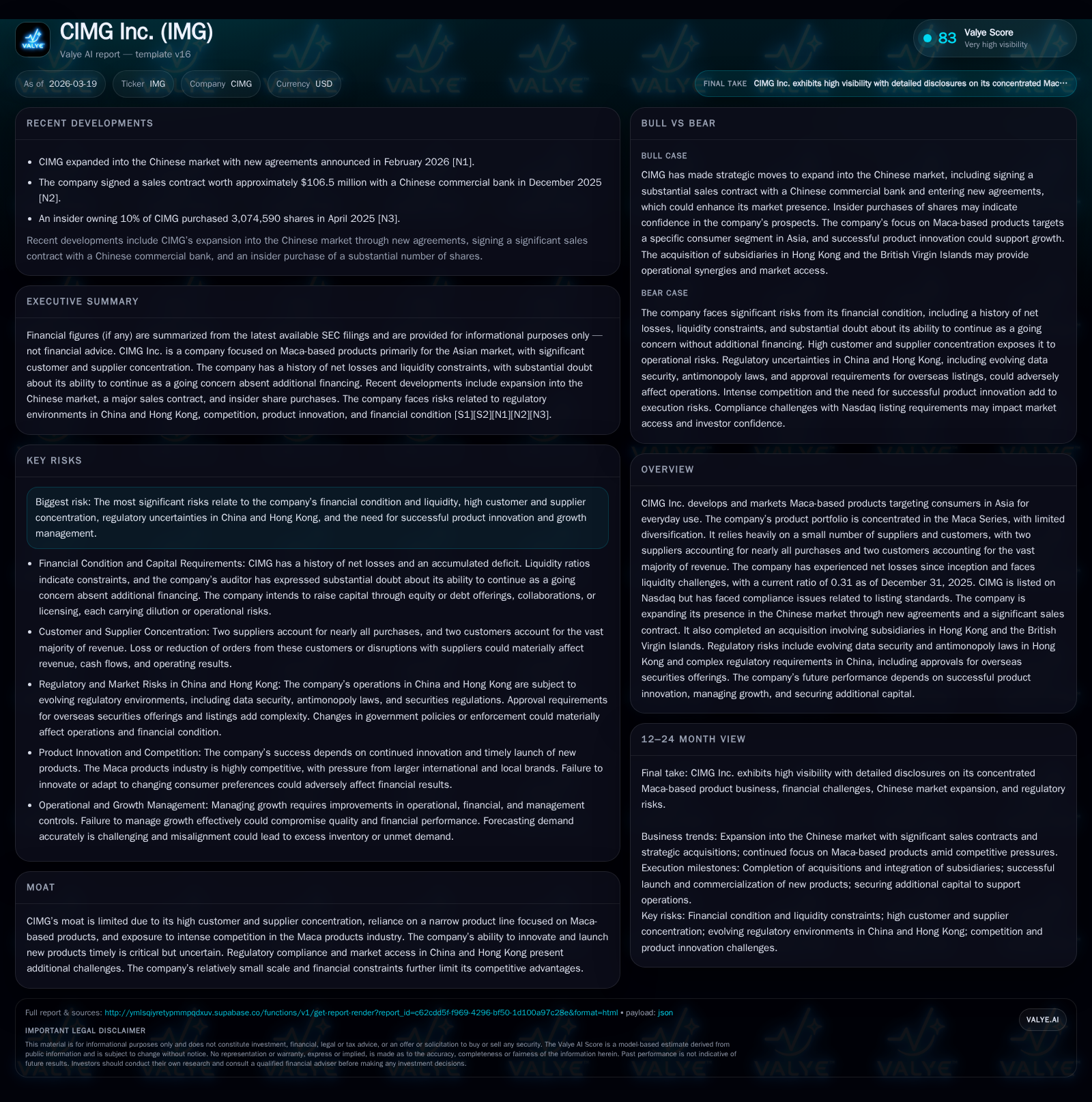

CIMG Inc.'s Maca Product Focus and Market Risks Define Its Growth Outlook

CIMG Inc. integrates concentrated supplier and customer reliance with strategic Chinese market expansion despite ongoing financial and liquidity pressures.

CIMG Inc., primarily engaged in the development and marketing of Maca-based consumer products in Asia, has experienced sustained net losses and liquidity challenges compounded by high supplier and customer concentration risks. Although revenue grew by 29.1% in FY2025, operating losses remain significant despite a 52.1% year-over-year improvement. Recently, the company expanded into the Chinese market through new agreements and acquisitions, presenting growth opportunities amidst regulatory complexities. Financially, the firm's low current ratio of 0.31 and history of negative operating cash flows underscore pressing near-term survival concerns. Successful innovation and effective management of regulatory and competitive barriers are critical for CIMG's trajectory.

Financial Trajectory: From Modest Revenue Growth to Persistent Losses

CIMG Inc.'s historical financial performance reveals a paradoxical pattern of growing top-line revenue coupled with lingering operating deficits. Revenues climbed from approximately USD 1.39 million in FY2018 to about USD 1.79 million in FY2019, marking steady albeit modest growth as the company expanded its Maca product sales in Asian markets [F1]. By FY2025, revenue improved markedly, increasing by 29.1% relative to FY2024 [F1], reflecting initial positive traction from strategic market entries.

Despite this growth in sales volume, operating income persists deep in negative territory at around -USD 5.2 million for FY2025—though this represents a meaningful 52.1% narrowing compared to the prior fiscal year [F1]. Net losses similarly reduced by roughly 45.6%, closing FY2025 at -USD 4.9 million [F1]. The company's cash flow profile further underscores operational challenges; operating cash flow deteriorated substantially reaching negative USD 17.6 million for FY2025 alone—a decline of over three-quarters year-over-year [F1]. Capital expenditures remained relatively flat around USD 320k reflecting limited investment capacity [F1].

This data traces a tentative yet fragile trajectory toward stabilizing operations overshadowed by ongoing cash burn characteristic of early commercialization phases common among niche wellness product ventures.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -5 | -18 | -5 | 319843 | +45.6% |

| 2024 | -9 | -10 | -11 | 319843 | -2.6% |

| 2023 | -9 | -7 | -9 | 16241 | +25.8% |

| 2022 | -12 | -7 | -11 | 191765 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -18 | -10.7 |

| 2024 | -10 | 1379.0 |

| 2023 | -7 | -522.6 |

| 2022 | -8 | -121.1 |

Source: SEC companyfacts cache [F1].

Table summarizing CIMG's recent annual financial results highlighting persistent losses despite revenue growth [F1].

Supplier and Customer Concentration: A Double-Edged Sword

The operational fabric of CIMG is highly dependent on an exceedingly narrow supplier and customer base that presents both leverage when stable but severe vulnerability otherwise. In FY2025 two suppliers accounted for approximately 96.8% of total company purchases [S6], showcasing acute supplier concentration risk typical within specialized natural product supply chains where quality standards are paramount yet sourcing options are limited.

Such concentration exposes CIMG to pricing pressure, supply chain disruption risk from capacity constraints or quality issues, as well as potential delays impeding product availability—a critical factor when rapid response to market demand shifts is essential.

Simultaneously, customer dependence mirrors this pattern—two customers contributed approximately 96% of CIMG’s total revenue during FY2025 [S6], with one representing about 60% alone [N1]. This creates revenue predictability challenges because losing or facing order reduction from either major customer could materially impair top-line results and cash flow stability.

Reliance on few entities thus intertwines credit risk management directly with broader commercial execution strategies.

Chinese Market Expansion: Agreements and Acquisition Moves

Fresh growth impetus arrives from CIMG’s explicit push into Mainland China’s lucrative wellness market evidenced by multiple recent agreements announced in early 2026 [N1][S3]. Notably, the company executed a sizable sales contract signaling intent to deepen market penetration beyond existing footprints primarily focused in Hong Kong.

Moreover, an acquisition involving subsidiaries domiciled in Hong Kong and the British Virgin Islands was completed per an amended equity transfer agreement executed February–March 2026 [S26][S28]. This move is designed both to enhance control over regional business operations and capitalize on synergies across adjacent jurisdictions.

While these steps potentially diversify geographic revenue sources away from over-dependence on limited customers domestically, they also significantly raise exposure to nuanced regulatory frameworks governing cross-border commerce including data privacy regimes and antimonopoly compliance in China/Hong Kong.

Navigating local administrative complexities while adapting products for consumer tastes amidst evolving distribution channels will test organizational capabilities.

Regulatory and Competitive Barriers: Navigating Uncertain Waters

CIMG operates within an intricate web of regulatory standards that pose complex compliance challenges impacting operational freedom. The firm faces prospective cybersecurity review requirements under China’s increasingly stringent network data security laws—though currently exempt due to scale thresholds—plus uncertainties surrounding future enforcement interpretations that could hamper data handling practices [S23]. These policies are especially pertinent given consumer personal information usage embedded within marketing analytics.

Further complicating matters are antimonopoly rules aimed at preserving competitive landscapes which place constraints on vendor agreements or pricing strategies potentially limiting exploitable commercial levers.

The Maca products space itself remains intensely competitive globally with CIMG vying against large multinational firms wielding greater financial resources alongside nimble local/regional players including private-label offerings developed by key retail chains [S22]. Maintaining differentiation through quality assurance, innovation cycles, timely product launches (the "commercialization cycle") and pricing agility remains crucial for sustaining market share.

Failure to safeguard intellectual property rights could expose CIMG both to infringement claims costly to defend and potential erosion of its distinct product positioning [S7][S21].

Capital Structure and Liquidity: Near-Term Survival Concerns

Liquidity metrics underline immediate existential risks confronting CIMG. As of December 31, 2025, current assets stood at approx USD 3.4 million compared to liabilities surpassing USD 10.9 million resulting in a distressed current ratio of only about 0.31 [F1], firmly below healthy operational thresholds indicating looming short-term funding gaps.

The auditor's report includes an explanatory paragraph highlighting substantial doubt about the company's ability to continue as a going concern absent successful financing or operations turnaround [S1]. Past capital raises included convertible notes aggregating USD 5 million with associated warrants issued recently as part of twin-tranche closings during February 2026 designed to shore up funding albeit contingent upon shareholder approvals subject to Nasdaq rules [S5][S8][S10].

Operating cash flow trends reveal accelerating negative outflows intensifying from nearly USD -7 million annually during FY2022-FY2023 towards almost USD -18 million by FY2025 tied partly to expanding commercial rollout but unsupported by net earnings conversion [F1].

These conditions necessitate continued capital injections or debt restructuring initiatives presenting dilution risks for existing shareholders alongside potential covenants restricting future financial strategy flexibility.

Innovation Imperative: Product Development as a Growth Catalyst

Given the company's concentrated Maca-based portfolio amid fierce competition, innovation serves as a pivotal differentiator shaping future viability. Continuous research & development investments targeting enhanced formulations or diversified product iterations could stimulate renewed customer interest and improve margins provided commercialization timelines align tightly with evolving consumer preferences particularly within wellness-conscious Asian demographics [S24][S26].

Product pipeline management involves balancing rapid go-to-market execution while ensuring sufficient quality validation amid regulatory scrutiny—a delicate equilibrium often fraught with timing pressures impacting brand reputation.

Strategic partnerships or licensing deals may also augment internal development capacities but require careful negotiation respecting existing intellectual property frameworks.

Delays or failures in launching innovative products could exacerbate revenue fluctuations already observed due to the nascent stage of mainstream adoption for certain offerings under their business model [S1][S22].

Forecast Indicators and What Investors Should Monitor

Explicit company forecasts remain undisclosed creating heightened reliance upon milestone tracking for forward insight: key indicators include performance outcomes from recent Chinese market contracts [N1], success metrics tied to newly acquired subsidiaries integration [S3], progress in negotiating or securing alternate suppliers mitigating concentration risk exposure [S6], along with responses by regulators regarding data security compliance evolution [S23].

Additionally, monitoring capital raise execution efficacy—particularly whether tranches convert promptly without adverse shareholder backlash—and subsequent liquidity improvement measures will be instructive signs of resilience or vulnerability.[N1][S5]

Sector observers should also watch competitive moves within core Maca marketplaces that may influence CIMG’s relative standing given compressed margins commonly reported.

Dividend Policy, Buybacks, and Return on Equity Insights

Capital allocation priorities overwhelmingly focus on preserving operational capabilities rather than shareholder returns at this juncture as reflected by absence of dividends or significant stock repurchase activity over recent years save minimal buybacks dating back several years documented at low levels (~USD15) [F1][S9][S19].

Return on equity remains deeply negative estimated around -10.7%, illustrative of ongoing loss absorption detrimental to equity value creation under current business conditions [F1].

Management’s stance appears prudently aligned toward liquidity conservation enabling strategic investments needed for growth rather than pursuing near-term distributions potentially unfeasible given capital constraints expected through the next fiscal periods.

Disclaimer: This analysis synthesizes publicly available SEC filings and news reports up to March 19, 2026 without forward-looking investment recommendations or forecasts beyond documented disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments