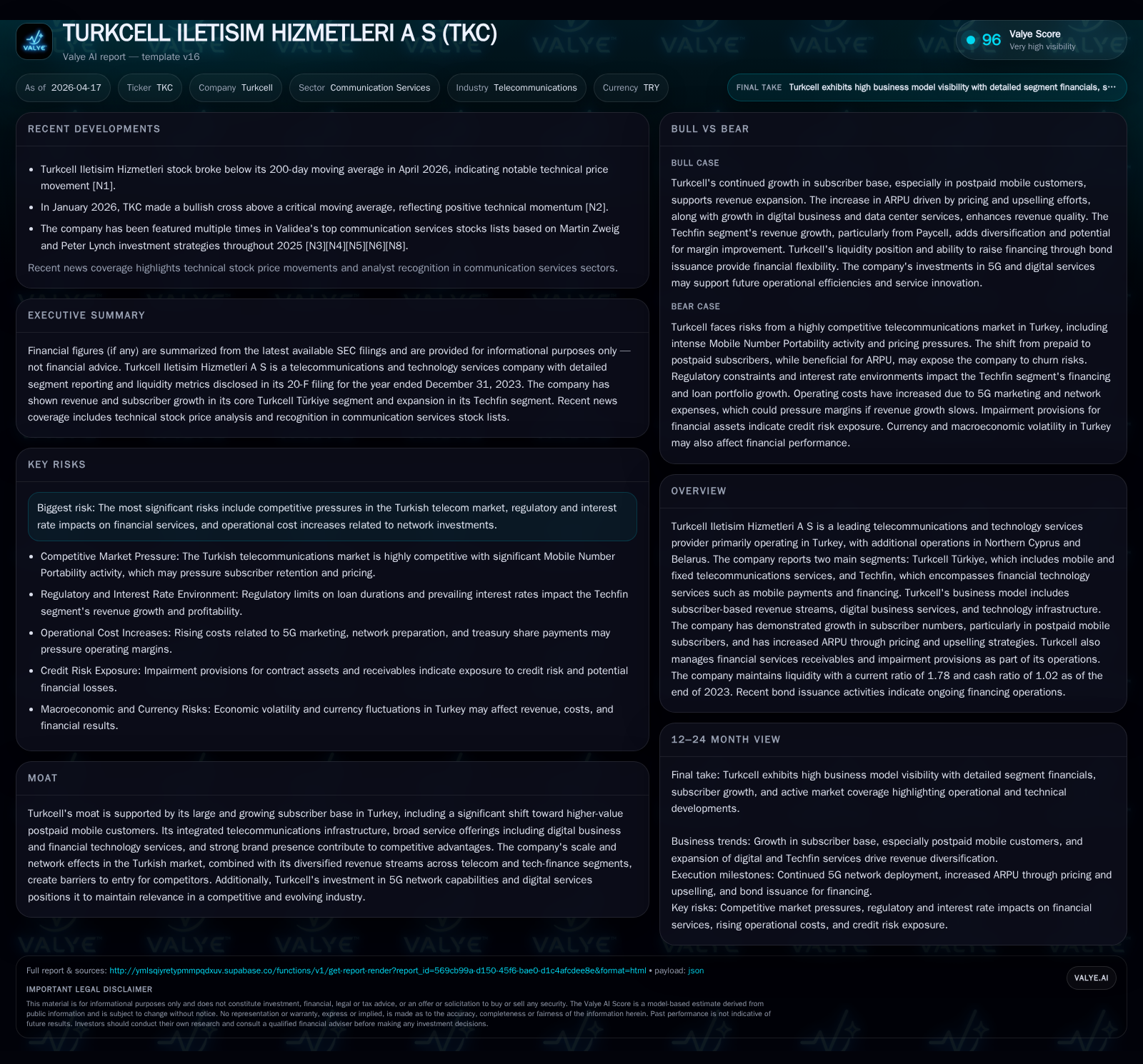

Turkcell’s Subscriber Surge Drives Transformational Growth and Strategic Financial Maneuvers

Turkcell leverages subscriber expansion and diversified financial strategies to sustain growth amid Turkey's dynamic telecom environment.

Turkcell has exhibited a remarkable revenue increase of 74% from 2022 to 2023, fueled by growing postpaid subscribers and enhanced ARPU through strategic pricing. Its hybrid business model, combining traditional telecom services with emerging Techfin offerings like mobile payments, underpins diversified revenue streams. The company maintains robust liquidity and capitalization to support large-scale investments in 5G infrastructure, leveraging a USD 1 billion Murabaha syndicated loan and other financing vehicles. Navigating Turkish regulatory complexities and currency volatility, Turkcell balances growth ambitions with disciplined capital allocation, achieving an estimated return on equity of 10.3%. Monitoring subscriber trends, regulatory renewals, and cost pressures remain critical for future performance.

Strong Growth Backed by Surging Subscribers and ARPU Expansion

Turkcell’s financial trajectory illustrates a marked acceleration in top-line growth, underpinned by its expanding subscriber base particularly favoring higher-value postpaid users. Between fiscal years 2022 and 2023, revenues surged by approximately 74%, reaching TRY 107.1 billion [F1]. This surge correlates strongly with operational metrics: the average number of mobile subscribers increased alongside a rise in mobile blended ARPU from TRY 320 in 2024 to TRY 348 in 2025 [S1][S25][S26]. This ARPU enhancement reflects effective pricing strategies combined with upselling efforts toward value-added digital services.

Impairment provisions related to financial service receivables—which stood at TRY ~1.17 billion at year-end 2025—indicate vigilant receivables quality management amidst credit risk inherent to the Techfin segment [S1]. Collections and write-offs offset impairment losses, suggesting active balance sheet stewardship.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2023 | 107.1 | 12.5 | +74.0% | +200.2% |

| 2022 | 61.5 | 4.2 | +71.3% | -17.0% |

| 2021 | 35.9 | 5.0 | +23.4% | +18.7% |

| 2020 | 29.1 | 4.2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | ROE% |

|---|---|---|

| 2023 | 2.5 | 10.3 |

| 2022 | 1.4 | 6.3 |

| 2021 | 2.6 | 22.3 |

| 2020 | 0.8 | 20.4 |

Source: SEC companyfacts cache [F1].

This table encapsulates Turkcell’s recent annual financial performance with YoY revenue growth notably rapid between FY22-23 [F1]. Net income’s doubling signals operating leverage benefits amid scaling subscriber metrics.

Dual-Segment Model: Synergy Between Telecom Services and Techfin Innovations

Turkcell operates two principal segments—Turkcell Türkiye encompassing mobile and fixed telecom services, and Techfin covering financial technology applications such as mobile payments and consumer financing [S1][S25]. This bifurcated business model delivers multiple monetization streams: subscription-based voice/data revenues coexist alongside emerging digital financial products which diversify income sources against traditional telecom market cyclicality.

Operational metrics such as churn rates have improved due to higher postpaid penetration, enhancing lifetime customer value while Digital Business revenues contribute increasingly to top-line robustness [S25][S26]. Nevertheless, the Techfin segment entails distinct risks—financial services receivables carry credit risk demanding dedicated impairment provisions, which Turkcell prudently manages via monitoring collections and conducting write-offs [S1].

This integrated telecom-financial ecosystem facilitates cross-selling opportunities but also obliges oversight of regulatory compliance across varied domains.

Regulatory Landscape: License Extensions and Compliance Challenges

A central strategic development was Turkcell securing GSM license extensions through April 30, 2029 along with spectrum renewals for legacy technologies (2G–4.5G) extending up to December 31, 2042 [S1][S23][S27]. These concessions include annual gross sales fees amounting to roughly five percent of mobile revenues, imposing ongoing operational costs.

The relationship with Turkey’s Information and Communication Technologies Authority (ICTA), coordinated via a License Coordination Committee, formalizes dispute resolution mechanisms primarily through arbitration or the Council of State depending on license type [S1]. Compliance mandates stipulate sourcing minimums for R&D investments domestically (≥40%) and engagement of SMEs (≥10%), enhancing local supplier development but introducing operational constraints.

Operational suspensions tied to national security are permitted under license terms without compensation beyond retaining revenue collections during suspensions—a unique risk dimension reflecting Turkey’s geo-political context [S1]. Overall these regulatory factors constitute structural industry barriers reinforcing Turkcell’s competitive moat albeit requiring vigilant compliance.

Foreign Currency Exposure and Hedging Strategies Amid Volatile Markets

Turkcell contends with complex FX exposures given USD-, EUR-, and CNY-denominated borrowings contrasted against predominantly TRY functional revenues [S1]. To mitigate translation and transaction risks affecting consolidated statements, Turkcell maintains "natural hedges" by holding cash reserves in foreign currencies aligned with liabilities.

Advanced derivative instruments including non-deliverable forwards (NDFs), currency swaps, and interest rate swaps underpin dynamic hedging practices despite liquidity diminution and rising hedging premiums amid global volatility [S1][S22]. Emerging market inflation accounting transitions also impact statutory accounts shaping capital resource planning.

Continual assessment of hedging capacity remains essential as derivative market interventions by Turkish regulators could materially escalate hedging costs disrupting risk management efficacy.

Capital Structure and Investment in 5G Network Infrastructure

March-April of calendar year 2026 saw Turkcell secure a USD $1 billion Murabaha syndicated loan compliant with Islamic finance principles featuring a seven-year tenor including a two-year principal grace period at an all-in cost approximating SOFR +2.14% annually [N1][S2][S3][S4][S6][S7][S8].

Complementary bond issuances—in particular USD conventional/sustainable tranches maturing in early-2030s at fixed coupons near mid-seven percent territory—reflect prevailing local interest rate environments [S14][S15][S16].

Capital expenditures have intensified toward next-generation network rollouts—especially for expanded fiber broadband footprint, data centers enhancement, renewable energy projects alongside core infrastructure maintenance—with operating capex approximated at about one quarter of revenues projected for fiscal year ending December 31, 2026 [S5][S20].

Efficient leverage management is demonstrated by net debt-to-Adjusted EBITDA ratios remaining conservative near or below the stated threshold of around one-tenth (0.14x end-2025) despite elevated capex commitments [S5][S6][S12][F1].

Robust Capital Allocation: Dividends, Buybacks, and Debt Management

The Company sustains shareholder returns via dividends aligned with its policy targeting payout ratios above fifty percent of distributable profits annually [S9][S21]. Dividend disbursements rose from TRY ~6.3 billion for FY23 payouts to planned distributions approximating TRY ~8.8 billion proposed for FY25 representing significant growth reflecting net income expansion [F1][S10][S11]. Share repurchase activity continues at modest scale enhancing shareholder value though less pronounced than cash dividends.

Cash flow from operations consistently funds dividend distributions alongside significant reinvestment needs; however free cash flow coverage is pressured given elevated capital expenditure requirements typical for telecom carriers undergoing technology transitions [F1][S9]. Foreign exchange volatility factors into debt servicing capacity but balanced maturity profiles mitigate refinancing risks well into late decade [F1][S6].

ROE approximates an attractive level near double digits (~10.3% using latest net income over equity) revealing efficient capital deployment within cyclical headwinds [F1].

Outlook and Key Milestones to Monitor for Sustained Growth

Absent explicit forward guidance on financial targets within disclosed documents, key indicators warranting close monitoring include subscriber base evolution—particularly retention improvements or accelerated postpaid penetration—alongside progressive profitability margins amidst rising network OPEX tied to the new technological infrastructure investments [N1][S1].

Licensing developments beyond the secured spectrum term till end-2042 represent potential inflection points impacting spectrum costs or usage rights renewal conditions that could materially affect long-term competitiveness.

Additional competitive pressures may stem from OTT entrants or regional rivals seeking disruptive pricing models necessitating agile commercial responses preserving Turkcell’s market leadership position.

Valye Analysis: Competitive Moat from Integrated Infrastructure and Diversified Revenue Streams

Turkcell commands entrenched advantages anchored in substantial network effects yielded from its dominant market share within Turkey combined with integrated Techfin capabilities expanding beyond classical telecom offerings . The firm’s investment mandates enforcing localized suppliers comprising significant R&D proportions fortify innovation pipelines domestically while nurturing SME ecosystems—a distinctive facet reducing dependency risks on global vendors under geopolitical uncertainty.

The synergy between telecom service reliability fortified by extensive infrastructure assets plus burgeoning digital financial services creates multifaceted barriers difficult for new entrants prioritizing scale or integration economies to surmount quickly.

Nonetheless steady vigilance around regulatory adaptations remains essential given ICTA’s authoritative role influencing operational contingencies including suspension rights under national security considerations—a structural risk component intrinsic to operating in Turkey’s strategically sensitive environment.

This analysis is based exclusively on publicly available information compiled from official company filings, news releases, and documented regulatory disclosures as of April 17, 2026; it avoids conjecture or speculative forecasts beyond stated sources. It is intended solely for informational purposes without investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments