Sunrise Real Estate Group’s Strategic Alliances Fuel Resilience Against China Market Challenges

SRRE leverages partnerships with mid-size developers to sustain operations amidst regulatory and financial hurdles in the Chinese property sector.

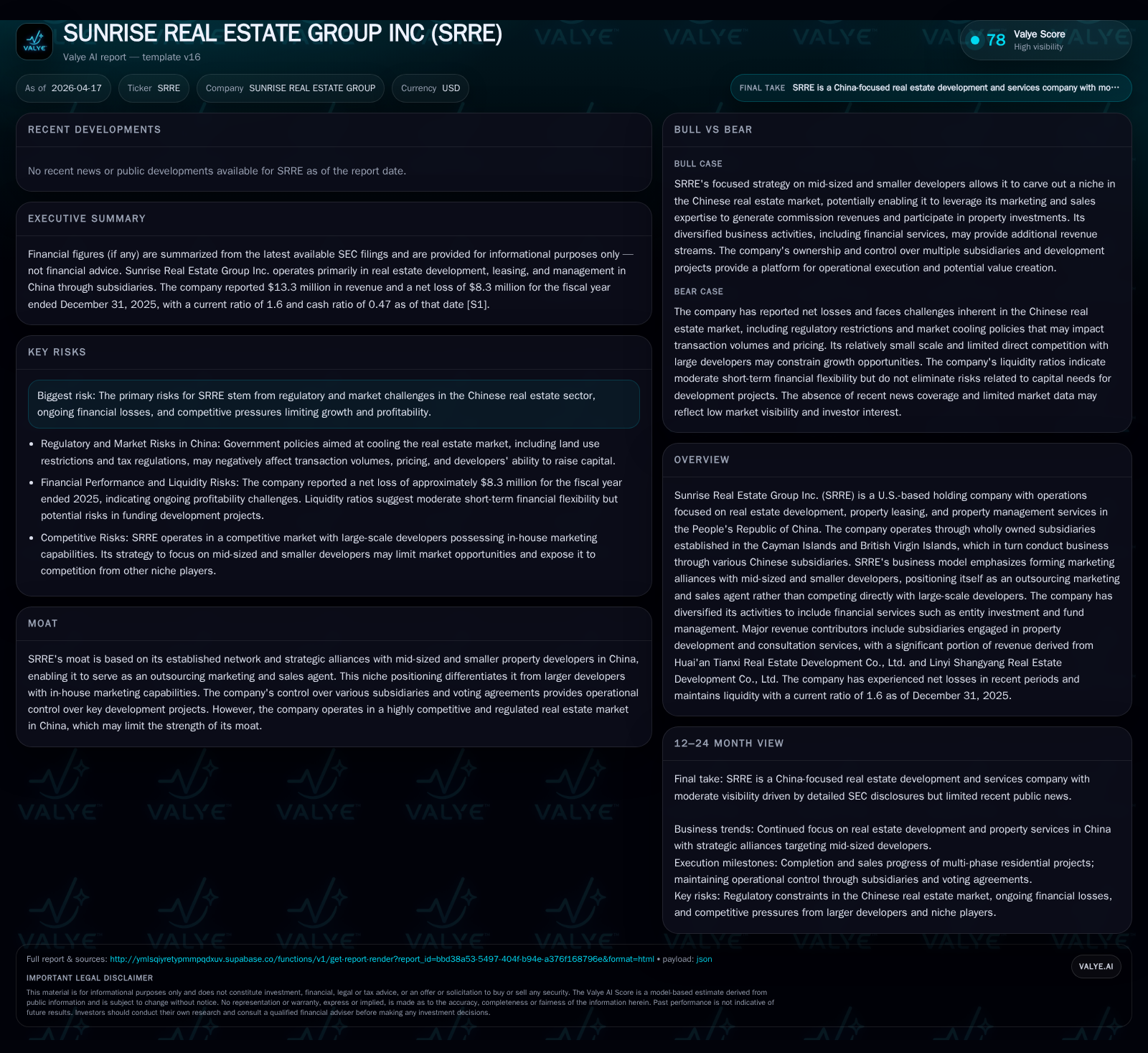

Sunrise Real Estate Group Inc. (SRRE) operates a unique business model centered on acting as an outsourcing marketing and sales agent for mid-sized and smaller real estate developers in China, differentiating itself from large developers who maintain internal marketing teams. Despite an increasingly restrictive regulatory environment and deteriorating financial performance characterized by steep revenue declines and ongoing losses, SRRE’s strategic alliances enable it to maintain a foothold in second-tier Chinese cities. The company has diversified into financial services such as entity investment and fund management, offering potential future growth avenues, although no explicit guidance has been issued. Persistent negative free cash flow and operating losses underscore the financial challenges facing SRRE, making monitoring of regulatory shifts and strategic partnership evolution critical for assessing its outlook.

Evolution of Revenue and Earnings: Tracking the Downtrend

Sunrise Real Estate Group Inc. (SRRE) has experienced a pronounced decline in top-line revenue over recent years amid challenging market conditions. As per company filings [F1], annual revenues nose-dived from $80.0 million in fiscal 2022 to just $13.3 million by fiscal 2025 — a staggering approximately 83% contraction.

Operating income metrics mirror this deterioration; losses expanded from approximately $-2.1 million in 2022 to $-3.7 million last fiscal year. Net income remained negative throughout the period with annual losses widening slightly from about $-8.4 million to $-8.3 million [F1]. These trends reveal mounting pressures stemming from declining property sales volumes and margins compressed by an unforgiving regulatory climate.

This negative financial trajectory reflects both shrinking commission fees earned from marketing activities and escalating costs related to project investments and subsidiary operations across China.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 13 | -8 | -16 | -4 | -14.9% | +8.2% |

| 2024 | 16 | -9 | -4 | -2 | -37.1% | +10.7% |

| 2023 | 25 | -10 | -4 | -1 | -69.0% | -20.2% |

| 2022 | 80 | -8 | -13 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -16 | -8.1 | |

| 2024 | 10 | -4 | -8.3 |

| 2023 | 10 | -4 | -8.5 |

| 2022 | 0 | -13 | -6.4 |

Source: SEC companyfacts cache [F1].

Note: Negative figures represent losses or declines.

Core Business Model: Outsourcing to Mid-sized Developers in China

Unlike large-scale Chinese real estate conglomerates that typically maintain substantial internal marketing departments, Sunrise Real Estate Group positions itself as a marketing outsourcing partner specifically tailored to mid-sized and smaller developers [S1], . This strategic niche minimizes direct competition with industry behemoths while tapping into a segment underserved by marketing agencies.

Sunrise earns commission fees calculated as percentages of sales prices on new development projects it assists in selling [S12]. With a broad network spanning multiple subsidiaries concentrated primarily on second-tier urban centers like Linyi and Huai'an—the company focuses on managing plot ratio controls effectively to navigate urban density regulations limiting residential unit sizes.

Operational control is cemented through carefully structured equity stakes combined with voting agreements—for instance controlling 80% of voting rights at Linyi Shang Yang Real Estate Consultation Company Limited—enabling Sunrise to steer marketing strategies while sharing investment risk with partners [S19], [S23]. This ownership structure allows flexible collaboration without overstretching capital resources.

Regulatory Headwinds and Sector Risks Shaping Growth Prospects

China’s government maintains stringent interventions designed to cool speculative housing markets including:

- Enforcing down payments upwards of 50% for multiple home purchases;

- Imposing a substantial capital gains tax (20%) on resale properties;

- Tightening land use administration through stricter plot ratio limits and expedited land bidding administration penalties for idled parcels [S12], [S24], [S27].

Such regulations suppress transaction volumes by discouraging speculative buying while increasing developer costs due to higher upfront land acquisition payments—in turn limiting margin expansion for marketing agents like SRRE.

The company specifically notes that these centralized policies have led to overall price declines and fewer transactions across both major cities like Beijing and Shanghai as well as across its targeted second-tier city portfolio [S4]. Against this backdrop competing platforms from large developers further constrain SRRE’s market share gains.

Future Growth Vectors and Operational Constraints

Beyond its core marketing alliance model with mid-tier developers, Sunrise has diversified activities into ancillary financial services such as entity investment management and fund management capabilities , [S5]. These moves reflect an attempt to deepen revenue streams amid sectoral contractions.

Geographically focused on second-tier cities where regulation is somewhat less stringent relative to first-tier hubs but urban growth remains robust—Sunrise aims to capitalize on emerging residential demand pockets. It has also invested significantly in ongoing development projects such as the Linyi villa-style housing complex whose phased construction continues alongside additional land acquisitions secured in recent years [S20], [S25].

However no explicit forward-looking guidance or revenue forecasts have been provided by management thus far [N/A]; hence future growth remains contingent upon easing regulatory barriers or successful scaling of its financial services ventures—a speculative prospect at present.

Financial Health: Capital Allocation, Cash Flows, and Return Measures

Sunrise’s capital allocation priorities reveal a cautious approach given tight liquidity conditions:

- Operating cash flow was deeply negative at nearly $-15.9 million in fiscal 2025 versus about $-4.2 million four years earlier,

- Capital expenditure remained nominal (~$18k), signaling restrained fixed asset investments,

- Equity declined steadily from about $131 million (FY22) to nearly $103 million (FY25), consistent with cumulative operating losses,

- Dividends were irregular; the company paid ~$10 million dividends only during FY23-FY24 despite net losses,

- No share repurchases were reported over this timeframe [F1], [S16], [S24], [S26], [S27].

The resultant return on equity hovered around negative 8%, underscoring absence of profitability despite maintaining operational scale.

Liquidity ratios remain moderate with current ratio near 1.6x supported by substantial current assets against liabilities indicating short-term solvency is preserved but long-term viability hinges on reversing negative free cash flow trends.

What Analysts Should Monitor Next: Milestones and Strategic Shifts

Key indicators warranting close attention include:

- Modifications in Chinese property market regulations or fiscal policy reversals that could relax restrictions on plot ratios or buyer financing requirements,

- Changes or expansions in SRRE’s alliance strategy—such as onboarding additional mid-tier developer partners or scaling fund management operations,

- Progress/status updates on major development project phases especially Linyi villas or Huai’an Tianxi Times projects that materially affect revenue recognition timelines,

- Potential shifts in capital allocation exemplified by increased capex or share repurchase programs indicating confidence,

- Adjustments in commission fee structures or diversification into adjacent property-related service domains.

Given the absence of formal guidance disclosures from management ([N/A]) staggered progress must be tracked via filings and operational updates to gauge recovery pathway viability.

Disclaimer: This report is for informational purposes only based on publicly available data as of April 17, 2026. It does not constitute investment advice or recommendations regarding shares of Sunrise Real Estate Group Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments