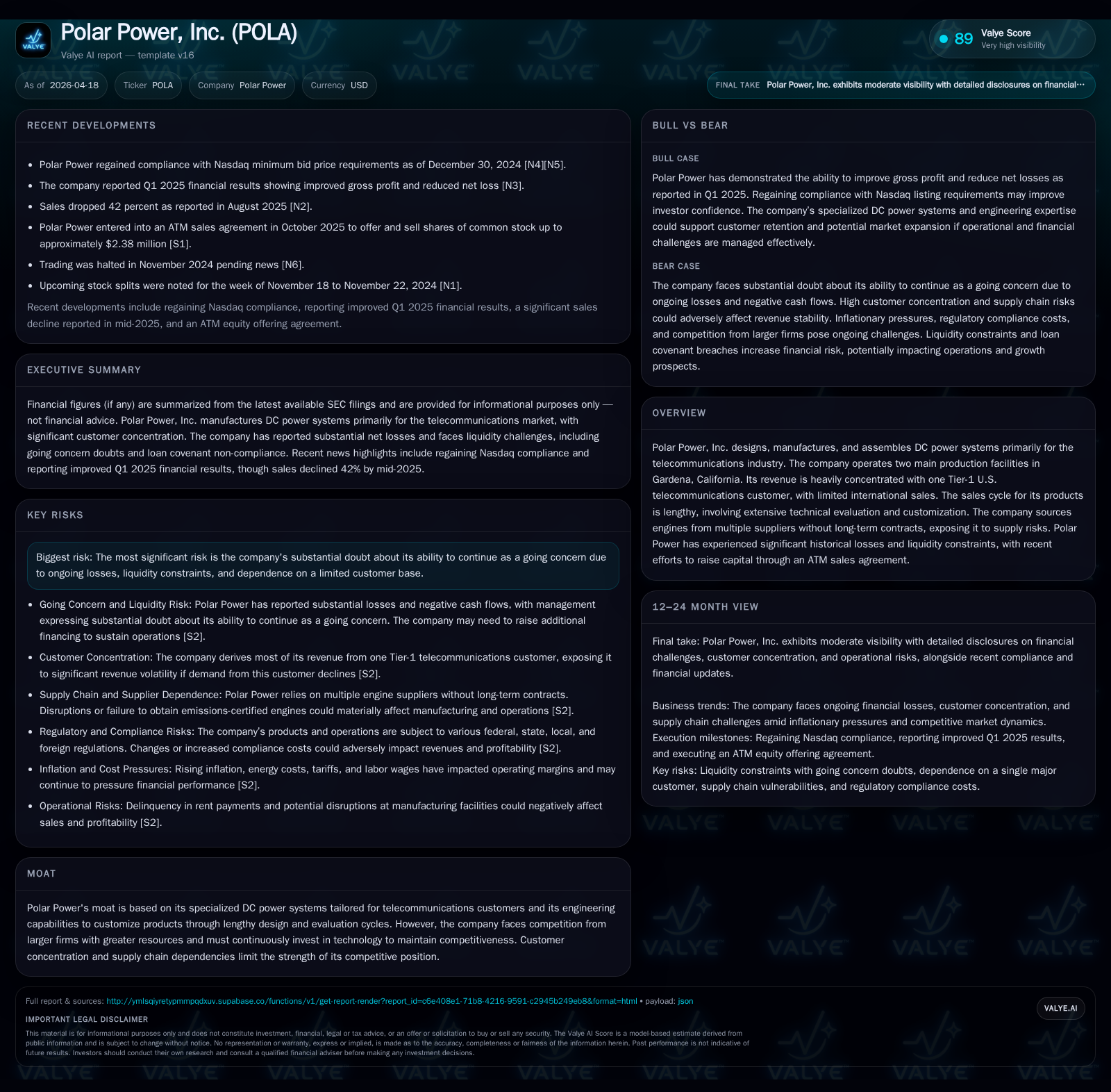

Polar Power Faces Steep Losses and Liquidity Risks Amid Market Focus

A niche DC power systems manufacturer contends with a concentrated customer base, mounting losses, and critical liquidity challenges.

Polar Power, Inc. crafts specialized DC power systems primarily for telecommunications, leveraging engineering customization to serve critical off-grid and backup applications. Despite modest revenue growth of 3.1% to $24.8 million in 2025, the company’s financial health deteriorated with net losses nearly doubling year-over-year to $9.13 million and operating cash outflows deepening. Reliance on one Tier-1 U.S. telecom customer for 65% of sales underscores concentration risks amid limited international expansion. While product innovations into hybrid power and EV mobile charging open diversification pathways, liquidity strains including rent delinquencies and covenant breaches place substantial doubt on going concern status. Capital allocation remains conservative with minimal reinvestment, reflecting ongoing survival mode.

Recent Financial Performance: Persistent Losses during Modest Revenue Growth

Polar Power reported annual revenue growth of just 3.1%, reaching approximately $24.8 million in fiscal year 2025 compared to the prior year [F1]. However, beneath this top-line stability lies a pronounced deterioration in profitability metrics: operating income tumbled by over 92%, culminating in a loss of $8.42 million. Net losses worsened materially by roughly 95%, hitting $9.13 million for the full year [F1]. Operating cash flow results echo this trend with expenses outpacing inflows—CFO fell nearly 98% year-over-year to negative $1.06 million [F1]. These figures reveal that despite maintaining sales volumes, operational efficiency has declined markedly.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -9 | -1 | -8 | 19000 | -95.3% |

| 2024 | -5 | -1 | -4 | 19000 | +28.6% |

| 2023 | -7 | -3 | -6 | 194000 | -17.3% |

| 2022 | -6 | -7 | -6 | 25000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | -6342.4 |

| 2024 | -1 | -54.9 |

| 2023 | -4 | -49.6 |

| 2022 | -7 | -30.7 |

Source: SEC companyfacts cache [F1].

Note: Fiscal years represent period ends stated; capex figures are rounded thousands.

Customer Concentration and Market Exposure: Telecom Reliance and Diversification Attempts

Polar Power’s single largest revenue contributor remains a Tier-1 U.S.-based telecommunications company representing about 65% of total net sales in 2025 [S1][S5][S9]. This concentration underscores a material customer risk given the variability inherent in contract renewals or shifts in procurement strategies within the telecom sector [S9]. The company’s international sales contracted materially to only about 7% of total revenues last year from higher prior-year levels [S1], signaling challenges expanding geographically beyond its entrenched U.S.–telecom market core.

Efforts toward diversification are visible but nascent, including targeted applications in military robotics power support (8% revenue), marine systems (down to about 1%), and emerging EV mobile charging solutions (approximately 3%) [S1][S25]. Despite these initiatives, telecommunications clearly dominates Polar Power’s sales profile creating an exposure bottleneck.

Product Portfolio and Industry Applications: DC Power Systems in Telecom, Military, and EV Charging

At the core of Polar Power’s value proposition are its direct current (DC) power systems designed primarily for off-grid prime power and backup power scenarios critical in telecom infrastructure [S1]. These range from stationary base power systems encapsulating automated controls and remote monitoring capabilities to hybrid power systems integrating advanced lithium-ion battery chemistries with proprietary battery management systems.

Further innovation has birthed solar hybrid configurations combining photovoltaic energy sources with hybrid storage architectures as well as increasingly compact mobile power units aimed at applications like electric vehicle (EV) fast-charging emergency services [S1]. The company markets its units across multiple fuel formats including diesel, propane (LPG), natural gas, and renewable options—all tailored for efficiency within their respective energy paradigms.

Prime power generator products incorporating Toyota’s optimized propane/natural gas engines target changing regulatory environments where tightening EPA restrictions diminish small diesel viability [S1]. This positions Polar Power strategically to address evolving demands for cleaner fuel adoption within critical infrastructure.

Supply Chain and Operational Constraints: Engine Sourcing Risks and Facility Challenges

Polar Power’s reliance on multiple third-party engine suppliers without long-term contracts imparts significant supply chain risk potentially impacting timely fulfillment [S5][S6]. The technical complexity of product customization inherently prolongs the sales cycle, amplifying inventory management challenges amid fluctuating material lead times.

Operationally, liquidity issues have precipitated serious facility concerns including delinquent rents at two Gardena-based manufacturing sites leading to legal summonses for eviction proceedings as recently as late 2025 [S1][S2][S14]. Although litigation was paused early in 2026 pending negotiations over payment plans, failure to resolve these matters could severely disrupt production continuity and access to critical inventory.

This precarious facility status magnifies the risk posed by already extended technical evaluation cycles needed before product acceptance [S9], compounding potential delays detrimental to both customer satisfaction and revenue timing.

Liquidity Position and Going Concern Warnings: Capital Raises and Delinquent Obligations

At December 31, 2025, Polar Power reported a cash balance of merely $200,000 against current liabilities exceeding $10 million resulting in a current ratio below unity at approximately 0.97—a traditional red flag for solvency concerns [F1]. Historic net losses coupled with recurring negative operating cash flows have drained internal resources rapidly.

The company’s management explicitly acknowledges "substantial doubt" about its ability to continue as a going concern given these financial stressors along with looming credit covenant violations tied to its credit facility with Pinnacle Finance through September 2026 [S1][S2][S14]. To partially address funding needs, Polar Power entered into an ATM stock sale agreement in late 2025 permitting periodic share issuance—but such dilutive strategies underscore financing vulnerabilities rather than long-term stability [S1].

Capital Allocation Review: Absence of Dividends, Minimal Capex, Focus on Survival

Polar Power has not declared or paid any dividends historically nor engaged in share repurchase programs indicative of mature capital return policies [S4]. Capital expenditures remain minimal; fiscal years ending both 2024 and the latest available indicate annual spend hovering near $19,000—a negligible figure relative to operational scale—highlighting almost no reinvestment into production capacity or technology upgrades during ongoing financial duress [F1][S4].

The stark contrast between deeply negative net incomes versus modest equity booked ($144K at year-end) produces an alarmingly negative return on equity approaching negative six thousand percent—manifesting severe erosion of shareholder value consistency over recent periods [F1].

Outlook and Strategic Opportunities: Renewable Energy Integration and EV Charger Expansion

Forward-looking commentary from management indicates strategic intent to capitalize on transitions away from diesel towards greener fuels within their core DC generator offerings through LPG/natural gas engines optimized for regulatory compliance trends impacting emissions-heavy technologies [N1][S1]. Expansion into Southern Pacific telecommunications markets aims to leverage ongoing infrastructure buildouts supporting next-generation network deployments referenced by the company [S1].

Parallel development efforts around mobile EV charging units upgrading from CHAdeMO standard towards the more globally adopted Combined Charging System (CCS) protocol demonstrate attempts at entering emergent clean mobility segments via portable high-power solutions suitable for robotic or security applications reliant on efficient prime power sources [S1].

While such initiatives may diversify future demand beyond telecom client concentration risk presently dominant, these remain early stage without firm revenue guidance attached.

Risks to Monitor: Legal, Regulatory, and Competitive Pressures Ahead

The inherent risk profile encompasses not only chronic financial instability but also external pressures including potential liability claims arising from use of products within mission-critical communications networks which demand high reliability under warranty commitments [S3]. Failure modes might provoke costly remediation or reputational damage impeding future contracts.

International expansion invites complex compliance mandates notably under U.S Foreign Corrupt Practices Act (FCPA) regulations alongside trade tariffs and export controls adding compliance costs and enforcement risks particularly when deploying capital-intensive projects overseas [S6][S12][S22][S24].

Competition escalates with larger firms possessing deeper R&D budgets capable of rapid technological innovation and price competition which could erode Polar Power’s specialized yet narrowly defended moat comprising technical customization capability amid lengthy design cycles .

Disclaimer

This analysis is prepared solely for informational purposes based on public filings and reporting as of April 2026 without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments