Immunocore’s Growth Transition Constrained by R&D Investment and International Risks

Immunocore Holdings plc shows improving operating results within a challenging biopharma development context marked by regulatory and geopolitical risks.

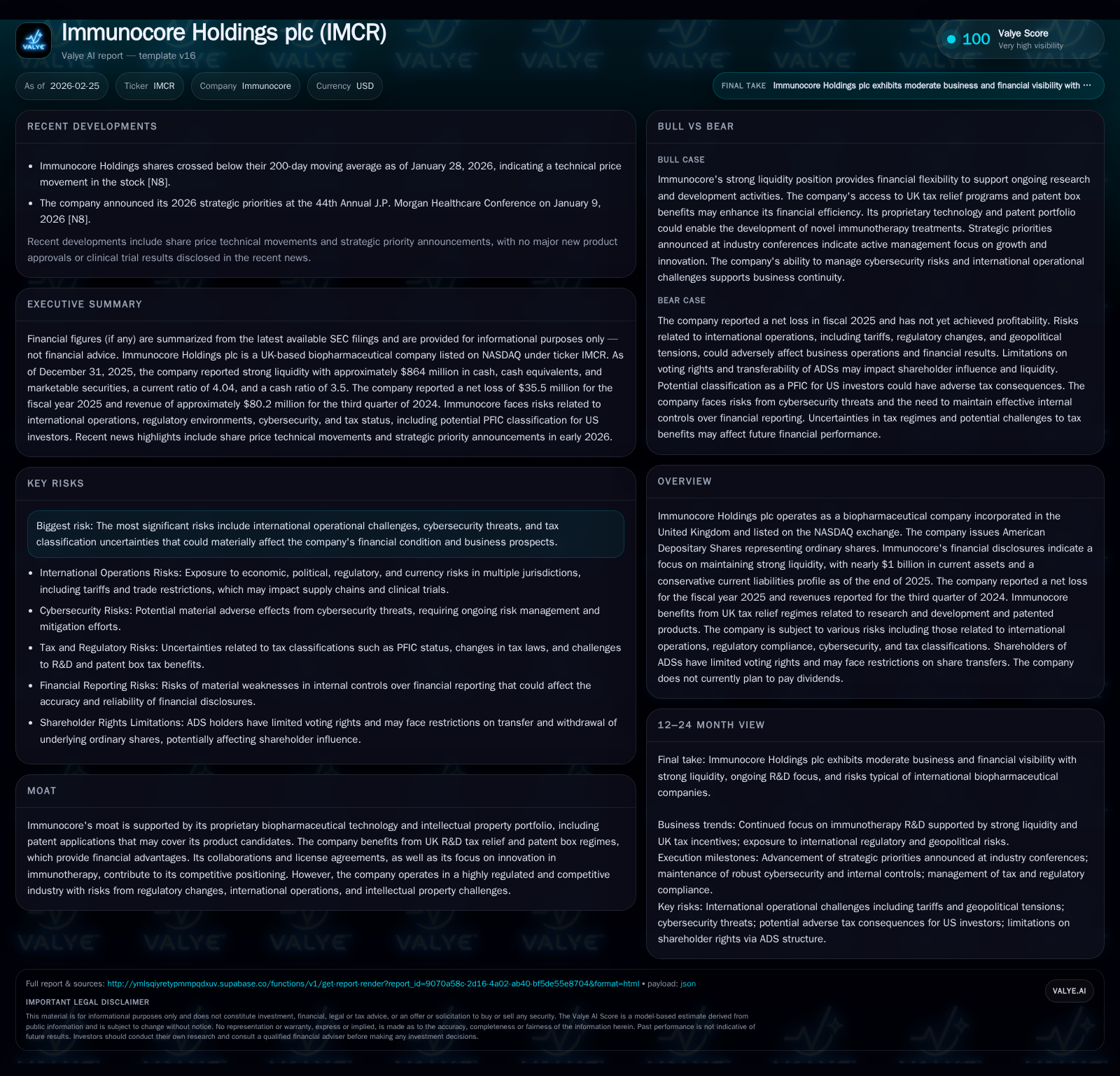

Immunocore Holdings plc, a UK-based biopharmaceutical company specializing in T-cell receptor immunotherapy, has experienced steady revenue growth alongside persistent operating losses. The company benefits from strong liquidity and UK tax incentives but faces significant constraints from international regulatory complexities, geopolitical uncertainties including trade tariffs, and ongoing R&D costs. Future growth hinges on clinical development milestones and commercialization efforts, while capital allocation currently prioritizes reinvestment over shareholder returns.

Company Background and Historical Performance

Immunocore Holdings plc is a United Kingdom-incorporated biopharmaceutical company that focuses on therapies based on proprietary T-cell receptor technology for oncology and infectious diseases [S1]. It trades on the NASDAQ exchange under the ticker IMCR via American Depositary Shares (ADSs). The company’s product candidates are still largely pre-commercial, which explains its operating losses despite accelerating revenue recognition in recent years.

Historically, Immunocore has demonstrated top-line growth with revenues increasing from approximately $249 million in FY2023 to $80 million reported through the first three quarters of 2024 [F1]. However, operating income remains negative, though improving: operating losses narrowed from -$59.6 million in FY2023 to -$70.5 million in FY2024 before improving to -$45.4 million in FY2025—a positive trend with a 35.6% year-over-year reduction [F1]. Net income follows this trajectory with net losses narrowing from -$55.3 million in FY2023 to -$51.1 million in FY2024 and further to -$35.5 million in FY2025 [F1].

This pattern reflects scaling costs associated with intensive research and development activities typical for innovative biotech firms that have not yet brought broad commercial products to market [S1]. Notably, capital expenditure has modestly decreased from about $5.4 million in FY2023 to $4.3 million in FY2025, indicating controlled investment into infrastructure [F1]. Operating cash flow turned positive temporarily in FY2024 at about $26 million but swung back to negative around -$10.7 million in FY2025, yielding free cash flow of roughly -$15 million after capex [F1]. The company maintains strong financial flexibility supported by nearly $1 billion of current assets against relatively low current liabilities ($247 million), producing a healthy current ratio above 4 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -36 | -11 | -45 | 4 | +30.5% |

| 2024 | -51 | 26 | -70 | 5 | +7.6% |

| 2023 | -55 | 3 | -60 | 5 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -15 | -9.3 |

| 2024 | 21 | -14.2 |

| 2023 | -2 | -15.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue data only available through Q3 2024; Dividend and buyback data not disclosed.

Business Model and Industry Context

Immunocore operates within the highly competitive immuno-oncology sector characterized by intensive R&D cycles and complex regulatory approval pathways [S1]. Its focus on T-cell receptor fusion proteins leverages proprietary biotechnology protected by numerous patent applications under active management [S1]. The company also benefits from UK government incentives such as R&D tax credits (approximately 15-16%) and the patent box regime allowing an effective corporate tax rate of around 10% on qualifying income—significant advantages enhancing post-tax returns relative to peers [S22][S23].

However, key challenges include stringent global regulatory environments across multiple jurisdictions given Immunocore’s international operations involving suppliers and clinical trial sites outside the US [S2][S13]. Economic instability, inflationary pressures, geopolitical tensions—including new US-EU pharmaceutical tariffs anticipated to raise import costs—and uncertainties related to Brexit continue to add complexity [S2][S21]. Unlike some other industries, pharmaceutical pricing methodologies limit Immunocore’s ability to pass increased tariffs onto customers directly, potentially compressing margins even if commercial products launch successfully [S4].

Cybersecurity emerges as a critical governance focus due to the sensitivity of clinical trial data and intellectual property involved; Immunocore employs rigorous risk management practices led by an experienced CIO reporting directly to senior leadership and overseen by the board's audit committee [S9][S15].

Future Growth Prospects

Immunocore’s near- to mid-term growth depends heavily on successful progression through clinical trial phases for its pipeline candidates followed by regulatory approvals that enable commercialization [N9][S1]. While no explicit revenue guidance is available publicly, monitoring clinical milestones—including late-stage trial readouts and approval decisions—will be essential indicators of potential revenue inflection points (analysis). Collaborations such as those mentioned with external partners (e.g., Gates Foundation collaboration cited historically) contribute incremental support but remain secondary relative to proprietary product advancement [S1].

Potential risk factors tempering growth include challenges securing freedom to operate internationally amid evolving patent landscapes and regulatory discrepancies between regions; disruptions arising from geopolitical conflicts impacting supply chains or trial sites (notably Eastern Europe and Middle East exposure); cybersecurity incidents; and changes in tax legislation reducing prior cost savings benefits [S2][S21][S9][S16][S22]. The nascent nature of many product candidates also means that pipeline disappointments could sharply affect future prospects.

Capital Allocation and Returns

Immunocore currently focuses its capital allocation strategies on sustained investment in research activities rather than shareholder distributions or share repurchases—no dividends have been declared or planned given accumulated net losses since inception exceeding distributable profits thresholds per UK law [S14][F1]. Equity base stands around $381 million at year-end 2025 with return on equity modestly negative at approximately -9% due primarily to net losses [F1]. There is no indication of near-term capital return programs; instead, shareholder resolutions permit share issuance flexibility enabling potential equity raises if needed for financing ongoing operations or strategic initiatives [S17][S18].

Operational cash flow remains volatile due largely to timing of milestone payments tied to study progress or licensing agreements; managing cash burn while preserving runway continues as a central priority.

Risks Summary

Prominent risks facing Immunocore encapsulate:

- International operational complexities including diverse regulatory standards, customs tariffs (including recently outlined US-EU pharma tariffs), currency fluctuations, and political-economic instability compounded by Brexit outcomes [S2][S21][S24];

- Cybersecurity threats targeting sensitive clinical trial data and intellectual property necessitating constant vigilance with escalation protocols for incidents overseen at board level [S9][S12];

- Tax classification uncertainties such as potential reclassification as Passive Foreign Investment Company (PFIC) for US investors or changes reducing benefits from UK R&D relief/patent box regimes impacting effective tax rates adversely [S23][S16];

- Limitations attached to ADSs traded on NASDAQ including restricted voting rights vis-à-vis ordinary shares potentially affecting shareholder influence on governance decisions [S1];

- Legal jurisdiction choices limiting favorable forums for shareholder claims possibly increasing litigation costs or complexity [S6];

- Dependency on success of ongoing clinical trials; any delays or failures could materially impair long-term viability.

Important Indicators To Watch (Analysis)

- Progression timeline and results readouts for lead drug candidates in Phase II/III trials.

- Regulatory approvals particularly within major markets (US FDA/EU EMA).

- Commercial launch execution effectiveness post-approval including reimbursement negotiations.

- Developments regarding international tariff implementations affecting supply chain economics.

- Cash burn rates relative to financing capacity including equity issuance plans.

- Any material cybersecurity incidents or regulatory enforcement actions.

Conclusion

Immunocore Holdings plc reflects attributes typical for advanced-stage biopharmaceutical innovators balancing promising revenue trajectories with persistent R&D-driven losses amid volatile external risks inherent to global pharmaceutical development ecosystems. The company's moat rests on scientifically differentiated proprietary technology coupled with tax-efficiency frameworks under UK jurisdiction providing financial cushioning relative to some peers.

Ultimately, near-term prospects hinge critically upon successful clinical milestones and navigating complex cross-jurisdictional operational hazards amid tightened global trade environments that could affect margins post commercialization.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments