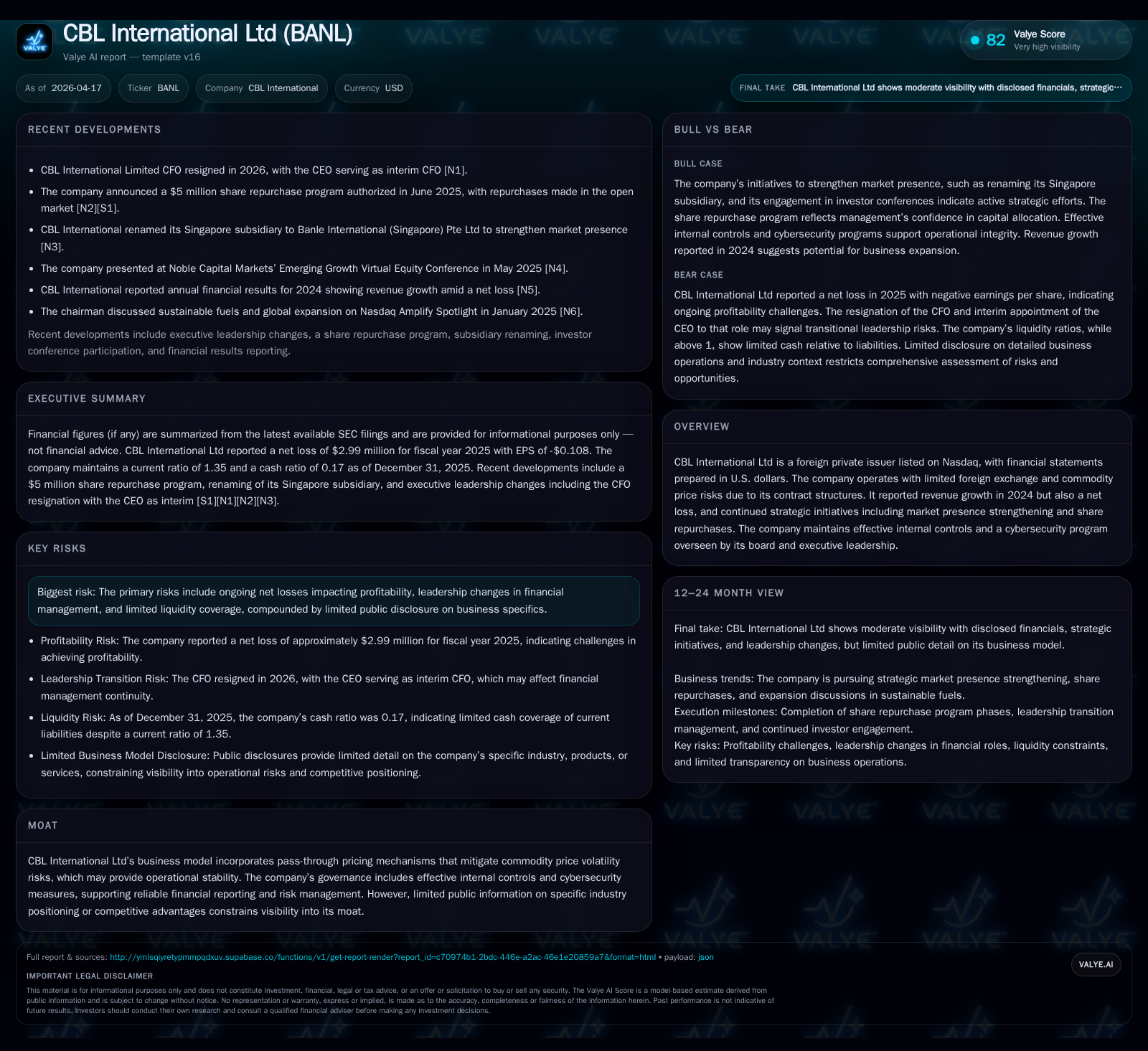

CBL International’s Expansion and Cost Discipline Drive Improved Losses Despite Revenue Pressure

The marine fuel logistics provider extended its global footprint and trimmed expenses, offsetting lower fuel prices and reporting narrower net losses in 2025.

CBL International Ltd continued expanding its service network aggressively in 2025, doubling port coverage and diversifying its customer base beyond container liners. Despite a 9% decline in revenue caused by lower bunker fuel prices, the company grew sales volume by 8% while cutting operating expenses sharply through group-wide cost controls. Its net loss narrowed by nearly 23%, aided by disciplined spending and expanding working capital facilities. Share repurchases commenced under a new program, reflecting shareholder value focus amid ongoing losses. The firm maintains a pass-through contract structure that shields it from commodity price volatility and preserves operational stability, though lingering risks include financial leadership turnover and concentrated customer receivables.

Business Overview and Past Performance

CBL International Ltd is a marine fuel logistics specialist with a focus on bunkering services at strategically important maritime ports globally. Historically centered on container liners as primary customers, the company has expanded its footprint since IPO, targeting bulk carriers and tankers to diversify its revenue streams [S1].

By the end of fiscal year (FY) 2025, CBL's network spanned over 70 ports across five continents including Asia Pacific, Europe, Australia, Africa, and Central America—a near doubling from the roughly 36 ports serviced at the time of IPO [S1]. This expansion supports broader trade routes notably across Trans-Pacific and Euro-Asia corridors that underpin much of global shipping.

Revenue declined from approximately $592.5 million in FY2024 to $538.5 million in FY2025, representing a -9.1% year-over-year decrease primarily due to significantly lower bunker fuel prices despite an increased sales volume of +8% [F1][S23]. Economically sensitive shipping patterns driven by geopolitical tensions such as Red Sea disruptions and shifting trade flows also influenced pricing flexibility [S23].

However, operating expenses decreased materially by about $1.8 million or more than 20% year-over-year to $6.9 million thanks to comprehensive cost reduction programs cutting selling & administration expenses [S12]. These cost controls contributed substantively to narrowing the pre-tax operating loss from approximately -$3.3 million in FY2024 to -$2.4 million in FY2025 (approximately +27% operating loss improvement) [F1].

Despite revenues contracting, net losses improved meaningfully to nearly -$3.0 million (FY2025) compared to almost -$3.9 million (FY2024), marking a ~23% reduction increase largely linked to expense control and enhanced operational efficiency [F1][S12].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | 4 | -2 | 2641 | +22.8% |

| 2024 | -4 | -2 | -3 | 144446 | -441.8% |

| 2023 | 1 | -10 | 2 | 773863 | -69.3% |

| 2022 | 4 | 3 | 5 | 373111 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 4 | -15.0 |

| 2024 | -2 | -16.9 |

| 2023 | -11 | 4.5 |

| 2022 | 3 | 30.4 |

Source: SEC companyfacts cache [F1].

Cash flow from operations swung positively in FY2025 (+$4 million), contrasting losses recorded previously, which reflects improving working capital management despite ongoing capital expenditures remaining minimal [F1]. Capex dropped sharply (-98%) signaling reduced investment intensity likely linked to recent expansion completion or reprioritization [F1].

Growth Strategy and Future Prospects

CBL’s growth blueprint is predicated on further enlarging geographic reach—specifically within high-growth hubs across Asia Pacific—and integrating sustainable fuels into its product suite including biofuels, LNG, green methanol, ammonia, and hydrogen [S1]. This strategy aligns with global maritime decarbonization efforts led by regulatory authorities like IMO.

Expansion efforts are bolstered by established supplier relationships ensuring competitively priced supply lines paired with stringent due diligence maintaining regulatory compliance—a critical advantage as environmental mandates tighten [S1]. CBL’s presence across major trade corridors (Euro-Asia, Trans-Pacific) facilitates access to premium clients whose operational requirements emphasize reliability and integrated refueling solutions.

Sales concentration among top five customers decreased over recent years — from above 70% toward approximately 60% by end-2025 — reflecting success diversifying beyond leading container liner clients into bulk carrier and tanker segments while growing overall volumes within key customer cohorts [S18].

Short-term sales volume growth faces external pressures including volatile geopolitical environments affecting routing efficiency (e.g., Red Sea tensions extending voyage durations), competitive pricing pressure reducing margins temporarily [S23], but expanded port coverage aims to mitigate some operational risks through route flexibility.

Capital Allocation and Returns

CBL raised approximately $1.375 million through a private placement in August 2024 supporting network growth and sustainable fuel initiatives while filing shelf registration enabling up to $50 million issuance capacity for broader funding flexibility [S21]. In early-to-mid-2025 it initiated an at-the-market equity offering capped near $2.6 million for opportunistic capital raises [S21].

A share repurchase program authorized mid-2025 permits up to $5 million buybacks over three years; during FY2025 management repurchased about ~52K shares worth roughly $49K as part of this initiative signaling confidence in intrinsic value despite ongoing operating losses [S10][S11][S13]. Subsequent repurchases occurred post year-end under favorable market conditions [S13].

No dividends have been declared or paid reflecting focus on liquidity preservation during transition toward profitability.

Liquidity Position and Financial Structure

As of December 31, 2025, cash & equivalents stood near $9.3 million supported by current assets totaling ~$75 million against current liabilities ~$56 million yielding a current ratio around 1.35 — an improvement suggesting sufficient near-term payment capacity amidst working capital demands [F1][S8][S15].

The company benefits from non-recourse receivable purchase agreements enabling immediate cash conversion of eligible invoices subject to bank discretion based on client credit profiles (majority factoring done under these programs not reflected on balance sheet receivables). Advances drawn under these arrangements rose moderately reflecting greater usage aligned with volume expansion [S4][S6][S15][S24].

Bank borrowings increased marginally year-over-year consistent with expanded credit facility utilization but remain short-term with no significant long-term debt maturing beyond two years reported as of December 31, 2025 [S6][S7][F1]. Interest rates on financing are fixed upon drawdowns averaging between roughly 5%-7%, elevated relative to earlier years due primarily to increased borrowings tied to financing accounts receivables [S7][S24].

The contract structure incorporating index-linked add-on pricing ensures commodity price volatility largely passes through directly without impacting gross margins materially unless timing mismatches occur between buy-sell settlements necessitating derivative hedging used sparingly as risk mitigation tools rather than speculative purposes [S6][S14][S22].

Risks and Governance Considerations

Principal risks derive from net losses hampering sustainable profitability; despite progress these remain elevated at nearly $3 million annually with negative return on equity approximated at -15% based on latest annual net loss relative to shareholder equity [$19.9M] end-2025 [F1]. Leadership stability poses challenges following CFO resignation reported early April; CEO is acting interim CFO while search proceeds potentially impacting strategic continuity or cadence of financial oversight temporarily [N1].

Liquidity constraints persist given lean buffer coverage against concentrated receivables—top five clients represent about two-thirds of accounts receivable value—raising exposure should any major counterparties experience financial distress or delayed payments warranting write-offs or more aggressive collection tactics under enforcement policies described [S14][S15].

Cybersecurity governance is emphasized with board oversight ensuring rigorous internal controls and adherence to evolving environmental regulations; however limited public disclosure on industry positioning restricts clarity on competitive moat sustainability apart from geographic breadth and contract mechanisms mitigating commodity risks .

What To Watch Next (Analysis)

Key metrics going forward will be gross margin recovery amid stabilizing bunker prices combined with continued volume expansion into newer port regions and alternative marine fuels adoption critical for navigating emerging environmental standards.

Monitoring balance sheet liquidity trends vis-à-vis credit facility access will provide insight into financial flexibility especially if geopolitical tensions disrupt shipping lanes further or cause rapid shifts in bunker demand.

Leadership appointment for CFO role may affect investor confidence impacting secondary offerings or market perception around execution capability.

Finally, management's pace on sustainable fuels integration beyond fossil bunkers will signal whether CBL can position itself competitively within a transitioning maritime energy ecosystem.

Disclaimer: This analysis is intended for informational purposes only and does not constitute investment advice or recommendations regarding securities of CBL International Ltd or any other entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments