digital identity frameworks post-artificial general intelligence (AGI), as well as artificial intelligence platforms—a convergence aiming to forge robust trust layers critical for decentralized applications and gaming authentication domains endorsed by the company’s mission pillars [S1]. Although not currently material revenue contributors themselves, these positions epitomize growth avenues that are speculative yet potentially transformative.

Capital Structure, Liquidity, and the Strain of Volatility

Eightco maintains a strong current ratio near 13.6x at December-end driven principally by cash & equivalents approximating $58 million on top of other liquid current assets totaling nearly $245 million against relatively modest current liabilities below $18 million—reflecting substantial liquidity reserves often earmarked for the DAT strategy rather than operational needs alone [F1,S6,S25].

Nonetheless, recurring negative cash flows from operations (-$11 million CFO for FY2025) expose strain despite infusion of capital afforded through equity raises totaling roughly $270M during calendar year ending December ‘25 primarily deployed into crypto acquisitions—highlighting reliance on equity markets sensitive to digital asset price landscapes for refinancing capacity [F1,S6,S14,S23].

Debt levels remain low relative to equity capitalization ($233 million equity at fiscal year-end), limiting leverage but reinforcing dependence on equity issuance while buybacks remain negligible amid ongoing financial deficits underscoring minimal shareholder returns at present [F1,S12].

Evaluating Returns: ROE, Operating Cash Flow, and Capital Allocation

Financial returns present a challenging profile: net losses surged drastically yielding an approximate return on equity (ROE) near negative -112.6% powered largely by unrealized digital asset markdowns overshadowing nominal operational results [F1]. Meanwhile cash flow metrics tell a picture consistent with an investment-stage entity: persistent negative operating cash flows reflect expenditures exceeding revenues alongside capex obligations within investments allocated to growth initiatives including FOREVER8 operations plus strategic tech stakes—thereby resulting in significant free cash flow pressure absent alternative financing sources [F1,S12].

Notably Eightco declares no dividend policy nor conducts meaningful share repurchases likely due both to retained capital needs supporting its evolving business model alongside volatile earnings impairments restraining conventional capital return strategies presently available to shareholders [S12].

Risks from Market Dynamics and Regulatory Environment

The conglomerate faces multifaceted risks heavily intertwined with its pioneering engagement across novel asset classes:

- Volatility inherent within digital asset markets exposes reported earnings—and subsequently enterprise valuation—to severe swings unrelated directly to fundamental business health given periodic fair value mark-to-market accounting requirements per ASU-2023-08 impacting comparability across periods or peer firms lacking such exposures [S1]

- Custody risks prevail due to reliance on third-party institutional custodians vulnerable to insolvency or cyber breaches affecting possession of high-value token holdings; any loss here would impair liquidity significantly given concentrated exposure in WLD tokens hosted primarily offline but monitored rigorously per disclosures [S15,S20]

- Regulatory ambiguity remains acute as federal/state securities agencies debate classification of core holdings including Worldcoin tokens; potential retroactive registration mandates or transfer restrictions could crystallize illiquidity or compliance costs complicating company operations materially despite proactive internal governance efforts [S13,S18]

- Market acceptance risks entwined with Worldcoin’s proof-of-personhood biometric scanning face challenges from global KYC/AML compliance frameworks positioning product adoption against legal restrictions potentially supressing demand or triggering audits impacting reputation severely across regions influencing token value trajectory alongside ongoing geopolitical instability mediating macroeconomic conditions affecting e-commerce transactional volumes managed by Forever eight segment as well [S28]

- Customer concentration is another operational risk vector underpinning vulnerability should contract terms alter unexpectedly or competing products capture market share more effectively undermining recurring cash inflows imperative for working capital needs underpinning broader corporate initiatives beyond DAT strategy deployment thus slenderly balancing short-term survival against long-term innovation bets taken simultaneously by management teams across distinct sectors concurrently within same corporate umbrella planning horizon stretching beyond immediate fiscal cycles [S4,S9]

What to Watch Ahead: Milestones and Strategic Catalysts

Absent explicit financial forecasts from company filings or press releases beyond recent announcements detailing attendance at ecosystem events like World Lift Off ([N3]), observers should focus on several qualitative indicators pivotal for assessing trajectory:

- Monitoring quarterly updates revealing fluctuations in fair value adjustments on key digital assets—especially WLD token price movements given outsized balance sheet representation—is critical due to their direct impact on reported earnings volatility.

- Potential further diversification efforts reducing dependency upon Forever eight largest customer or expansion into complementary verticals could improve stability but would require constructive evidence emerging from segment reporting or investor presentations.

- Timely updates surrounding regulatory clarity developments at SEC or CFTC level affecting crypto classifications will inform whether intrinsic legal risk lessens or intensifies for their treasury holdings.

- Progression and valuation markers associated with strategic investments such as OpenAI stakes might offer proxy signals regarding potential portfolio appreciation aligned with technological validation regimes surrounding post AGI authentication frameworks.

- Capital raising environment sensitivity should be observed since ability to secure incremental funding tied closely with prevailing crypto market sentiments will determine operational runway amid continuing negative cash flow trends.

Market participants should thus maintain vigilance toward news flows concerning these axes while recognizing Eightco’s hybrid model simultaneously straddles deeply innovative technology sponsorships alongside legacy-like inventory financial services presenting unique tradeoffs rarely seen within public companies today.

Disclaimer: This analysis is based exclusively on publicly filed documents including Form 10-Ks credible news sources cited herein; all figures are sourced accordingly without extrapolation or speculative estimation beyond documented facts evaluated objectively without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments