Dream Homes & Development Corp. Focuses on Build to Lease and Lot Sales for Growth

Dream Homes transitions from traditional homebuilding to build-to-lease and improved lot sales, capturing evolving real estate market demand.

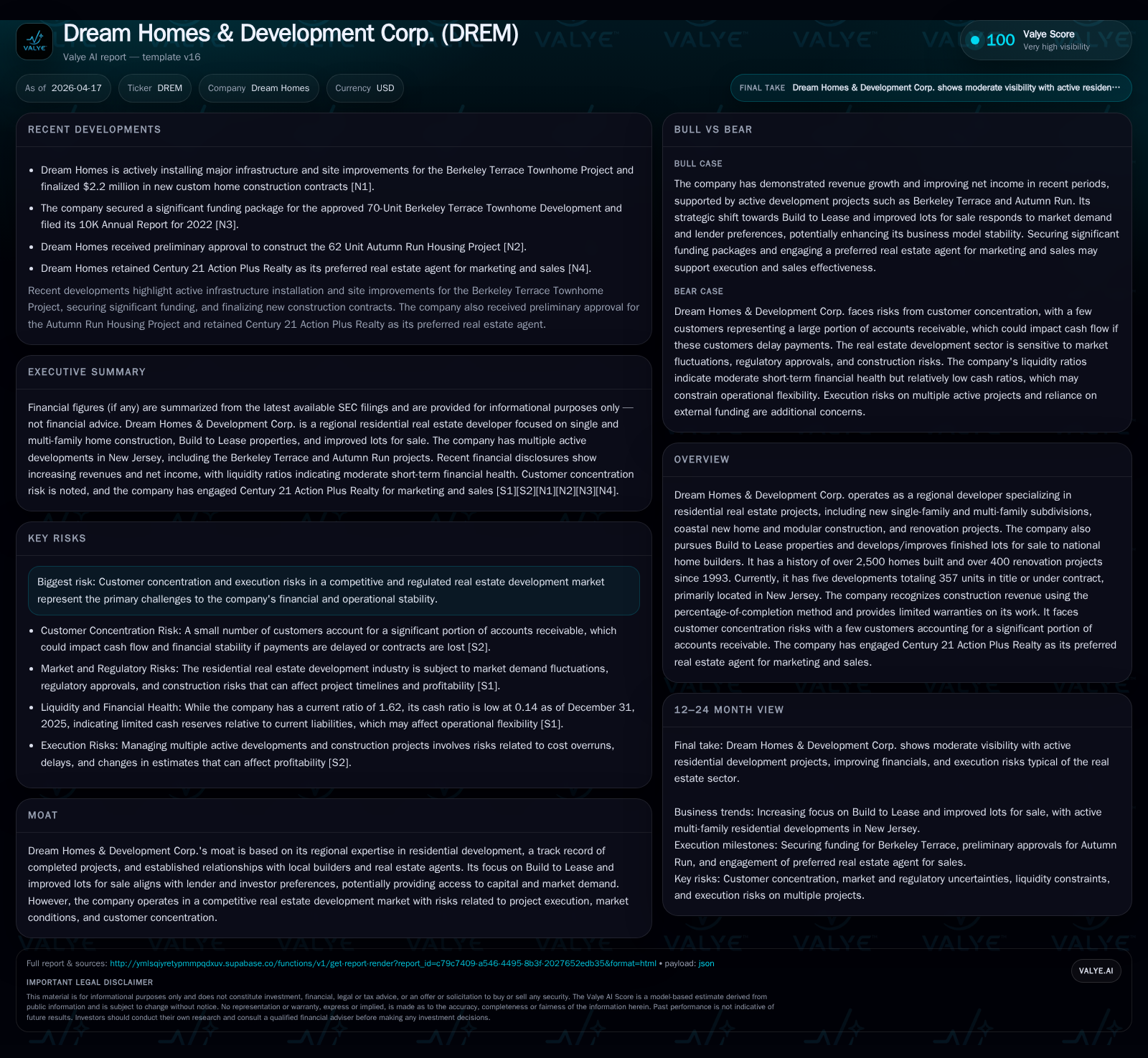

Dream Homes & Development Corp. has a long track record in residential development, primarily in New Jersey, delivering over 2,500 homes and 400 renovations since 1993. Recently, it has shifted strategy to focus on build-to-lease multi-family units and selling improved finished lots to national builders, aligning with lender preferences and institutional demand for stable rental income streams. Despite a recent revenue dip and tightening margins, the company generated robust operating cash flows in 2025 and maintains moderate liquidity amid a competitive environment marked by customer concentration risks. The transition into build-to-lease assets promises to diversify revenue sources and capitalize on regional rental shortages and favorable financing conditions.

Historical Growth Trajectory and Past Performance Drivers

Dream Homes & Development Corp., established in 1993, has developed over 2,500 new homes alongside more than 400 renovation projects focusing on single-family and multi-family residential developments primarily within New Jersey [S1]. The company recognizes revenue using the percentage-of-completion method consistent with industry practice.

Financially, revenues declined from approximately $2.93 million in fiscal year 2017 to around $2.57 million in fiscal year 2018, continuing into recent years with a roughly 12.4% decrease year-over-year through 2025 [F1]. Operating income decreased by 26.4% from $1.5 million in FY2024 to about $1.1 million in FY2025, while net income increased by approximately 11%, reaching $418K in FY2025 [F1]. This reflects efforts toward operational cost management amid fluctuating sales volumes.

Operating cash flow demonstrated a notable increase of over sixfold in fiscal year ended December 31, 2025, generating approximately $3.95 million despite underlying revenue softness—indicative of improved working capital management and project execution [F1]. Capital expenditures rose sharply by about 346%, reaching nearly $290K as the company invested significantly in land acquisitions and development improvements aligned with its evolving strategy [F1].

Historical performance (annual)

| FY | Net ($) | CFO ($mm) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 418271 | 4 | 1104614 | +11.2% |

| 2024 | 375985 | -1 | 1499918 | +486.1% |

| 2023 | -97379 | 0 | 68803 | -163.2% |

| 2022 | 154090 | 1 | 205522 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 30.2 |

| 2024 | 15.8 |

| 2023 | -15.4 |

| 2022 | 24.1 |

Source: SEC companyfacts cache [F1].

This table highlights key financial metrics illustrating declining topline paired with margin compression but strong cash flow generation.

Market Conditions Shaping Business Model Evolution

Dream Homes operates within a cyclical residential real estate development industry sensitive to macroeconomic factors including employment levels, consumer confidence, mortgage interest rate fluctuations, and construction material cost volatility [S1]. The New Jersey market reflects a significant shortage of rental properties across demographics including first-time homebuyers, retirees, and young professionals seeking leasing flexibility.

This rental scarcity alongside lender preference for financing projects generating recurring rental income rather than one-time home sales has driven Dream Homes’ strategic pivot toward build-to-lease multi-family units and finished lot sales [S1]. Institutional investors such as pension funds and insurance companies increasingly seek stabilized leased residential assets offering predictable cash flows—a trend that supports developers adapting their product mix accordingly.

Strategic Shift: Embracing Build to Lease and Finished Lots

In response to these trends, Dream Homes plans to convert two existing multi-family developments totaling 79 units from 'Build For Sale' to 'Build To Lease,' retaining ownership post-construction for rental income over an indefinite period [S1].

Additionally, the company is expanding its finished lot sales business targeting national builders eager for turnkey lots ready for immediate construction starts [S1]. This dual focus aligns with lender risk assessments favoring long-term asset-backed returns over transactional sale cycles.

This shift creates a fourth division supplementing core operations: new custom homes construction, renovation/elevation projects, finished lots for sale, now augmented by long-term multi-family leasing operations [S1]. The company also holds options on several parcels providing opportunities for further expansion of these initiatives contingent on market conditions.

Financial Overview: Profitability and Cash Flow Trends

Profit margins have been pressured by pre-set pricing commitments—often fixed up to twelve months ahead—and inflationary cost increases that were not always fully recoverable due to competitive pricing [S1]. Nonetheless, operating expenses slightly decreased entering FY2025 contributing to improved operational leverage [F1].

The substantial increase in operating cash flow (+610%) underscores effective cash conversion despite softer revenues; this is vital given elevated capital expenditure requirements related to land development supporting strategic pivots (+346% capex) [F1]. Free cash flow after capex remains strongly positive at approximately $3.9 million.

An approximate return on equity based on FY2025 net income relative to book equity suggests robust profitability near 30%, reflecting management’s ability to improve earnings amid industry cyclicality [F1].

Capital Allocation: Liquidity and Debt Positioning

As of December 31, 2025 total stockholders’ equity was approximately $1.39 million against liabilities near $6.64 million resulting in a current ratio around a moderate 1.62—indicating reasonable short-term liquidity though meaningful leverage relative to capitalization levels [F1].

The company maintains sizable loans payable including mortgages refinanced under a new funding facility for the Autumn Run manufactured home development valued at $13.6 million closed mid-2025; this facility covers refinancing existing debt plus site infrastructure costs and vertical construction financing [S14][S15].

There are no recent dividends or share repurchases reported; historical buybacks occurred several years ago without clear ongoing capital return policy [F1][S3][S4]. Insider ownership remains concentrated with Vincent Simonelli controlling nearly 57% of shares along with related party loans contributing governance influence [S1].

Risks: Customer Concentration and Execution Challenges

Customer concentration risk persists—top three customers accounted for more than half of accounts receivable at year-end periods—posing credit risk should any significant customer default or delay payments materially impacting cash flows [S7][S9][S19]. Project execution risks remain inherent due to competitive real estate environments coupled with regulatory compliance that can delay schedules or increase costs unexpectedly.

Minor ongoing legal proceedings are disclosed but considered immaterial without expected financial impact; the company defends these vigorously maintaining transparency [S1][S3]. Pricing commitments made well ahead of delivery combined with inflationary pressures create potential margin squeeze especially if buyers cancel or renegotiate contracts during adverse market conditions.

What to Monitor: Upcoming Milestones and Industry Signals

While explicit forward guidance is absent from filings or news releases currently, monitoring successful lease-up rates of converted multi-family units under build-to-lease strategy is critical as it validates the new recurring revenue stream akin to institutional real estate investment products.

Additionally, proceeds from improved lot sales indicate strong demand from national builders with recent transactions shortly after fiscal year-end providing visibility into near-term inflows [S8][S14]. Changes in lending environments affecting interest rates or credit availability could materially impact project feasibility given reliance on mortgage financing.

Broader housing market indicators such as employment data and consumer sentiment should be observed as bellwethers influencing buyer behavior impacting Dream Homes’ evolving lease versus sale product mix.

This analysis is based exclusively on publicly available company filings through April 17, 2026. No forward-looking recommendations are intended or implied herein; readers should perform their own due diligence using multiple information sources before forming opinions concerning Dream Homes & Development Corp.’s business prospects or financial position.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments