Pacific Airport Group’s Growth Challenges Amid Traffic Decline and Capital Expansion

PAC manages key airport concessions in Mexico and Jamaica but faces regulatory and traffic headwinds.

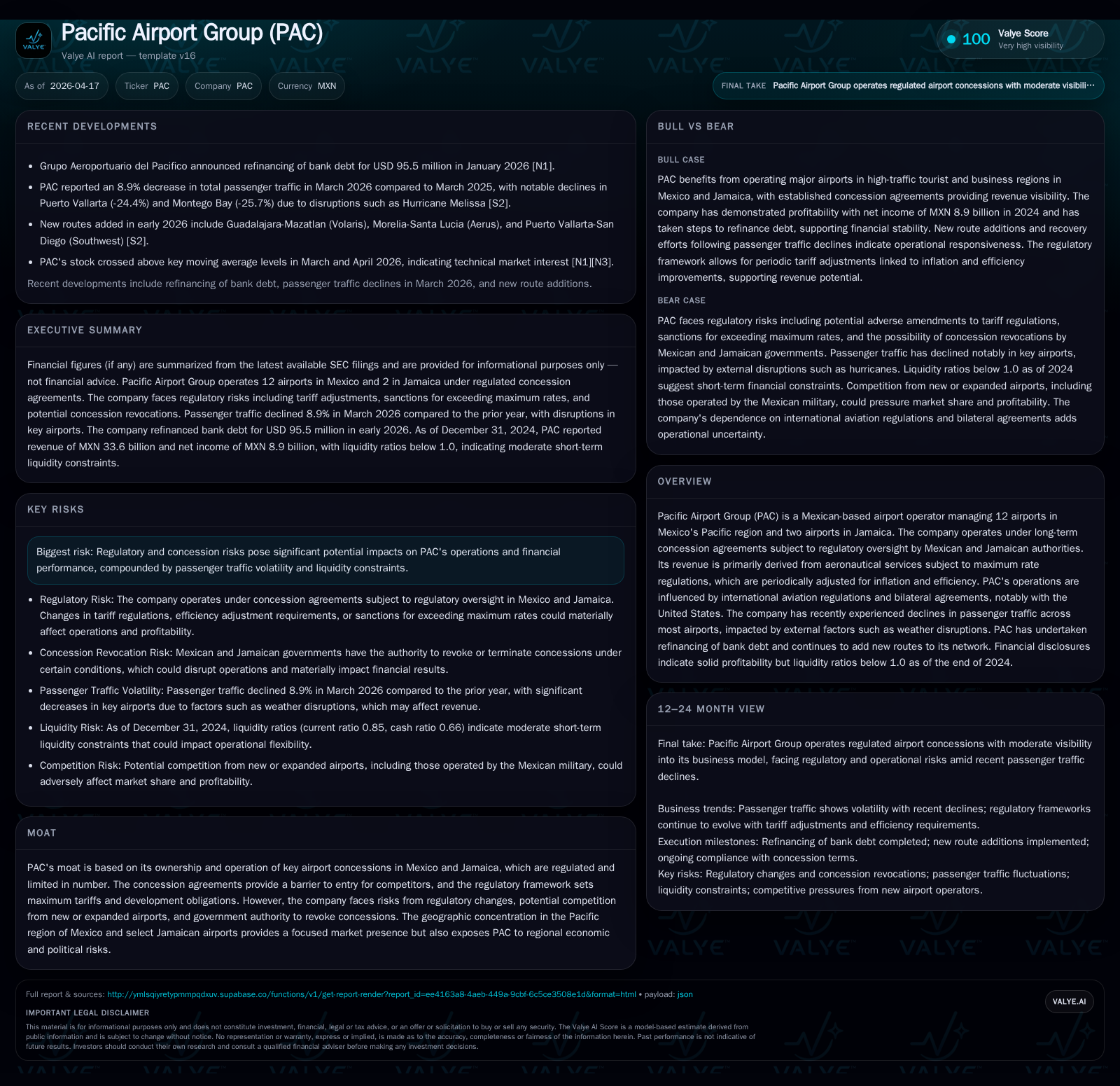

Pacific Airport Group operates 14 airports under long-term concessions mainly in Mexico’s Pacific region and Jamaica, generating regulated aeronautical revenues. The company’s revenue grew modestly in 2024 but faced a passenger traffic decline early in 2026, driven by external factors including weather disruptions and regional volatility. PAC is executing significant capital expenditures aligned with its Master Development Programs and has strategically refinanced debt to support growth. However, liquidity ratios remain below one, and regulatory changes impose uncertainties on pricing and profitability moving forward.

Company Overview

Pacific Airport Group (PAC) operates fourteen airports under long-term concession agreements primarily across Mexico’s Pacific region and Jamaica. Its portfolio includes major tourist destinations such as Guadalajara, Puerto Vallarta, Los Cabos, Tijuana, Kingston, and Montego Bay. These concessions are subject to regulatory oversight that limits pricing flexibility but offer structural barriers against new entrants [S1][S29].

Historical Financial Performance

For fiscal year 2024, PAC reported revenue of MXN 33.6 billion representing a modest increase of approximately 1.2% from MXN 33.2 billion in 2023 [F1]. Net income declined by about 8.4% to MXN 8.9 billion from MXN 9.7 billion the prior year [F1]. Equity increased to approximately MXN 24.6 billion yielding an approximate return on equity (ROE) of 36%, indicating efficient capital utilization despite a dip from prior levels [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 33.6 | 8.9 | +1.2% | -8.4% |

| 2023 | 33.2 | 9.7 | +21.3% | +5.5% |

| 2022 | 27.4 | 9.2 | +44.0% | +52.0% |

| 2021 | 19.0 | 6.0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | ROE% |

|---|---|---|

| 2024 | 7.5 | 36.0 |

| 2023 | 7.5 | 46.3 |

| 2022 | 7.3 | 46.3 |

| 2021 | 4.4 | 29.6 |

Source: SEC companyfacts cache [F1].

Figures per fiscal year-end; dividends exclude years without available data [F1].

Passenger Traffic Trends

Passenger volumes have shown recent volatility with a reported decline of approximately 7.6% year-over-year across PAC’s Mexican airports during March 2026 [S2]. Key tourist hubs such as Puerto Vallarta experienced sharp declines exceeding 24%, while Los Cabos and Tijuana saw mid-single digit decreases [S2]. In Jamaica, Montego Bay's traffic fell nearly 26% mainly due to disruptions from Hurricane Melissa, whereas Kingston recorded modest growth [S2]. These volume contractions reflect external disruptions including weather events and regional travel advisories impacting demand [S20].

Capital Investment and Development Programs

PAC is actively investing through its approved Master Development Programs (MDPs) which constitute binding five-year capital expenditure commitments under its Mexican concessions [S14][S15][S25]. Capital expenditures rose significantly to MXN ~12.4 billion in fiscal year 2025 compared to about MXN ~7.8 billion the previous year [S4][S14]. Investments focus on terminal expansions at Guadalajara, Los Cabos, Puerto Vallarta, runway renovations across multiple airports, technology upgrades including baggage handling systems, and sustainability initiatives such as solar farms [S14][S25]. Approximately one-third of these expenditures are internally funded via operating cash flows; the remainder is financed through debt issuances [S14][S25].

Liquidity and Capital Structure

As of December 31, 2024 PAC held cash and equivalents of approximately MXN 13.5 billion against current liabilities exceeding current assets resulting in a current ratio near .85 [F1], highlighting short-term liquidity pressures amid ongoing dividend payments exceeding MXN 7 billion annually alongside heavy capital spending and debt service obligations.

The company has managed scheduled debt maturities through refinancing activities including issuance of Ps.10.7 billion bond certificates in March 2026 intended to fund pending business combination cash considerations among other uses [S3][S7]. Other recent refinancings include extension of US$40 million loans with Citibanamex and multiple unsecured Peso-denominated bonds maturing through the early-2030s carrying fixed or floating interest rates [S5][S11][S15]. Pro forma leverage following recent issuances is around a Net Debt/EBITDA ratio of approximately 2.1x [S7].

Regulatory Environment & Risks

PAC operates within a complex framework governed by Mexican civil aviation authorities and Jamaican regulators [S13][S18][S20]. In late 2023 the Mexican Federal Civil Aviation Agency amended tariff base regulations affecting fee structures starting January 1, 2025 introducing uncertainty beyond the current five-year cycle ending in late-2029 [S1][S13]. Future regulatory actions or stakeholder pressures—including from airlines or antitrust bodies—may further constrain pricing power.

Jamaican operations face additional challenges from evolving tax laws, security concerns including U.S travel advisories related to crime rates affecting passenger volumes or operational costs [S20], as well as environmental compliance requirements such as Mexico's CO2 emissions market mandating infrastructure investments like wastewater treatment upgrades [S12][S23].

Strategic & Governance Considerations

As a holding company relying on subsidiaries for dividend streams subject to legal restrictions, PAC faces governance risks compounded by shareholder ownership limitations that may deter acquisitions but also affect market perception [S13][S17][S21]. The company is progressing with internalization of technical assistance services previously outsourced—a process carrying execution risks that could delay realization of expected synergies tied to a recently approved business combination valued at nearly US$488 million cash consideration payable imminently [S13][S21].

Outlook & Near-Term Milestones

Early-2026 passenger traffic declines pose headwinds for PAC’s aeronautical revenue base requiring close monitoring of recovery trends amid geopolitical uncertainties.

Substantial capital expenditure commitments under Master Development Programs totaling over Ps.32 billion through end-2029 necessitate sustained financing access paired with prudent cash flow management [S15][S22]. Upcoming debt maturity profiles call for continued refinancing vigilance.

Regulatory clarity post-2029 on tariff structures remains uncertain with potential medium-to-long term implications for revenue.

Investors should watch for progress on closing and integrating the pending business combination alongside updates on Jamaican traffic developments impacted by travel advisories.

Summary

PAC holds a strategically important position operating a concentrated portfolio of regulated airports offering competitive insulation via concession barriers but exposed to significant regulatory dependency.

Steady historical growth with solid profitability reflected by a healthy ROE (~36%) contrasts with recent passenger setbacks stressing revenue prospects amid rising capital intensity driven by infrastructure expansion programs.

The company balances dividend distributions, capital investment demands, and refinancing obligations within a carefully structured capital framework.

Regulatory ambiguities beyond the current tariff cycle combined with emerging tax burdens underscore embedded risks within PAC’s operating environment.

Execution on investment programs, traffic recovery trends, liquidity management, and stakeholder relations will be critical determinants shaping PAC’s trajectory over coming years.

Disclaimer: This analysis is based solely on publicly available data from official filings and news reports as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments