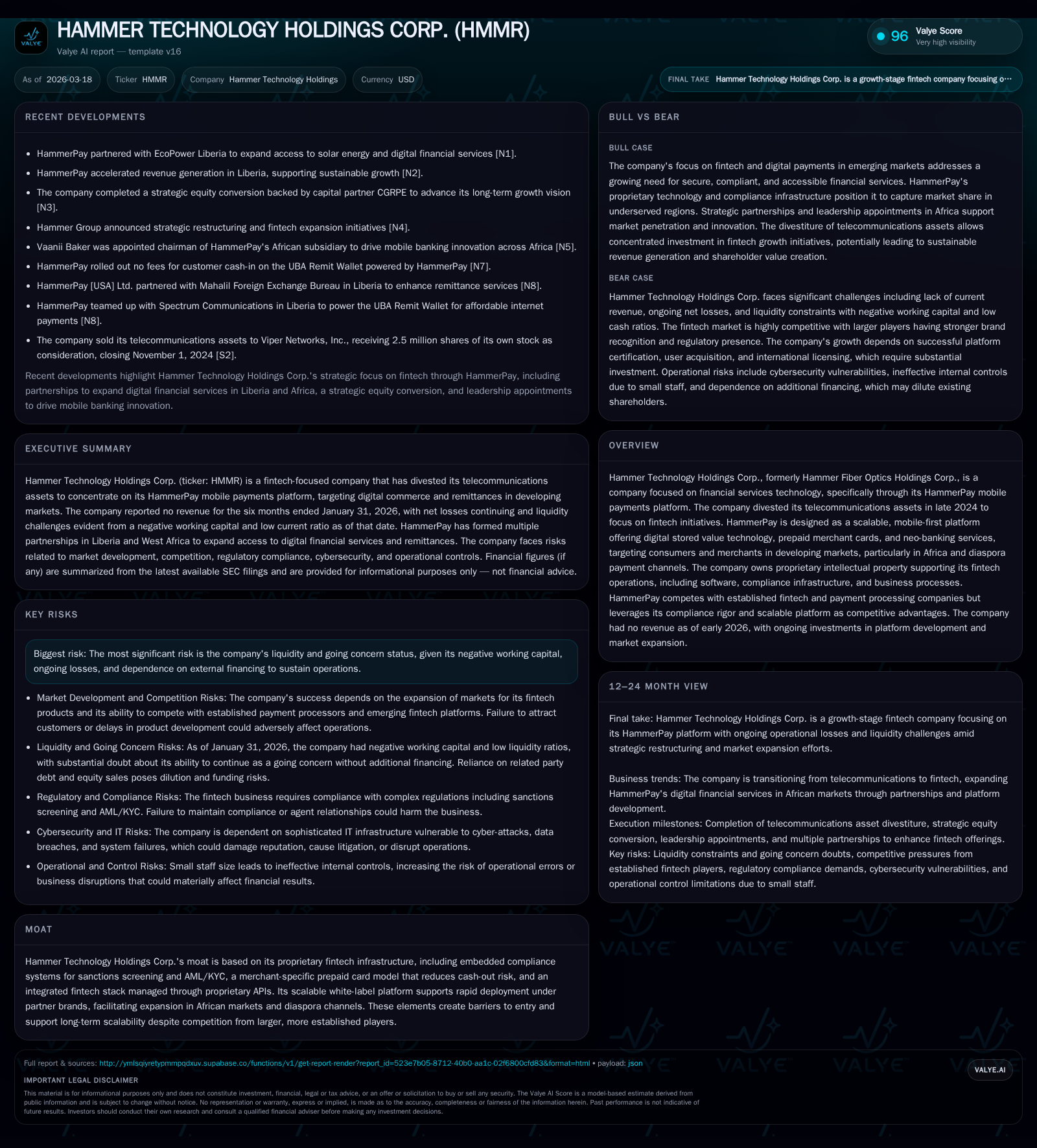

Hammer Technology Holdings Corp.: From Telecom Divestiture to Fintech Ambitions

Hammer Technology has transitioned from telecommunications to a fintech focus with its HammerPay platform, yet faces critical liquidity challenges.

Hammer Technology Holdings Corp. divested its telecommunications assets in late 2024, eliminating legacy revenues and focusing on financial technology through its HammerPay mobile payments platform. The company reported zero revenue in fiscal 2025 and recorded a significant increase in operating losses due to an intangible asset impairment. HammerPay offers compliance and scalability features tailored for emerging markets, especially Africa and diaspora payment corridors. However, ongoing negative working capital and reliance on related-party debt financing raise substantial doubt about the company's ability to continue as a going concern. Key near-term factors include the commercial launch of HammerPay, user adoption, regulatory approvals, and securing additional funding.

Historical Performance: Telecommunications Exit and Financial Impact

Hammer Technology Holdings Corp., formerly Hammer Fiber Optics Holdings Corp., completed the sale of its telecommunications assets to Viper Networks, Inc., closing on November 1, 2024 [S1][S2]. This divestiture eliminated nearly $3.28 million in revenue generated during fiscal year 2024 but refocused the company exclusively on fintech initiatives.

As a result, revenues from continuing operations declined from $3.28 million in FY2024 to zero in FY2025 due to the absence of telecom sales and the pre-launch status of HammerPay [F1][S1][S2]. Operating loss widened significantly by approximately 145%, from $1.39 million in FY2024 to $3.41 million in FY2025 [F1]. The increased loss was driven primarily by a $1.89 million impairment charge on customer contract intangible assets amid uncertainty around future earnings [S1][S16]. Selling, general and administrative expenses increased by roughly 16%, reflecting higher professional fees and IT costs linked to fintech development, while depreciation and amortization remained relatively stable at about $678k [S1].

Net income losses also expanded from approximately $1.23 million in FY2024 to nearly $2.8 million in FY2025 [F1], underscoring the operational costs associated with transitioning away from telecom towards unproven fintech offerings.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | -3 | -3 | -100.0% | -126.9% | |

| 2024 | 3 | -1 | -760238 | -1 | +0.7% | +52.2% |

| 2023 | 3 | -3 | -636706 | -1 | +25.2% | -122.7% |

| 2022 | 3 | -1 | -819609 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 384.2 | |

| 2024 | -779957 | 128.3 |

| 2023 | -649356 | -3618.2 |

| 2022 | -1024669 | -19.2 |

Source: SEC companyfacts cache [F1].

Note: Operating cash flow is from continuing operations; Capex relates mainly to software/internal development.

The divestiture also reduced liabilities associated with discontinued operations but left the company with substantial negative working capital [S6][F1]. Losses related to debt conversions further pressured results [S6].

Fintech Focus: The HammerPay Platform

Following the exit from telecommunications and rebranding effective September 3, 2025 [S1], Hammer Technology concentrates solely on fintech through its HammerPay mobile payments platform aimed at developing markets across Africa and diaspora corridors [S1][S2].

HammerPay integrates:

- Embedded AML/KYC Compliance: Automated sanctions screening aligned with OFAC, EU and UN lists embedded within onboarding workflows.

- Merchant-Specific Prepaid Cards: Prepaid cards restricted per merchant limit cash-out risks inherent in remittance corridors.

- White-Label API Integration: Enables partners to deploy branded solutions rapidly with secure issuing/acquiring and encrypted settlement.

This integrated approach provides regulatory rigor combined with operational flexibility designed to serve high-risk emerging markets effectively [S20].

Competition includes established players like Payoneer and Wise but Hammer aims to differentiate through jurisdiction-specific compliance integration and merchant-level risk controls.

Financial Condition & Liquidity

As of January 31, 2026, Hammer held $28,312 in cash against current liabilities of $725,775—yielding a current ratio near 0.04—and negative working capital of approximately $697k [F1][S3]. While this marks an improvement from July 31, 2025's deeper deficit ($858k negative working capital), liquidity remains critically constrained.

The company’s operations continue to be funded primarily through related-party convertible notes without recent third-party financing commitments [S3][S9]. For the six months ended January 31, 2026 it reported a net loss of $301k from continuing operations and used $328k cash in operating activities [F1][S9]. Management discloses substantial doubt about its ability to continue as a going concern absent additional equity or debt financing that may dilute shareholders or be available only on unfavorable terms [S3][S10][S16].

Capital Allocation & Funding Strategy

Hammer has not paid dividends or repurchased shares due to sustained losses since inception [F1][S25]. Capital expenditures have declined consistent with a shift away from physical telecommunications infrastructure toward software development supporting fintech products—the latter reflected by capex below $20k for FY2024 compared with prior years [F1].

Funding relies heavily on related-party convertible note proceeds totaling several hundred thousand dollars annually [S6][S22], highlighting dependence on internal sources until positive cash flow from operations can be realized.

Growth Outlook & Risks

Though no explicit revenue guidance or launch dates are provided due to pre-commercial status [N#], Hammer emphasizes strategic positioning:

- Targeting rapid growth in Africa’s expanding digital payments market where mobile money adoption is increasing.

- Leveraging diaspora remittance corridors underserved by traditional channels.

- Enabling scalable partner deployments via white-label APIs.

- Offering embedded sanctions screening aligning with tightening global regulations.

Risks include evolving regulatory demands requiring continual compliance system updates; potential agent network failures impacting compliance; privacy breaches threatening reputation; intense competition from banks and fintech incumbents; currency volatility; and political uncertainties common in targeted regions [S13][S18][S20].

Milestones & Investor Considerations

Key indicators for investors will be:

- Timing of commercial launch(s) enabling revenue generation beyond development phases [S2].

- User adoption metrics among merchants and consumers validating scalable deployment assumptions.

- Regulatory licenses secured across target jurisdictions crucial for cross-border services.

- Additional funding rounds or partnerships easing liquidity constraints enabling operational continuity [S3].

Monitoring these factors is essential to assess whether Hammer can translate its technology moat into sustainable commercial success supporting solvency.

This report synthesizes SEC filings up through March 18, 2026 without providing investment recommendations beyond documented data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments