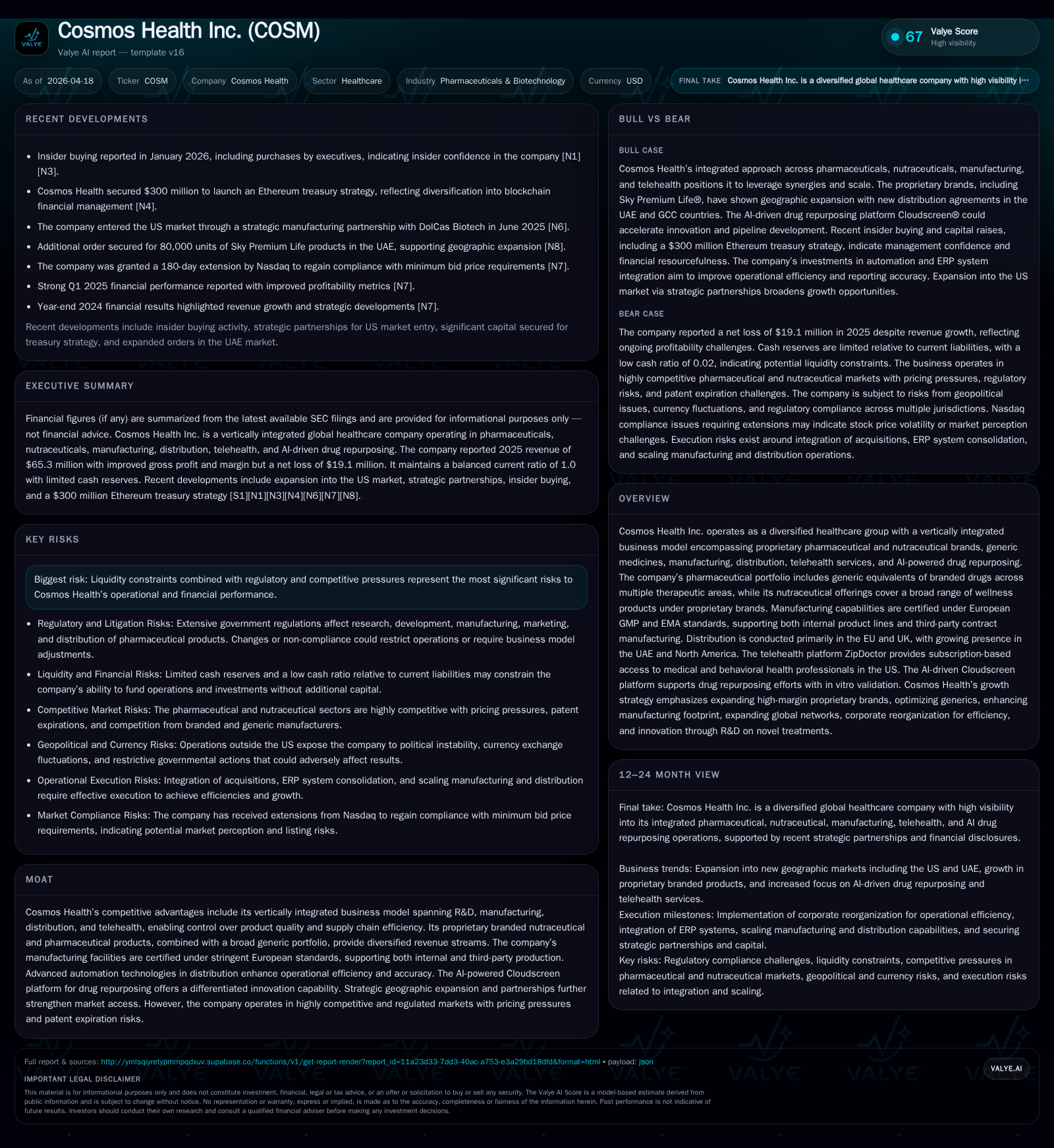

Cosmos Health Expands Global Footprint Amid Continued Losses

The company’s vertical integration and geographic expansion drive strong revenue growth, while persistent operational losses and constrained cash flow highlight ongoing challenges.

Cosmos Health Inc. has broadened its global operations across pharmaceutical manufacturing, branded generics, nutraceuticals, and telehealth services, achieving nearly 20% revenue growth in fiscal 2025. Despite this top-line momentum, operating and net losses widened due to elevated costs and investments in innovation and market entry. The vertically integrated model—spanning R&D, European GMP-certified manufacturing, distribution automation, and an AI-powered drug repurposing platform—offers competitive advantages amid a highly regulated environment. However, liquidity pressures alongside pricing competition and regulatory complexity pose near-term challenges to profitability and cash flows.

Historical Financial Performance

Cosmos Health has delivered consistent revenue growth from $50.3 million in FY2022 to $65.3 million in FY2025—a nearly 20% increase year-over-year in the latest fiscal year—reflecting successful expansion of its pharmaceutical generics and proprietary nutraceutical brands primarily within Greece and the EU [F1; S4].

Despite rising revenues, operating income remains negative, with losses widening to $16.7 million in FY2025 from $7.5 million three years prior. Net income followed a similar trajectory, reaching a loss of approximately $19.1 million [F1]. This indicates that fixed costs related to R&D investments, manufacturing scale-up, and SG&A expenses are outpacing sales gains.

Operating cash flow was also negative at $8.4 million in FY2025, while capital expenditures fell sharply by approximately 87% compared to FY2024’s already low level of about $418,000—suggesting cost control measures or completion of prior investments [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 65 | -19 | -8 | -17 | +19.9% | -18.3% |

| 2024 | 54 | -16 | -8 | -16 | +2.0% | +12.7% |

| 2023 | 53 | -19 | -16 | -22 | +6.0% | -34.1% |

| 2022 | 50 | -14 | -15 | -7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -9 | -103.9 | |

| 2024 | 0 | -8 | -66.0 |

| 2023 | 100452 | -17 | -51.4 |

| 2022 | -15 | -35.2 |

Source: SEC companyfacts cache [F1].

Vertically Integrated Model

Cosmos Health operates a vertically integrated healthcare platform encompassing research & development; manufacturing certified under European Medicines Agency Good Manufacturing Practices (GMP); automated pharmaceutical wholesaling using technologies such as the ROWA™ robotic system; proprietary nutraceutical brands; generic drug portfolios; and telehealth services through ZipDoctor in the United States [S7; S20].

Manufacturing capabilities cover diverse pharmaceutical forms including tablets and syrups as well as biocides and cosmetics produced under GMP certification [S7]. Automation enhances order accuracy and cost efficiency crucial for competing within price-sensitive markets.

The recent acquisition of Cloudscreen®, an AI-driven drug repurposing platform specializing in identifying new uses for approved drugs particularly in oncology indications supports Cosmos Health's emphasis on innovation with lower risk profiles compared to novel drug discovery [S11].

Geographic Footprint

Most revenues originate from Greece (>97%) with additional sales from other EU countries such as the UK and Balkan nations including Bulgaria and Albania [S4]. The company is expanding into the UAE through partnerships targeting nutraceutical distribution while initiating operations in North America via ZipDoctor telehealth services starting in early 2026 [S4; S21].

While geographic diversification aims to broaden market access and mitigate currency risks inherent in foreign revenues denominated outside the U.S., the business faces pricing pressures from consolidated pharmaceutical wholesalers with growing purchasing leverage across regions [S4; S18].

Profitability & Cash Flow Challenges

Despite revenue growth momentum (+19.9% YoY), operating losses increased slightly due to high fixed costs tied to R&D activities including Cloudscreen development programs plus telehealth service deployment [F1; S9]. Negative operating cash flow persisted at $8.4 million with minimal capex spend signaling tight liquidity conditions requiring disciplined capital allocation [F1].

Working capital remains tightly managed with current assets closely matching current liabilities as of year-end 2025 [F1], emphasizing the importance of efficient receivables and payables management.

Regulatory & Pricing Risks

The company’s operations are subject to extensive regulatory oversight across multiple jurisdictions including stringent EU pharmaceutical regulations requiring product licensing under Good Distribution Practices (GDP) plus periodic renewals that have previously experienced delays resulting in fines [S5; S8; S16].

Tax compliance is complex given international transfer pricing laws impacting intercompany transactions between U.S.-based parent company and foreign subsidiaries which could affect effective tax rates if challenged by authorities [S5; S6].

Pricing pressures intensify amid competitive generic markets combined with potential impacts from U.S. legislative initiatives such as Medicare drug price negotiation rules that may indirectly affect international markets over time [S10].

Capital Allocation & Shareholder Returns

Capital expenditures declined significantly indicating cautious investment pacing possibly linked to prior facility upgrades or IT systems implementations completed recently [F1; S29]. No dividends or share repurchases were recorded since FY2024 reflecting prioritization of reinvestment or liquidity preservation during this growth phase [F1].

Innovation Pipeline & Strategic Milestones

Cloudscreen’s AI-powered repurposing platform offers potential upside through identification of new therapeutic indications with patent filings underway particularly targeting oncology applications supported by preclinical collaborations such as with the National Hellenic Research Foundation [S11; S13].

Upcoming milestones include scaling telehealth user base in North America post-2026 launch alongside regulatory license renewals critical for core wholesale distribution businesses primarily within Greece [S3; S9]. Progress against these will be key indicators of operational leverage gains.

Conclusion

Cosmos Health balances strong revenue growth driven by diversification into proprietary brands and geographic expansion against persistent operating losses reflecting ongoing investment in R&D innovation platforms like Cloudscreen® alongside telehealth service rollout.

The company’s vertically integrated model affords competitive differentiation but navigating regulatory complexities combined with liquidity constraints demands rigorous financial discipline.

Monitoring execution on expanding US telehealth presence plus advancement of AI-driven drug repurposing pipelines will be essential for assessing Cosmos Health’s prospects for achieving sustainable profitability.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments