TuHURA Biosciences Advances Immuno-Oncology Pipeline with IFx-2.0 Phase 3 and Kineta Deal

TuHURA’s recent quarterly filing highlights pivotal progress in its IFx-2.0 Phase 3 trial and strategic expansion via Kineta acquisition, underscoring both potential and challenges ahead.

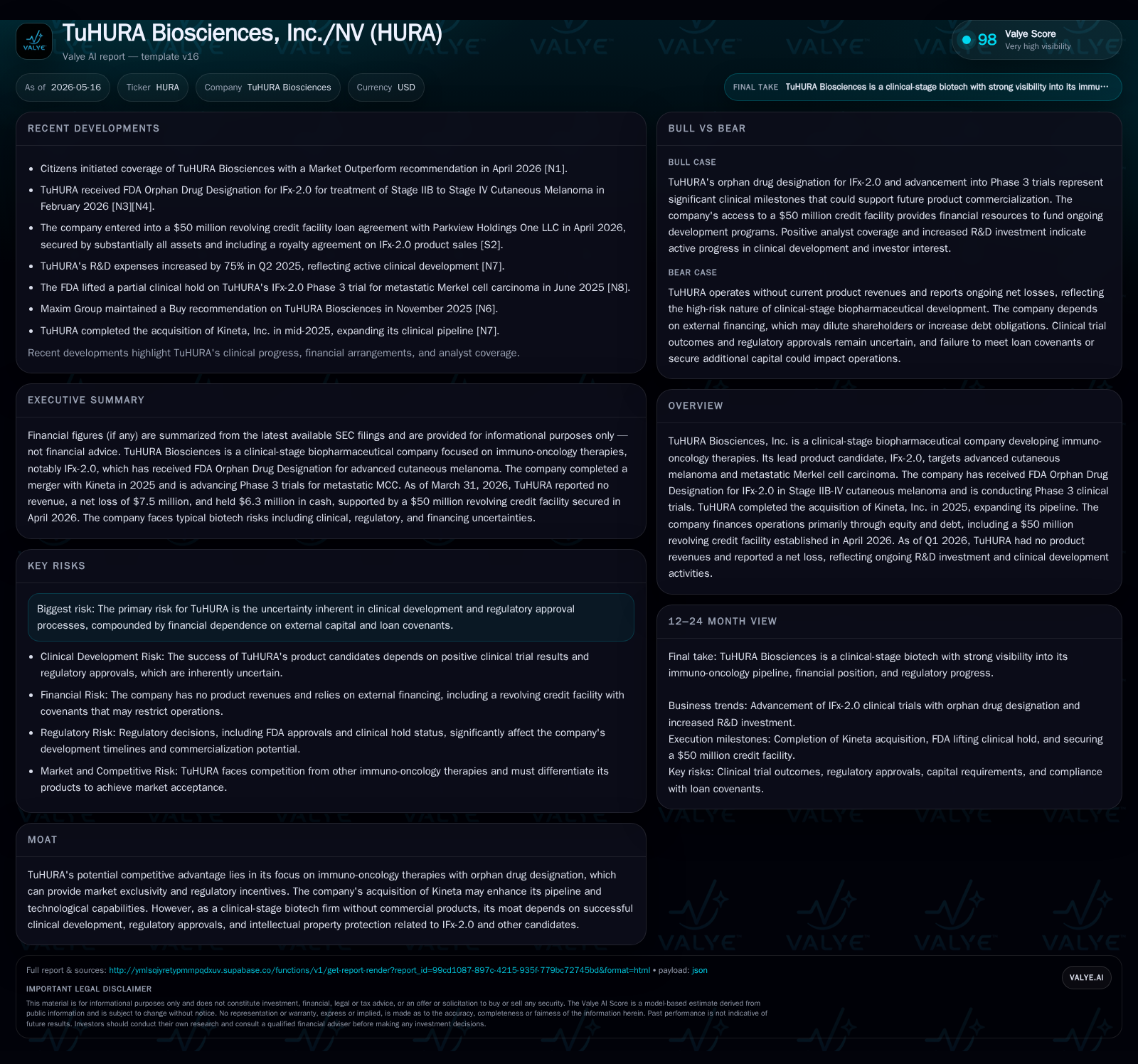

In Q1 2026, TuHURA Biosciences commenced pivotal Phase 3 clinical trials for its lead immuno-oncology candidate, IFx-2.0, targeted at advanced cutaneous melanoma and Merkel cell carcinoma. The company’s acquisition of Kineta in mid-2025 adds depth to its therapeutic pipeline and technological capabilities. Despite no product revenue and ongoing net losses, TuHURA secured a $50 million revolving credit facility in April 2026 to underwrite clinical development. The firm’s position within the orphan drug space offers regulatory and market exclusivity benefits, but growth remains contingent on clinical outcomes and capital market access.

Q1 2026 Operating Highlights: Clinical and Corporate Progress

TuHURA Biosciences' latest quarterly filing dated May 15, 2026 [S2] reveals critical operational milestones setting the near-term tone for the company’s trajectory. Most notably, TuHURA has initiated the pivotal Phase 3 clinical trial for its lead asset, IFx-2.0, designed to treat advanced cutaneous melanoma (Stages IIB-IV) and metastatic Merkel cell carcinoma — serious indications with limited effective treatment options. This candidate retains FDA Orphan Drug Designation status for Stage IIB-IV cutaneous melanoma, an important regulatory recognition that can confer seven years of marketing exclusivity in the U.S., plus valuable development incentives.

Additionally, the company’s corporate strategy is strengthened by the acquisition of Kineta in mid-2025 [S7], which augmented TuHURA’s immuno-oncology pipeline breadth beyond IFx-2.0 and enhanced its technology platforms. The impact of this deal is ongoing as integration efforts continue.

Financially, TuHURA operates without product revenue while incurring net losses reflecting significant R&D spending intrinsic to early-stage biopharma [F1]. To underwrite these expenditures amid intensive clinical development demands, TuHURA secured a $50 million revolving credit facility from Parkview Holdings One LLC in April 2026 [S15]. This facility matures in five years and is structured to allow monthly draws up to pre-agreed budget thresholds subject to lender approval. With cash and equivalents at approximately $6.3 million at quarter-end [F1], complemented by negligible debt (approximate total debt $265) [F1], this credit arrangement markedly extends TuHURA’s operational runway into early 2028.

Business Model Overview: Immuno-Oncology Focus and Product Pipeline

TuHURA's business model centers on developing immuno-oncology therapies targeting rare but severe cancers where standard treatments remain inadequate or non-existent. Its primary revenue levers are prospective medical breakthroughs rather than realized sales; it finances operations mostly via equity raises and debt facilities tied to clinical development stages.

The lead compound IFx-2.0 exemplifies this model through its orphan drug-indicated targeting of advanced-stage melanoma sub-types — an area benefiting from FDA Fast Track designations incentivizing accelerated development cycles and enhanced post-approval market protections [S1]. Orphan drug status typically allows premium pricing due to lack of competition and unmet patient demand, which can translate into robust margins upon commercialization.

The Kineta acquisition diversifies TuHURA's development portfolio beyond a single asset focus by backing next-generation immunotherapies potentially targeting other oncologic pathways or tumor profiles [S7]. Although no commercial products exist today generating top-line revenue due to phase-gated trial progressions inherent in biotech R&D timelines [F1], successful late-stage approvals would unlock traditional pharmaceutical revenue streams.

This model demonstrates acute dependence on capital markets for sustained funding until positive regulatory outcomes materialize — a dynamic common across clinical-stage biopharmaceutical companies focused on niche oncology therapeutics.

Industry Context and Competitive Positioning in Orphan Drug Markets

Within the broader immuno-oncology industry landscape, TuHURA operates in a competitive environment characterized by rapid innovation yet substantial scientific uncertainty. Success rests heavily on pioneering proprietary immune-modulating technologies capable of differentiating from existing immune checkpoint inhibitors or targeted therapies prevalent in melanoma treatment.

Orphan drug designation provides companies like TuHURA unique advantages: market exclusivity protections limiting direct competitors post-marketing authorization, potential tax credits for clinical trials, waived application fees, and expedited FDA reviews [S1]. These regulatory incentives effectively elevate entry barriers for newcomers and reinforce pricing power given limited alternative options for rare cancers.

However, enrollment challenges are pronounced because patient pools are small due to tumor rarity—requiring sophisticated site networks and collaborations with oncology specialists to ensure adequate trial participation timing. Intellectual property securing novel molecular constructs or delivery modalities remains an essential moat component to preserve competitive advantage once licensing hurdles clear.

Despite these defenses, the space remains high-risk/high-reward: pipeline candidates face considerable failure modes during development stages; hence agility in portfolio management combined with strong scientific differentiation is crucial.

Growth Drivers: Clinical Milestones and Strategic Acquisitions

The paramount driver underpinning TuHURA’s anticipated value inflection is the successful execution of the IFx-2.0 Phase 3 pivotal trial launched recently as per May 2026 disclosures [S2],[S3]. Positive interim data readouts designed into trial protocols could substantially reduce time-to-market assumptions while catalyzing patient enrollment momentum.

Concurrently, the Kineta acquisition diversifies developmental prospects through additional therapeutic candidates entering preclinical or early clinical phases — expanding future approval opportunities alongside IFx-2.0 [S7],[S8]. This deal also potentially accelerates scientific innovation via shared intellectual property assets or research platforms enhancing immune-modulatory intervention approaches.

Key performance indicators watching forward include patient recruitment rates aligned with protocol timelines; timing of planned interim efficacy/safety analyses; patent filings securing novel compositions; and any supplemental regulatory designations broadening indication scope or accelerating review speed.

Furthermore, favorable adjustments to loan structuring under the revolving credit facility may offer financial flexibility supporting protracted developmental cycles typical for immunotherapies targeting complex malignancies [S15].

Risks and Constraints: Development Uncertainties and Financial Dependence

While TuHURA enjoys orphan drug regulatory benefits nurturing potential pricing power upon eventual commercialization, it remains encumbered by classic biotech sector risks inherent to clinical-stage enterprise models.[S2],[S1]

Chief among these is outcome uncertainty. Clinical trials carry high attrition probabilities due to safety concerns or lack of efficacy signals that could indefinitely delay or derail approval timelines leading to write-downs of R&D investments.

Moreover, intellectual property challenges can arise if competitor claims encroach upon compound novelty or trial data exclusivity rights failing legal scrutiny.

The company also faces lingering financial constraints: absence of product revenues forces reliance on external capital infusion—whether equity offerings or debt drawdowns—to maintain research momentum without triggering liquidity shortfalls.[F1],[S15]

The revolving credit facility bears interest rates above typical corporate borrowing costs reflecting elevated risk premiums tied to biotech funding volatility,[S15] thus pressuring future profitability profiles once commercial sales commence.

Corporate governance dynamics such as stockholder approval requirements related to loan fee share issuances inject additional execution dependencies.[S15]

Lastly, market competition from larger pharmaceutical firms developing alternative checkpoint inhibitors or novel cell therapies may crowd out adoption despite orphan drug niche advantages.

Comprehensively managing these risk vectors while advancing development milestones predicates long-term success prospects.

Near-Term Catalysts to Track: Trials, Approvals, and Financing

Investors should monitor tangible operational checkpoints progressively shaping TuHURA's forward outlook:[S2],[S3]

- Completion dates for interim safety and efficacy assessments within the ongoing IFx-2.0 Phase 3 study—a possible harbinger for accelerated regulatory dialogue or adaptive trial modifications;

- FDA communications related to supplemental orphan drug applications or Fast Track status expansions influencing competitive positioning;

- Stockholder voting outcomes on loan fee share issuance affecting capital structure flexibility;

- Pipeline updates from Kineta-derived assets including IND filings or early-phase clinical data announcements;

- Quarterly financial disclosures spotlighting cash burn trajectories versus available credit; any amendments reflecting additional fundraising initiatives or changes in credit line terms. These markers offer measurable insights into execution capacity amid developmental headwinds and financial stewardship efficacy.

Latest Financial Profile: Cash Position and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $6mm | |

| 2026-03-31 | ||

| Current assets | $7mm | |

| 2026-03-31 | ||

| Current liabilities | $6mm | |

| 2026-03-31 | ||

| Current ratio | 1.15x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

At March 31, 2026 quarter-end,[F1] TuHURA reported cash & equivalents totaling approximately $6.3 million against minimal recorded debt nearing $265—indicating nominal leverage risk given relative liquidity.[F1] Current assets stood around $6.98 million balanced against current liabilities approximating $6.07 million resulting in a current ratio near 1.15 signifying close working capital equilibrium but leaving narrow buffer zones.[F1]

The freshly established $50 million revolving credit facility arranged in April extends funding capacity materially,[S15] providing a tangible runway into early calendar year 2028 assuming adherence to agreed borrowing limits tied to budgeted expense levels.[S29] This financial architecture supports ongoing multi-year R&D investment needs critical through pre-commercialization phases.

Given no revenue generation presently,[F1] operational reliance on continued capital inflows heightens sensitivity to external financing market conditions impacting borrowing costs and equity issuance feasibility.[S15] Continued prudent cash management combined with milestone-driven financing will remain core pillars safeguarding survival through uncertain clinical development durations.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available SEC filings as of May 16, 2026. It does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments