urban-gro's Strategic Pivot to Flash Sports & Media Amid Financial and Operational Challenges

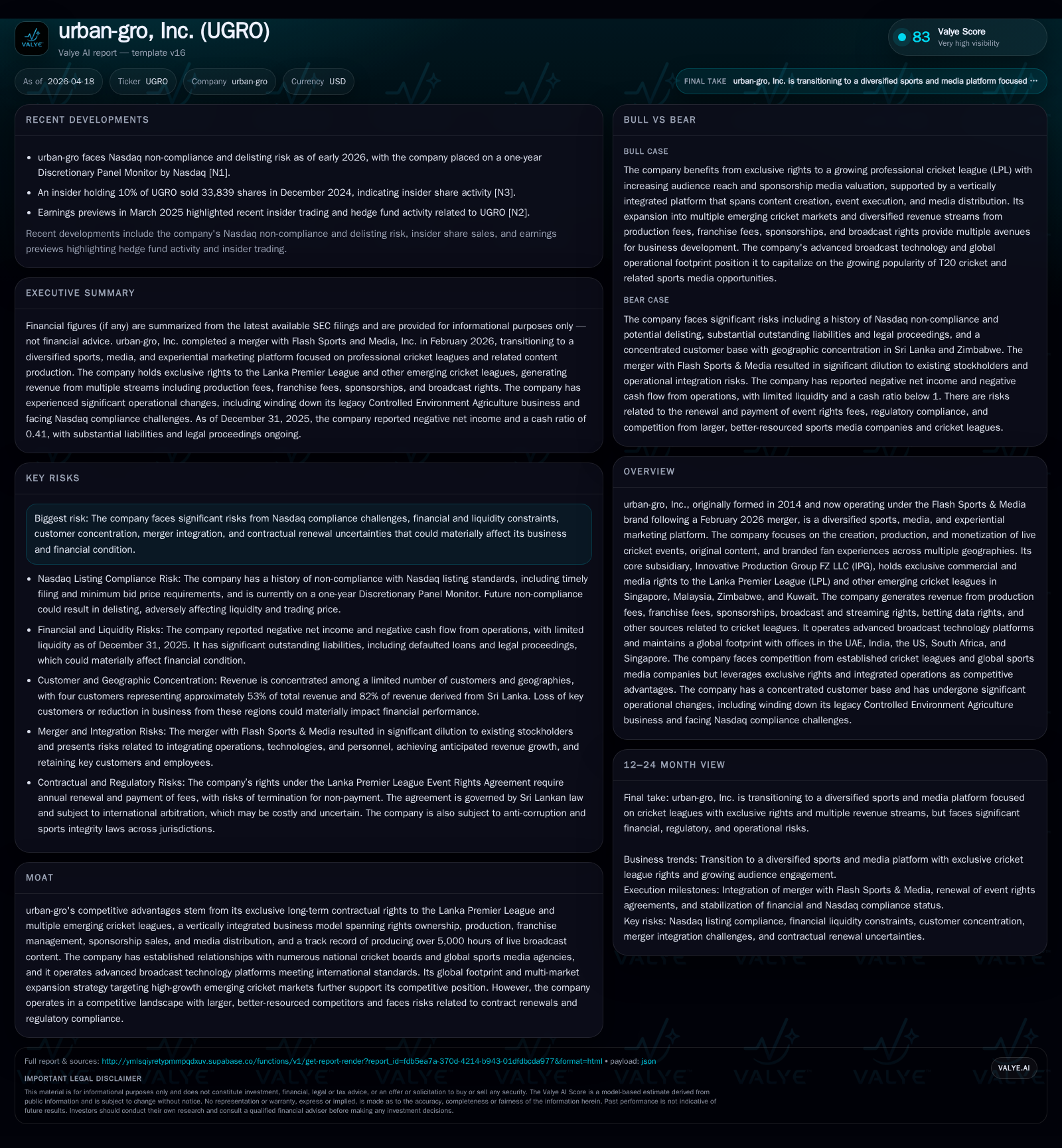

urban-gro, Inc. transformed through a 2026 merger into a diversified sports media platform, leveraging exclusive cricket rights while managing significant financial headwinds.

In February 2026, urban-gro, Inc. completed a transformative merger with Flash Sports & Media, shifting from controlled environment agriculture to a global sports media and event production company. The firm holds exclusive commercial rights to professional T20 cricket leagues such as the Lanka Premier League, driving multi-channel revenue streams. Despite this strategic repositioning, urban-gro faces material financial challenges including steep revenue declines in 2025, sustained net losses, and liquidity constraints. Operational cash flow turned positive in 2025 after several years of negative trends, signaling early stabilization. However, high customer concentration in Sri Lanka and Zimbabwe, contract renewal uncertainties, and merger integration risks remain key concerns.

Company Background and Strategic Transition

urban-gro, Inc., founded in 2014 initially as a controlled environment agriculture (CEA) company, underwent a major strategic transformation following its merger with Flash Sports & Media, Inc., completed on February 17, 2026 [S1][S25]. This transaction marked the company's exit from legacy CEA operations which were largely wound down by late 2025. Post-merger, the company operates under the Flash Sports & Media brand as a diversified global sports media platform focused on live event production, original content creation, and branded fan experience monetization across multiple geographies [S1].

The key operating subsidiary post-merger is Innovative Production Group FZ LLC (IPG), which holds exclusive commercial and broadcast rights for professional T20 cricket leagues including the Lanka Premier League (LPL) and emerging franchises in markets such as Singapore, Malaysia, Zimbabwe, and Kuwait [S1][S25]. This vertically integrated model encompasses league management, franchise support services, sponsorship sales, broadcast distribution, and betting data licensing.

Historical Financial Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 17 | -22 | 1 | -18 | -56.5% | +39.4% |

| 2024 | 40 | -36 | -3 | -36 | -95.4% | |

| 2023 | -19 | -11 | -17 | -22.3% | ||

| 2022 | -15 | -13 | -13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1 | 48.9 | |

| 2024 | 0 | -3 | 148.1 |

| 2023 | 0 | -12 | -93.1 |

| 2022 | 4 | -13 | -44.0 |

Source: SEC companyfacts cache [F1].

The company experienced a sharp revenue decline exceeding 56% from fiscal year 2024 to 2025 as it transitioned away from its legacy business lines [F1]. Operating losses improved significantly but remained large at approximately $18 million for FY25 compared to over $35 million in FY24 [F1]. Net losses also narrowed but persisted at over $22 million in FY25 [F1].

A notable improvement was seen in operating cash flow which turned positive at approximately $841 thousand in FY25 after several years of negative cash flow generation [F1]. Capital expenditures increased moderately to support infrastructure necessary for live content production.

However, liquidity remains critically strained with current assets reported at only $10.6 thousand against current liabilities exceeding $45 million at December 31, 2025 [F1]. The company's balance sheet shows a substantial equity deficit deepening from roughly -$24.6 million to -$45.2 million during this period [F1], underscoring solvency challenges.

Growth Outlook and Milestones

urban-gro’s future growth hinges on monetizing its exclusive cricket league rights portfolio—particularly the LPL—and expanding into other emerging markets where IPG holds or seeks rights [S25]. The company’s vertically integrated model leverages proprietary production capabilities with over 5,000 hours of live broadcast experience supporting scalable content creation tailored for global distribution [S5].

Key growth drivers include increasing sponsorship valuations—LPL sponsorship media value reportedly grew from around $54.5 million initially to about $176.5 million by season five—and international media partnerships facilitating broader distribution [S5]. Expansion into high-growth regions such as Southeast Asia and Africa offers additional scaling opportunities.

Significant risks temper this outlook:

- Heavy dependence on annual renewals of the Master Event Rights Agreement with Sri Lanka Cricket creates revenue uncertainty despite automatic one-year renewal provisions [S13].

- Customer concentration remains elevated with four customers representing approximately half of total revenues as of recent years; geographic concentration is primarily Sri Lanka (82%) and Zimbabwe (18%) [S13][S25].

- Regulatory challenges include evolving anti-corruption laws across jurisdictions and restrictions on sports betting advertising affecting certain revenue streams [S9][S22].

- Intense competition exists from established cricket leagues like IPL alongside global sports media firms with deeper resources [S5].

- Integration risks arise from combining operations of legacy urban-gro with Flash subsidiaries amid ongoing organizational change [S18].

Investors should monitor contract renewals each March for the Sri Lanka Cricket agreement—the cornerstone commercial arrangement—as well as quarterly financial results for signs of revenue recovery or further erosion. Progress on Nasdaq compliance following prior deficiencies will also be important [S19]. Liquidity improvements or recapitalization efforts remain critical given the extreme working capital deficits noted at year-end FY25 [S6][S11].

Capital Allocation and Returns Profile

Urban-gro has not declared dividends nor conducted share repurchases since fiscal year 2022 when small buybacks ceased amid worsening financial conditions [F1][S10]. The company’s capital allocation reflects prioritization of operational continuity over shareholder returns given persistent losses.

The net loss relative to shareholders’ deficit suggests an approximate absolute loss magnitude equivalent to about half (-48.9%) of the negative equity base for FY25—a reference illustrating ongoing value erosion absent turnaround efforts [F1]. Free cash flow was positive in FY25—operating cash flow less capex approximated $543 thousand—indicating early improvement though overall financial health remains fragile [F1].

Industry Context

Urban-gro's repositioning situates it within the dynamic T20 cricket broadcasting ecosystem that includes dominant leagues such as IPL and Big Bash but also emerging markets where demand for localized professional cricket is growing rapidly [S5]. Competitive advantage derives from exclusive market contracts enabling control across multiple stages of content production and distribution—a vertical integration increasingly important in sports media.

The company’s proprietary broadcast technology infrastructure supports adaptable clean feeds essential for satellite TV broadcasters and OTT platforms globally amid evolving viewer preferences for multi-angle live coverage.

Regulatory complexity related to international anti-corruption frameworks and sports betting advertising constraints adds operational challenges given cross-border content distribution footprints.

Conclusion

urban-gro’s transformation into Flash Sports & Media reflects a strategic bet on niche global sports media markets anchored by expanding interest in professional cricket beyond traditional powerhouses. While holding valuable exclusive rights facilitating multi-channel revenue potential supported by established broadcast expertise,[S1][S5] the company faces pronounced financial difficulties characterized by large recurring losses and acute liquidity shortfalls as reported for fiscal year ending December 31, 2025.[F1] Concentrated customer exposure combined with integration execution risks emphasize caution regarding near-term outlooks.[S9][S18]

Future success depends critically on securing favorable contract renewals particularly with Sri Lanka Cricket; diversifying revenues internationally; improving working capital fundamentals; maintaining compliance amidst evolving regulatory regimes; broadening customer base; managing competitive pressures effectively; and ultimately achieving sustainable profitability supported by positive operating cash flow expansion.

Investors should closely watch upcoming quarterly filings for developments on these fronts alongside updates on Nasdaq compliance status as indicators of financial stabilization or deterioration.

This analysis is provided solely for informational purposes without investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments