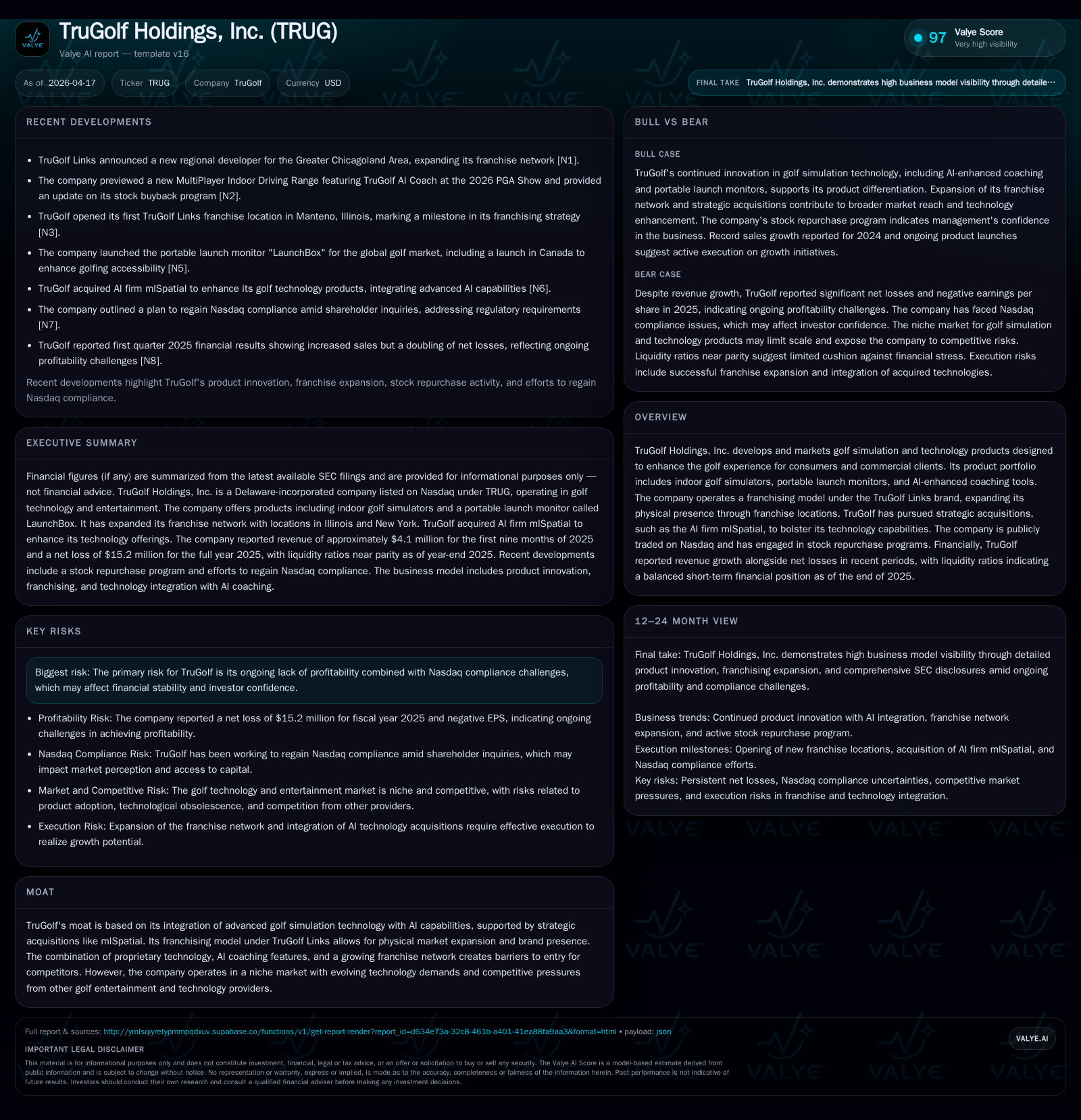

TruGolf Holdings Advances AI-Driven Golf Simulations While Managing Profitability Challenges

TruGolf integrates advanced AI technology and franchise growth to drive revenue amid ongoing net losses and capital discipline measures.

TruGolf Holdings is expanding its footprint through a franchising model and strategic acquisitions, notably integrating AI capabilities into its golf simulation products. Despite revenue growth to approximately $21.9 million in 2024, the company continues to face significant net losses, which deepened to over $15 million in 2025, reflecting intensified operating expenses linked with scaling efforts. Capital allocation remains disciplined with share repurchases under a $2 million program and balanced liquidity of roughly $10.5 million as of year-end 2025. Profitability challenges persist, but improved operating cash flows hint at gradual operational stabilization.

Evolution of TruGolf’s Growth: Technological Integration Meets Market Expansion

TruGolf Holdings has steadily advanced its position by marrying cutting-edge golf simulation hardware with AI-enhanced software applications. The company's product suite delivers indoor golf simulators with portable launch monitors complemented by AI-driven coaching tools designed for both consumer and commercial use. This technological integration underpins growing demand leading into fiscal 2024, with total revenues nearing $21.9 million [F1].

Parallel to product innovation, TruGolf has pursued market expansion through the 'TruGolf Links' franchising model, enabling physical service points that reinforce brand visibility and generate steady streams beyond direct product sales . This dual approach leverages the network effect of franchised venues while embedding proprietary simulation technology advantageously within a competitive niche.

The company’s moat is delineated by this synergy between technology — notably its acquisition of AI specialist mlSpatial — and physical presence expansion via franchises, establishing barriers against emerging competitors aiming to penetrate golf entertainment tech . As such, TruGolf's historical revenue growth reflects both organic demand for immersive golf experiences and strategic footprint broadening.

Financial Performance Review: Revenue Gains Amid Expanding Net Losses

While revenue rose significantly through 2024, TruGolf's income statement reveals mounting net losses culminating in -$15.2 million by fiscal year-end 2025 [F1]. This represents a sharp worsening of 73% relative to the prior year's net loss of approximately -$8.8 million [F1]. Operating income similarly eroded from -$2.1 million in 2024 to -$6.1 million in 2025, evidencing the scale-up pressures borne from R&D intensification, franchise support costs, and ongoing integration expenses tied to acquisitions.

Operating cash flow improved markedly by approximately 57% year-over-year but remained negative at around -$1.7 million for the latest fiscal period [F1]. Such cash flow dynamics suggest that while operational efficiency is incrementally advancing, cash burn continues as the company invests in evolving its product capabilities and extending distribution channels.

Capital expenditures surged over fourfold in 2025 compared to prior year levels (from ~36k USD to ~205k USD), indicating enhanced investment in equipment or infrastructure required to support growth initiatives [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -15 | -2 | -6 | 205443 | -73.1% |

| 2024 | -9 | -4 | -2 | 36339 | -2097.6% |

| 2023 | 0 | -1 | +3.3% | ||

| 2022 | 0 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -354.1 |

| 2024 | -4 | 189.5 |

| 2023 | 6.2 | |

| 2022 | 11.0 |

Source: SEC companyfacts cache [F1].

Table notes: Revenue figure is for FY2024 as latest available; operating income and net income are available for FY2024-FY2025 [F1].

Franchising Model Growth and Strategic Acquisitions: Scaling Physical and Technological Presence

TruGolf's franchising model creates tangible market touchpoints that extend its reach well beyond direct sales channels. Under the 'TruGolf Links' brand umbrella, franchise locations leverage the company's core simulation systems enhanced by proprietary software assets including AI-enabled coaching features . This structure permits efficient rollouts leveraging franchise unit economics that ideally promote recurring service-based revenues.

Strategically acquiring mlSpatial positions TruGolf ahead technologically by embedding advanced AI solutions within its coaching ecosystem — an important differentiator given increasing customer expectations for analytic insight integrated directly into play experiences . Such moves enhance user engagement and customer stickiness in an industry where hardware commoditization risks escalating.

The combined approach fosters competitive insulation: franchises broaden geographic penetration while technology advancements raise switching costs for end-users seeking high-fidelity golf simulation enriched with AI-driven personalized feedback.

Outlook on Growth Drivers and Headwinds: Balancing Innovation with Market Niche Dynamics

Looking forward, TruGolf’s growth is anchored on continued innovation in simulation accuracy coupled with expanded franchise deployments generating recurring revenues. The incorporation of AI coaching tools aligns well with broader trends toward data-enabled performance improvement favored by serious golfers . However, inherent risks include sustaining sizeable investment outlays that weigh on profitability amid a niche market constrained by specialized demand patterns.

Competition from other golf entertainment providers presents an ongoing challenge as technological differentiation must keep pace with innovations from larger players potentially targeting casual segments with lower-cost alternatives . Moreover, maintaining investor confidence amidst persistent losses and Nasdaq listing compliance issues adds another layer of complexity.

Capital Structure Discipline: Liquidity, Stock Repurchases, and Debt Overview

TruGolf reported robust liquidity entering fiscal year-end 2025 with around $10.5 million in cash and equivalents alongside current assets totaling approximately $15.5 million versus current liabilities close to $14.4 million — yielding a current ratio near parity at 1.07 [F1][S20]. This reflects sound short-term financial positioning enabling ongoing operations without immediate funding pressure.

Capital allocation highlights include continuation of a stock repurchase program capped at $2 million total authorized spend. As of early February 2026, about $1.67 million remains available under this buyback authorization after repurchasing roughly 423 thousand shares at average prices between $0.75–$0.85 per share [S4][S5]. Such measured repurchases signal confidence in underlying equity value despite ongoing earnings volatility.

Debt levels remain moderate without significant reported leverage burdens adverse to operational flexibility or Nasdaq compliance considerations currently focused more on corporate governance aspects than financial covenants [S6][S7][S8][S20][S25].

Profitability Challenges and Return Metrics: Understanding TruGolf’s Earnings Trajectory

Despite top-line gains through product expansion and franchising efforts, TruGolf’s profitability profile remains strained; latest ROE approximation stands near -354%, broadly reflecting accumulated net losses eroding shareholders’ equity base [F1]. While this negative return underscores ongoing earnings challenges typical for emerging tech-centric firms scaling innovative franchises, operating cash flow improvements (+57% YoY), paired with strategic cost controls implemented during FY2025 suggest gradual progress toward sustainable operations if growth drivers materialize broadly.

Ongoing losses highlight the need for close monitoring on margins tightening versus incremental economies of scale realized across both proprietary hardware/software stacks as well as recurring franchise fees from expanding location counts.

What Investors Should Watch Next: Key Milestones and Industry Headwinds

No explicit forecasts or milestone guidance were provided; consequently investors should focus on several indicators:

- Progress towards meeting Nasdaq compliance mandates related to corporate governance timing (e.g., annual meetings) which remain noteworthy regulatory risks [S21].

- Quarterly updates on the pace of new franchise openings under 'TruGolf Links' impacting recurring revenue streams.

- Adoption metrics for AI coaching platforms integrated into existing simulator offerings signaling competitive differentiation potency.

- Trends in operating leverage evidenced through narrowing net loss margins or achieving positive free cash flows implying break-even viability from core business segments.

- Potential future acquisitions or partnerships aimed at enhancing sensor fidelity or data analytics capabilities integral to premium simulation experience enhancements.

In aggregate, evaluating operational execution against these benchmarks will illuminate if TruGolf can successfully translate its innovation pipeline and physical footprint expansion into durable financial returns within a demanding market environment characterized by both technical complexity and consumer leisure spending variability.

This analysis relies exclusively on publicly filed documents and validated company disclosures as of April 17, 2026; no investment recommendations or forecasts are expressed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments