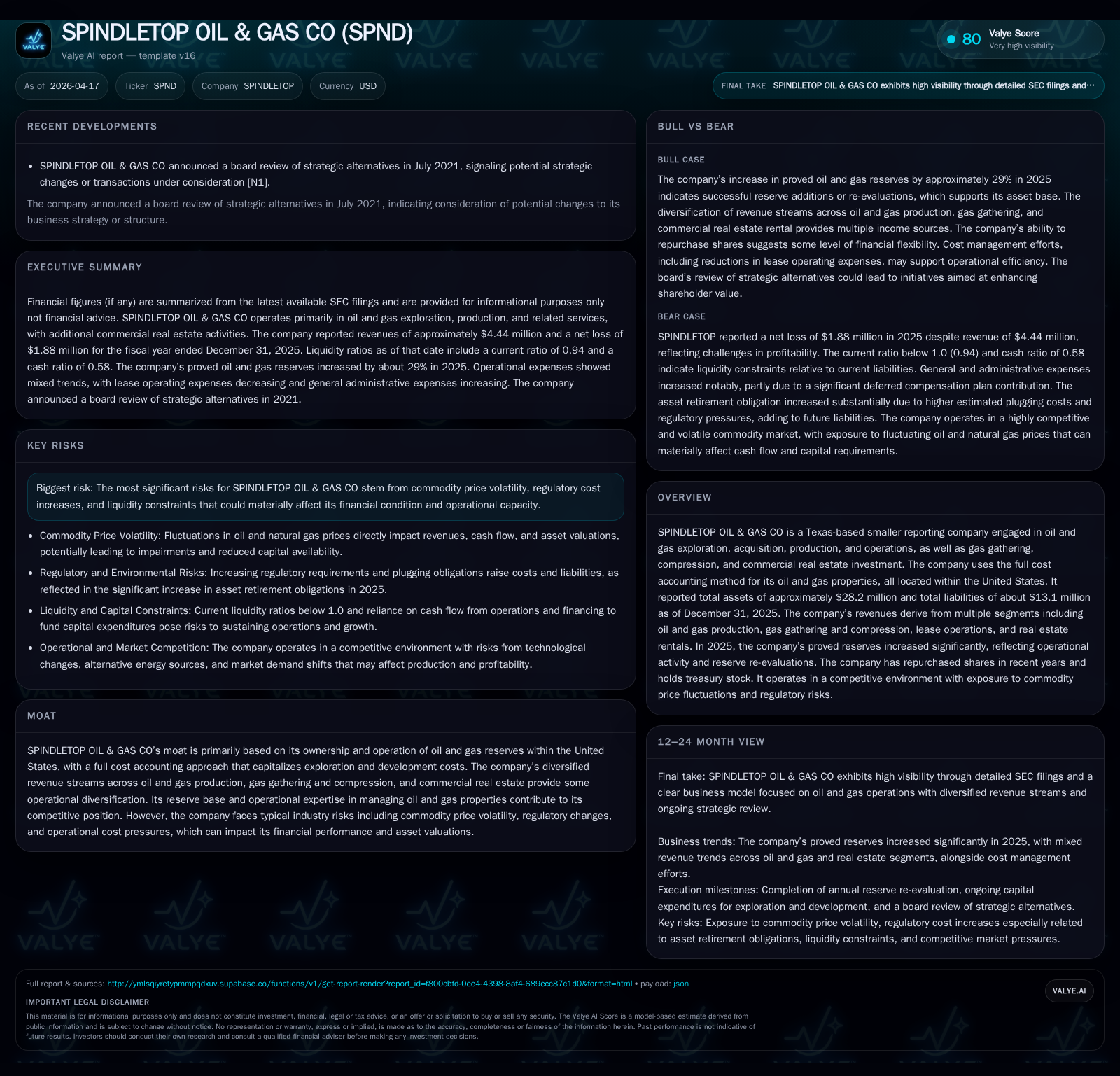

SPINDLETOP Oil & Gas: Balancing Asset Growth and Operational Challenges in 2025

SPINDLETOP Oil & Gas expanded its proved reserves in 2025 but grappled with deepening losses and liquidity strains amid volatile market conditions.

In 2025, SPINDLETOP Oil & Gas recorded a modest revenue increase alongside a significant rise in proved reserves, signaling active operational engagement. However, the company faced sharply deteriorating operating income and net losses, compounded by negative operating cash flow and a current ratio below one, underscoring liquidity pressures. While the firm undertook opportunistic share repurchases, it maintained no dividend policy amid constrained profitability and capital market challenges. Going forward, SPINDLETOP's financial health depends on managing its working capital requirements and navigating sector headwinds including commodity price fluctuations and regulatory risks.

Revenue and Reserve Trends: Reviewing Recent Performance

In fiscal year 2025, SPINDLETOP Oil & Gas reversed a multi-year revenue decline with a modest top-line increase to approximately $4.44 million, up 4.4% from $4.26 million in 2024 [F1]. This growth was driven by sustained production operations combined with expansion in proved reserves. The company operates under the full cost accounting method for its wholly U.S.-based oil and gas properties, which capitalizes exploration and development costs in a conventional manner for smaller producers [S10]. The rising reserve base reported at the end of 2025 reflects both reserve additions through operational activity such as new drilling efforts—including participation in non-operated wells in Oklahoma—and technical revisions tied to price sensitivity adjustments consistent with industry practices [S23][N/A].

SPINDLETOP also maintains diversified income streams spanning oil and gas production, gas gathering and compression services, lease operations, and commercial real estate rentals—offering some operational diversification albeit within a concentrated geographic footprint primarily focused on Texas [S10]. However, these segments contribute relatively small revenue slices outside core hydrocarbons.

Operating Losses Deepen Despite Growing Asset Base

Notwithstanding an expanding asset profile evidenced by increasing proved reserves (albeit details on exact reserve volumes remain generalized), SPINDLETOP deepened operating losses substantially in 2025. The operating income deteriorated by approximately 85%, from a loss of $1.78 million in 2024 to a more severe loss of $3.28 million in 2025 [F1]. This deterioration aligns with common sector dynamics where margin pressure emerges due to depressed commodity prices juxtaposed against inflationary trends in oilfield services costs—including labor, materials, and logistics—that weigh heavily on smaller operators without scale economies [S1][S23].

Net losses widened even more dramatically reaching $1.88 million for the year—a loss magnitude unlikely mitigated by any offsetting income sources—with the implied return on equity slipping into negative territory around -13% based on fiscal year-end equity balances near $14.3 million [F1][S13]. The company's margin compression is notably driven by increasing amortization rates applied on the full cost pool—a direct consequence of reserve reevaluation that raises depletion expense—and an uptick in general & administrative expenses alongside fixed operational costs pressured by regulatory compliance costs [S23].

Cash Flow Dynamics, Capex, and Working Capital Pressures

SPINDLETOP's ability to convert operations into positive cash flow is currently impaired; the company reported negative operating cash flow of roughly -$135 thousand for 2025 following positive inflows in prior years ($224k in 2024) despite continuing conservative capital spending capped at approximately $83 thousand per annum [F1]. This gap underscores constraints in generating sufficient internal funding for ongoing exploration and development programs.

The liquidity profile reflects underlying working capital tensions: with current assets of around $6.34 million barely covering current liabilities of approximately $6.74 million as of December 31, 2025—yielding a current ratio near 0.94 which flags short-term funding tightness [F1][S13]. Accounts payable notably track rises consistent with deferred payments for oilfield services as well as accrued liabilities including production proceeds obligations—a typical feature in upstream cash flow cycles but challenging when continuous drilling activities require upfront investment without prompt cash conversion.

The company is actively assessing funding alternatives including third-party joint ventures or selective divestitures of certain properties likely aimed at bolstering operating capital availability or reducing balance sheet leverage—steps aligned with industry best practices among smaller public independents experiencing capital market friction [S3][S5]. These measures are pivotal given systemic volatility impacting credit accessibility.

Capital Structure and Liquidity: Navigating Funding Constraints

A material challenge facing SPINDLETOP lies in external financing markets dynamics further complicated by its downgrade from OTC Pink Current market status to OTC Pink Limited market effective July 2025—a shift that signals reduced disclosure completeness and heightens trading caution among investors [S6][S14]. This downgrade imposes practical barriers hampering both equity liquidity and debt availability since institutional lenders often factor exchange visibility into credit risk assessments.

Investor sentiment toward oil and gas extraction companies has also been dampened by growing ESG activism targeting fossil fuel investments; pension funds and wealth managers imposing divestment policies add layers of complexity restricting new capital inflow channels for firms like SPINDLETOP reliant on external funding cycles [S3][S5]. Such changes worsen cost-of-capital parameters.

The company’s balance sheet shows total liabilities edging up (from about $11 million in 2024 to over $13 million at end-2025), mainly driven by increased asset retirement obligations (ARO) reflecting recalculated future plugging costs—a key regulatory liability recognized under federal accounting guidance—which strain long-term liquidity planning amidst uncertain commodity outlooks [S13][S14].

Risks Spotlight: Commodity Volatility and Regulatory Headwinds

SPINDLETOP acknowledges principal operational risks centering on price fluctuations inherent to hydrocarbons affecting production economics directly: sustained low pricing leads to potential curtailments or shut-ins which cascade into reserve impairments necessitating write-downs under full cost accounting—events that materially depress earnings quality [S14][S6]. Additionally, evolving environmental regulations increase compliance burden including rising decommissioning costs encompassed within ARO calculations escalating ongoing liabilities.

The firm faces ongoing litigation exposure with lawsuits filed against subsidiaries involving pollution claims though recent dismissals have alleviated immediate contingent risk; nevertheless continuous monitoring remains obligatory due to potential financial impacts if outcomes diverge unfavorably [S14][S25].

Strategic Capital Allocation: Share Buybacks Versus Dividends

Though SPINDLETOP pays no dividends—consistent with a resource-sector focus on reinvestment amid profitability challenges—it has opportunistically repurchased shares from unaffiliated non-controlling shareholders without a formal repurchase program during the past three years totaling over 150 thousand shares including transactions as recent as June 2025 at an average price near $2.48 per share; these shares are held as treasury stock reducing outstanding float but signifying limited but disciplined use of excess liquidity where available rather than broad-based shareholder returns [S4][F1][S19].

Given negative net returns on equity around -13%, such cautious buyback activity reflects an emphasis on capital preservation rather than aggressive value extraction while navigating structural earnings headwinds.

Outlook Highlights: Potential Catalysts and Financial Priorities

Management offers limited formal guidance but signals focus remains on securing sufficient funding through potential joint ventures or asset sales crucial for sustaining planned exploration drilling activities notably ongoing recompletion efforts targeting formations like Mississippian Lime via non-operated fractional interests—activity that supports reserve growth even amid funding uncertainty [S3][N/A][S19].[N/A]

Market conditions remain precarious; tracking commodity prices will be essential along with monitoring progress on litigation matters potentially materializing from ongoing claims in Louisiana which could influence future contingency provisions or impairments.

Careful balance between preserving operational momentum while managing leverage levels will drive financial priorities going forward.

Key Metrics Summary and Historical Financial Table

Historical performance (annual)

| FY | Rev ($mm) | CFO ($) | OpInc ($mm) | Capex ($) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 4 | -135000 | -3 | +4.4% | |

| 2024 | 4 | 224000 | -2 | 83000 | -16.7% |

| 2023 | 5 | 853000 | -1 | 83000 | -38.9% |

| 2022 | 8 | 1600000 | 0 | 82000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) |

|---|---|

| 2025 | |

| 2024 | 141000 |

| 2023 | 770000 |

| 2022 | 1518000 |

Source: SEC companyfacts cache [F1]. Revenue figures are millions USD; Operating/Net Income millions USD; CFO/Capex thousands USD; YoY % comparisons based only on adjacent years data as available.

This summary illustrates a trajectory of shrinking revenues post-peak years intertwined with mounting losses amplifying operating stress despite modest capex constancy aimed at preserving asset base.

This analysis synthesizes SPINDLETOP Oil & Gas’s publicly available financial disclosures up to its FY2025 annual report and related quarterly filings without extrapolations or speculative forward looking views beyond company-provided commentary or factual references herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments