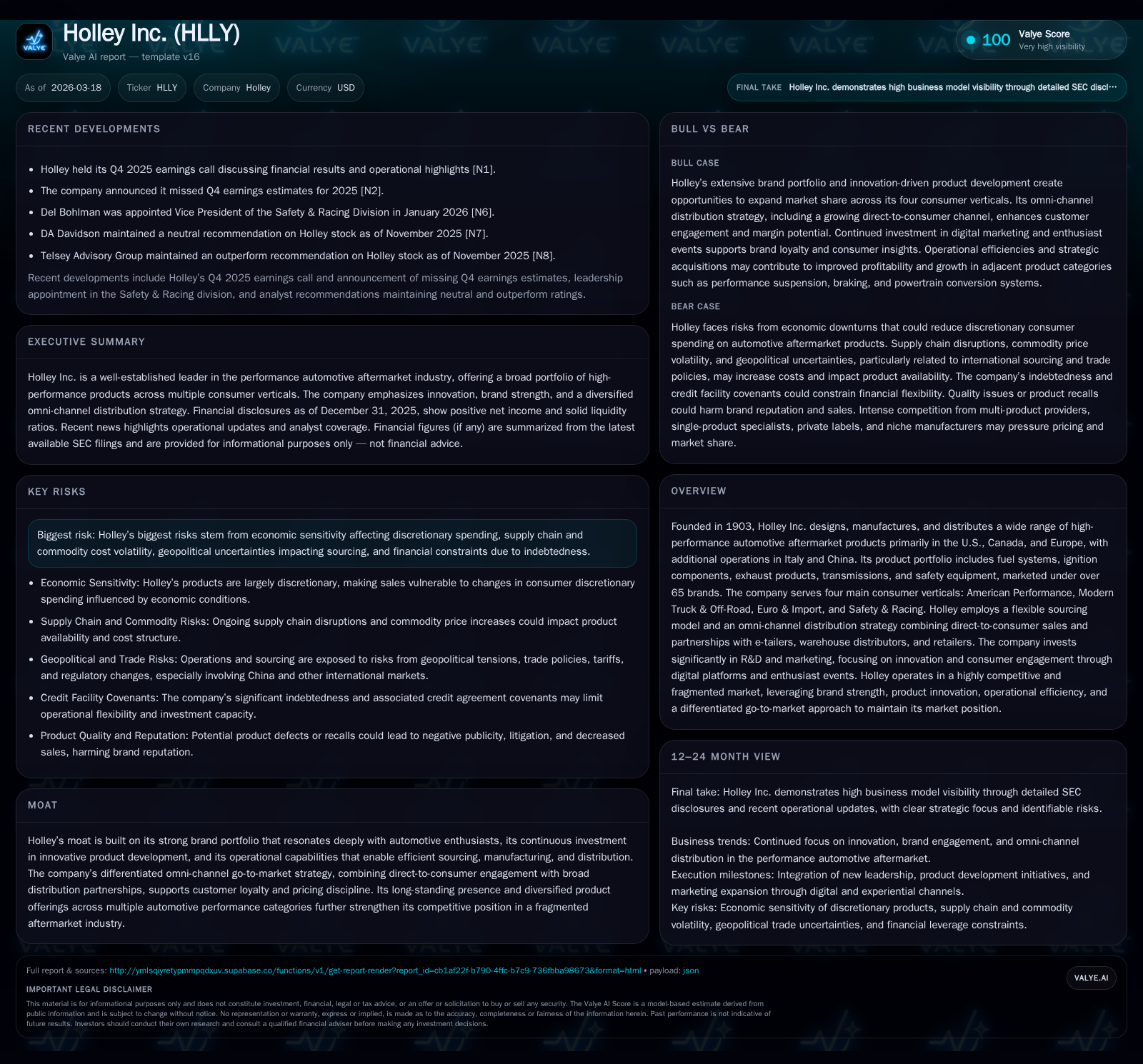

Holley Inc. Rebounds in 2025 with Innovation and Brand Strength Amid Macro Challenges

Holley Inc. leverages its diversified brand portfolio and go-to-market strategy to recover profitability despite economic and supply headwinds.

After a difficult 2024 marked by losses, Holley Inc. experienced a significant rebound in operating income and net earnings in 2025, driven by operational improvements and product innovation. The company’s broad portfolio of over 65 automotive aftermarket brands, combined with an omni-channel distribution approach, supports resilience in a fragmented and competitive market. However, ongoing risks remain from macroeconomic volatility, supply chain pressures, tariffs, and financial leverage constraints. Future growth hinges on successful new product launches, market share expansion within established verticals, and navigating external uncertainties.

Historical Performance Trends

Holley Inc., an established leader since 1903 in the high-performance automotive aftermarket sector, emerged from a challenging fiscal environment with notable financial gains in 2025. After posting a net loss of $23.2 million in 2024 accompanied by compressed operating income of only $14.7 million, Holley recalibrated operations resulting in sizable improvement: operating income soared to approximately $82.5 million — a stunning near fivefold increase — while net income swung positively to $19.2 million for the year ended December 31, 2025 [F1].

Operating cash flow showed remarkable consistency around $46 million annually despite this volatility, reflecting effective working capital management during fluctuating sales and elevated marketing expenses tied to brand-building efforts and digital transformation initiatives [F1][S14]. Capital expenditures rose sharply to about $12.3 million (up over 80%), signaling reinvestment aimed at sustaining innovation pipelines and production efficiencies necessary to support aggressive growth targets [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 19 | 46 | 82 | 12 | +182.5% |

| 2024 | -23 | 47 | 15 | 7 | -221.1% |

| 2023 | 19 | 88 | 94 | 6 | -74.0% |

| 2022 | 74 | 12 | 51 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 34 | 4.3 |

| 2024 | 40 | -5.5 |

| 2023 | 82 | 4.3 |

| 2022 | -1 | 17.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures were not explicitly disclosed within the available filings.

Business Model and Industry Positioning

Holley is widely recognized for its extensive lineup of over 65 brands distributed across more than thirty-five product categories spanning fuel systems, ignition components, exhaust products, transmission systems, safety gear, and performance electronics [S12][S13]. The company's strategic focus targets four core consumer verticals: American Performance enthusiasts favoring traditional muscle cars; Modern Truck & Off-Road consumers; Euro & Import vehicle owners; and Safety & Racing participants seeking specialized gear [S12][S14].

This segmentation allows Holley to tailor both product development and marketing programs distinctly for each group. Brand names such as Holley EFI (17% of sales), Holley legacy brand (11%), MSD ignition systems, Flowmaster exhausts, Simpson racing equipment, EDGE tuners, Cataclean additives and Accel spark plugs underpin the company's commanding presence within highly fragmented aftermarket niches [S12]. Concentration among the top five brands accounted for nearly half of total revenues within the latest reporting period.

Incorporating an omni-channel distribution approach amplifies reach: direct-to-consumer sales through Holley.com enable full assortment visibility plus exclusive content linked to enthusiast culture via Motor Life internal publication; meanwhile approximately half of total revenues flow through established warehouse distributors and e-tailers who serve diverse retailer clients including jobbers/installers [S13][S14]. This blended go-to-market system secures pricing discipline through minimum advertised price policies while fostering customer loyalty via brand authenticity initiatives.

Customer events such as LS Fest East/West and Ford Fest have grown attendance tenfold over the decade—reaching about 110,000 attendees during calendar year 2025—showcasing community-building efforts beyond transactional relationships [S14].

Growth Prospects & Strategy Execution

Holley's management has outlined expansion plans emphasizing both organic innovation and bolt-on acquisitions especially focused on adjacent product segments such as performance suspension systems, braking solutions, powertrain conversions, as well as broader automotive safety offerings that are powertrain agnostic—broadening relevance amidst evolving engine technologies including electrification trends creeping into enthusiast circles [S7][S12].

Innovation is central: heavy investment into R&D enables Holley EFI products showcasing electronic fuel injection advancements complemented by software-enabled tuning tools meeting modern vehicle demands [S12]. Digital marketing spend reached roughly $14.7 million (~2.3% of projected annual revenues), underscoring resource commitment towards digital advertising channels alongside traditional enthusiast outreach [S14].

Risks persist due to external factors impacting discretionary spending patterns critical to aftermarket parts sales: inflationary pressures combined with volatile global macroeconomic conditions could suppress demand or shift mix towards lower-margin economy products necessitating price competition that challenges margin sustainability [S1][S24]. Tariffs primarily imposed on Chinese imports introduce cost volatility which may not be fully recoverable—potentially squeezing earnings if commodity prices spike simultaneously or supply chain constraints trigger stock-outs or delays [S1][S18].

Geopolitical tensions notably between US-China relations adjoining Taiwan add uncertainty particularly for components sourced overseas impacting inventory lead times or cost bases; mitigation strategies include maintaining multiple sourcing options though no assurance exists against all supply shocks [S8][S9].

Financial Position & Capital Allocation Discipline

Total debt outstanding stood at $529.4 million as of December 31, 2025 under a credit facility structured with restrictive covenants including leverage targets requiring net leverage ratio below defined thresholds; failure risks triggering acceleration clauses impacting liquidity if breached during periods of operational stress [S4][S6][S15]. Interest expense sensitivity to variable rates adds potential cost risk if broader monetary tightening continues.

Despite indebtedness constraints Holley maintains solid liquidity positions—with cash plus equivalents totaling approximately $37 million complemented by current assets surpassing liabilities nearly threefold yielding a current ratio of about 2.75 supporting ample near-term working capital needs [F1][S4]. Operating cash flows stabilized at around $46 million annually though free cash flow generation was tempered by capex upticks yielding an approximate FCF figure near $33.9 million last year—indicating prudent reinvestment balanced with capital stewardship [F1].

No dividends or share buybacks were noted explicitly in disclosures implying retention of cash flows for business development or debt reduction priorities currently [F1]. Going forward it will be critical for Holley to manage covenant compliance tightly while balancing investment requirements particularly given its high fixed cost operational footprint inclusive of manufacturing automation initiatives.

Key Challenges & Risks Overview

Beyond cyclical vulnerability due to discretionary nature of recreational automotive parts spending there are several structural risks:

- Legal/regulatory compliance spanning environmental laws (notably related to air emissions under frameworks like California’s Air Resources Board), data privacy regimes cross-jurisdictionally including GDPR sensitivities impacting e-commerce channels incur ongoing costs/fines risk exposures if breached accidentally or otherwise [S10][S19][S26].

- Quality assurance challenges whereby any recalls or warranty claims could damage reputation among enthusiasts who value reliability potentially depressing demand after negative publicity episodes—Holley's rigorous testing regimes help but do not eliminate risks altogether [S9][S17].

- Continued competition from multi-product conglomerates leveraging scale efficiencies; single-product specialists focusing on quality/price niches; e-tailer private labels serving value-oriented buyers; and niche custom shops targeting localized segments compels persistent innovation/differentiation efforts alongside channel management vigilance for gray market erosion prevention commonly encountered in aftermarket industries [S12][S29].

- Market disruptions stemming from natural disasters or geopolitical instability affecting supply chains predominantly overseas suppliers creating inventory fulfillment risks also underpinned by cost pushes related to freight rate fluctuations or labor disputes affecting ports/manufacturing hubs globally especially China operations contribute risk layers demanding contingency planning rigor [S18][S21][S23].

Future Outlook Indicators (Analysis)

Though explicit revenue guidance was not published recently by company filings or earnings calls available up to early March '26 there are clear signals to monitor:

- Success metrics around new product releases particularly in electronically enhanced powertrain controllers or suspension components.

- Gains in DTC channel online traffic growth reflecting deeper consumer engagement tied directly to e-commerce conversions.

- Distribution partner order volumes signaling wholesale demand stability across economic cycles.

- Margins resilience amid inflationary pressures indicating efficacy of cost control measures including sourcing diversification.

- Debt covenant compliance levels tracked quarterly influencing strategic options related to further acquisitions or shareholder returns.

- Adoption rates for Holley's expanded events series attendance providing qualitative proxies for brand vitality among enthusiasts.

Investors should watch for disclosed milestones concerning any re-rating catalysts such as penetration into emerging EV performance component spaces or partnership announcements broadening global footprint beyond legacy Western hemisphere strongholds.

Conclusion

Holley Inc.'s turnaround story in FY2025 underscores enduring strength rooted in iconic brands deeply embedded within automotive enthusiast culture coupled with savvy commercial execution across multiple verticals supported by an expansive distribution network balanced by direct consumer relationships digitally enabled. Despite runaway macroeconomic uncertainty entangled with geopolitical trade frictions posing transient shocks intermixed with structural industry competitiveness pressures the firm’s sustained R&D focus alongside practical capital allocation evidences preparedness for sustained profitable growth. However management must vigilantly address liquidity covenant headwinds while maintaining product leadership within fast-evolving performance categories where emerging technologies disrupt traditional combustion engine centric paradigms alongside shifting consumer behaviors influenced by regulatory climate change imperatives. Maintaining operational excellence amidst these complex variables will define Holley's ability to convert decades-old heritage advantage into tomorrow's aftermarket success story.

Disclaimer: This analysis is based solely on publicly sourced data up to March 18, 2026 and does not represent investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments