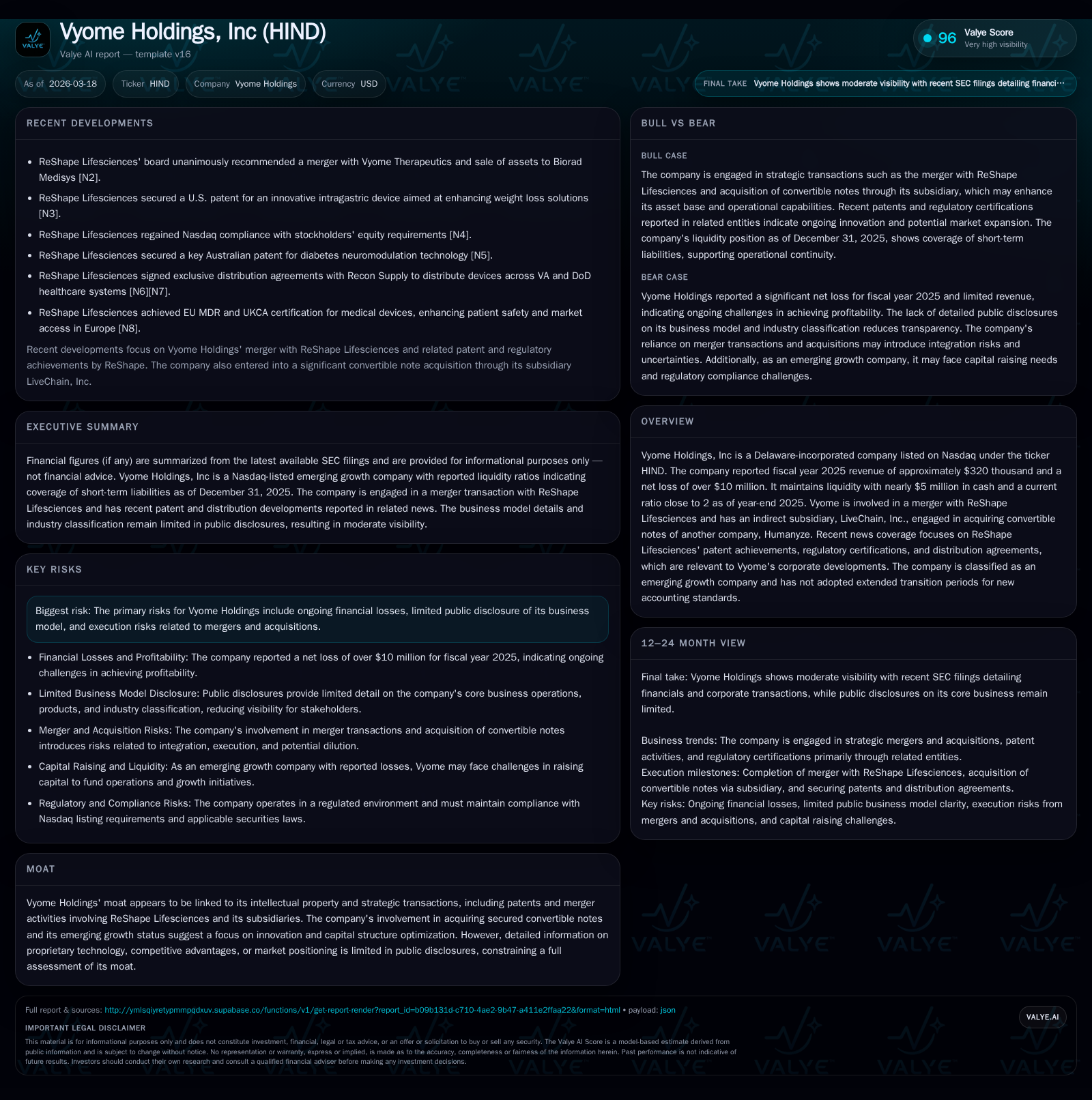

Vyome Holdings' Strategic Merger and Clinical Pipeline Challenges in 2025

Vyome Holdings confronts persistent financial losses while advancing its merger with ReShape Lifesciences and progressing late-stage clinical assets.

Vyome Holdings, Inc. reported revenue of approximately $320 thousand in FY2025 against sustained net losses exceeding $10 million. The strategic merger with ReShape Lifesciences in mid-2025 introduces potential synergies but also operational complexities amid ongoing clinical development delays. Core clinical assets VT-1953 and VB-1953 approach pivotal regulatory milestones with orphan drug designations enhancing exclusivity prospects. Liquidity remains constrained at roughly $5 million cash with a near 2x current ratio, necessitating prudent capital management including convertible note acquisitions via subsidiary LiveChain. Execution risks persist due to the company's limited commercialization history and clinical trial uncertainties, setting the stage for critical FDA interactions in H1 2026.

Historical Financial Trends Reflecting Revenue Collapse and Persistent Losses

Vyome Holdings has experienced a pronounced deterioration in revenue coupled with persistent heavy operating losses over recent years. After peaking at approximately $3.7 million in revenue during FY2017, revenues have contracted sharply to a mere $319,714 by FY2025—a precipitous fall of roughly 84.3% year-over-year from FY2024 [F1]. Concurrently, operating income remained deeply negative at -$10.45 million for FY2025, a 35% improvement from the prior year's loss but still indicative of severe operational challenges.

Net losses follow a similar pattern: from a loss exceeding $46 million in FY2022, the deficit narrowed significantly but remained substantial at an over $10.2 million net loss in FY2025 [F1]. Operating cash flows also remain negative, albeit improving from -$21.9 million in FY2022 to -$3.75 million by FY2025. Capital expenditures are minimal and declining relative to previous years, suggesting a low fixed asset intensity typical of clinical-stage pharmaceutical companies reliant on R&D rather than manufacturing.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -10 | -4 | -10 | -43.9% |

| 2024 | -7 | -4 | -8 | +37.4% |

| 2023 | -11 | -17 | -15 | +75.4% |

| 2022 | -46 | -22 | -46 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | |

| 2024 | 2818.2 |

| 2023 | -170.9 |

| 2022 | -1262.3 |

Source: SEC companyfacts cache [F1].

These figures underscore the difficult trajectory for Vyome's commercial viability absent successful clinical progress or transformative corporate transactions.

Merger with ReShape Lifesciences: A Turning Point or Additional Complexity?

On August 15, 2025, Vyome completed its merger with ReShape Lifesciences Inc., marking a pivotal corporate transition [S1]. The merger rebranded the combined entity as Vyome Holdings and resulted in Vyome Therapeutics continuing as a subsidiary under this structure. Intended synergies include leveraging innovation along the US-India corridor and combining intellectual property portfolios.

However, the merger entailed substantial direct and indirect costs that have materially impacted FY2025 results [S1]. While management anticipates long-term benefits from scale and clinical pipeline consolidation, integration risks remain notable—ranging from operational disruptions to investor hesitancy if anticipated efficiencies fail to materialize or are delayed.

Moreover, shareholder approvals and strategic realignments add layers of complexity typical for such transformative transactions in specialty pharma where product pipelines dictate future valuations rather than historic revenues.

Clinical Development Focus: VT-1953 Topical Gel and VB-1953 Acne Program’s Milestones and Regulatory Outlook

Vyome’s primary growth drivers reside in its late-stage clinical candidates aimed at immune-inflammatory and rare diseases of unmet need [S1]. Its lead asset VT-1953 is a topical gel being developed for malignant fungating wounds (MFW), which carries potential orphan drug designation—significant for regulatory exclusivity advantages.

Positive Phase II data emerged from an investigator-initiated trial supporting VT-1953’s efficacy profile [S1]. The company plans FDA discussions on pivotal Phase III trial design targeted for H1 2026—critical milestones that could shape regulatory pathways and bolster valuation if affirmative.

Alongside VT-1953, VB-1953 targets moderate to severe acne and is phase 3-ready following completion of its Phase II trial [S1]. The pipeline also includes VT-1908 — an ophthalmic drops program targeting steroid-sparing anterior uveitis — still at pre-Investigational New Drug application stage but potentially qualifying as an orphan drug candidate as well.

Securing orphan status typically provides seven years market exclusivity post-approval in the U.S., alongside expedited review paths. Such designations enhance commercial viability but hinge entirely on successful trial execution and FDA engagement.

Capital Structure Evolutions and Liquidity Management Amid Ongoing Operating Cash Burn

As of December 31, 2025 year-end close-out [F1], Vyome reported cash & cash equivalents of approximately $4.98 million paired with current assets totaling around $5.44 million against current liabilities near $2.74 million—yielding a current ratio close to an enviable 1.99x liquidity buffer.

Operating cash flow remains negative at about -$3.75 million for FY2025 albeit improved versus prior years [F1]. This ongoing cash burn highlights funding urgency common among clinical-stage firms still pre-commercialization.

To bolster liquidity beyond organic means and equity raises tied to merger event costs [S1], Vyome’s indirect subsidiary LiveChain has engaged in acquiring senior secured convertible notes issued by Humanyze—an entity specializing in advanced workplace analytics solutions [S6][S8][S23].

This transaction involved issuing substantial common stock representing significant minority ownership (~25%) of LiveChain's fully diluted shares to Remus Capital Series B II LP [S6][S9][S13]. Additionally, up to another ~10% shares reserved for employee compensation within LiveChain emphasize equity dilution as a tradeoff against securing strategic asset control within an evolving capital structure. Such deal structures reflect niche biotech finance strategies balancing cash conservation against obtaining real assets or intellectual property embedded within convertible debt instruments.

Risks Surrounding Limited Operating History, Regulatory Approval Uncertainties, and Execution Challenges

Vyome explicitly acknowledges material risk factors reflective of its developmental stage:

- The company has no history bringing products successfully through commercialization and faces high odds associated with advancing VT-1953 and VT-1908 through the regulatory process without failure or delay [S1][S4].

- Patient enrollment delays remain a feasible risk given narrow indications involved with orphan drug pathways resulting in extended timelines or elevated costs [S1].

- Prolonged operating losses necessitate repeated capital raises introducing dilution risk or unfavorable financing terms that could further pressure shareholder value [S1][S4].

- Integration risks post-merger include realizing projected synergies amid possible operational disruptions or conflicting priorities between combined entities’ leadership teams [S1].

- Intellectual property infringement exposure exists although not currently litigated; this represents standard industry risk especially within specialized dermatological therapeutics domains.

Collectively these risk vectors demand cautious monitoring by stakeholders given the speculative nature inherent in specialty pharma clinical development contexts.

What to Watch: Upcoming FDA Discussions on VT-1953 Pivotal Trial Design & Phase III Readiness for VB-1953 Acne Treatment Program

Investors and analysts should closely follow scheduled FDA engagements planned by Vyome for first half of calendar year 2026 that focus on pivotal Phase III trial designs particularly surrounding VT-1953's malignant fungating wounds indication [S1]. These meetings will be barometers determining whether existing Phase II datasets suffice or whether additional studies will be mandated—a decision point that can redefine timeframes to market or partner/licensing negotiations.

Simultaneously advancing VB-1953 into late-stage development steps offers dual catalysts supporting pipeline breadth that could mitigate risks associated with single asset dependency frequently scrutinized by biotech investors.

Overall these milestones represent critical pressure points where technical progress intersects distinctly with financing needs—and shape near-term narrative shifts away from persistent losses toward eventual proof-of-concept validation essential for commercialization pathways.

This analysis incorporates data strictly derived from Vyome Holdings' SEC filings through March 18th, 2026 ([F1], ) synthesizing reported financials alongside corporate developments without introducing speculative forecasts or investment recommendations. Given the early-stage developmental status combined with complex financial restructuring activities including merger integration and convertible note transactions via subsidiaries like LiveChain Inc., Vyome Holdings presents fundamental operational challenges offset moderately by promising orphan drug pipeline candidates entering critical regulatory phases expected over coming quarters.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments