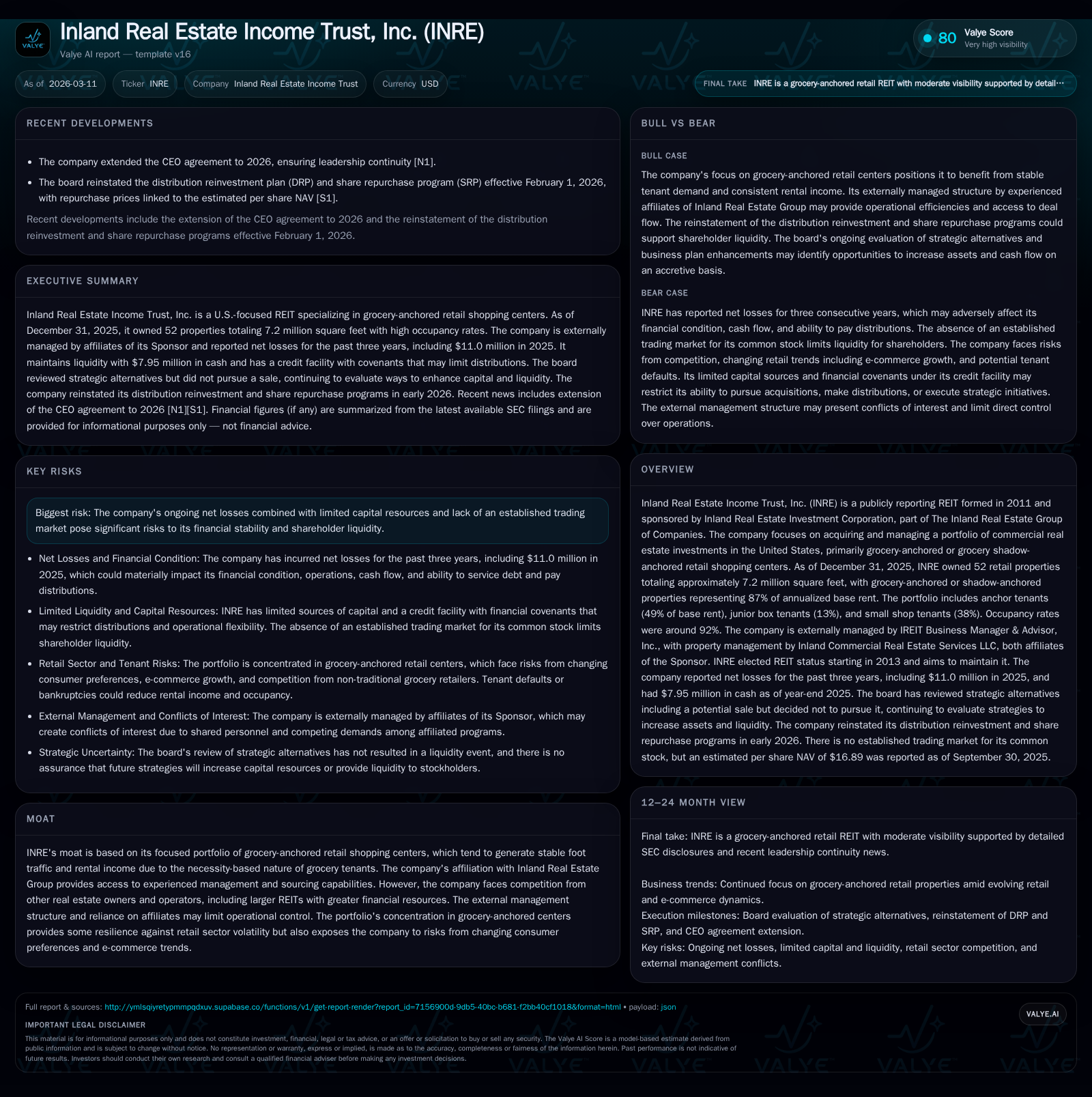

Inland Real Estate Income Trust: Balancing Portfolio Focus and Financial Pressures

Stable grocery-anchored retail properties underpin Inland REIT’s leasing performance despite persistent net losses and capital challenges.

Inland Real Estate Income Trust, Inc. maintains a portfolio concentrated in grocery-anchored retail shopping centers that supports occupancy near 92% and a relatively stable annualized base rent profile. However, the company has incurred net losses for several consecutive years, reflecting operational costs amplified by its external management structure and constrained capital resources. Its capital structure features sizable revolving credit and term loan facilities with covenants that limit flexibility, while dividend payments and share repurchases continue despite these financial pressures. The board’s recent strategic review aims to enhance asset growth and liquidity, though no immediate milestones or liquidity events are guaranteed.

Portfolio Composition and Historical Growth Drivers

Inland Real Estate Income Trust (INRE) specializes in grocery-anchored or grocery shadow-anchored retail shopping centers — a niche that inherently benefits from stable tenant demand due to the necessity-based nature of grocery stores. As of December 31, 2025, the portfolio comprised 52 retail properties with a total of approximately 7.2 million square feet [S1]. Grocery-anchored or shadow-anchored assets accounted for roughly 87% of annualized base rent (ABR), underscoring the company's deliberate focus on high-foot-traffic locations.

The ABR per square foot averaged $19.57 in 2025, a marginal decrease from prior years but still reflective of relative pricing stability within this segment [S1]. Occupancy hovered at about 92%, with physical occupancy at 92.0% and economic occupancy closely aligned at 92.2%, indicating a robust lease-up status in leased space metrics [S1]. The portfolio is diversified across anchor tenants (49% ABR), junior box tenants (13%), and small shop tenants (38%), capturing different tenant sizes that collectively support base rent stability.

Historically, INRE's operating income experienced significant growth culminating in $18 million in fiscal year 2018, up dramatically from $5.3 million in FY2017 — an extraordinary year-over-year increase of approximately 239% based on available data [F1]. This jump likely reflected either portfolio expansion or improved property operational efficiencies during that period. However, this rise in operating income did not translate into sustained overall profitability as net income remained negative thereafter.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -11 | 43 | 2 | +26.2% |

| 2024 | -15 | 43 | 4 | +1.0% |

| 2023 | -15 | 39 | 1 | -19.9% |

| 2022 | -13 | 45 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 20 | 5 | 41 |

| 2024 | 20 | 5 | 40 |

| 2023 | 20 | 6 | 38 |

| 2022 | 20 | 4 | 45 |

Source: SEC companyfacts cache [F1].

Table illustrates oscillating operating income growth contrasting with persistent net losses; includes cash flow stability amid reduced capex reflecting cautious capital spending [F1].

Operating Costs, Net Income Trends, and External Management Effects

Despite positive swings in operating income during earlier years within the reported range, INRE experienced continuous GAAP net losses from at least 2022 through the end of fiscal year 2025: net losses were $12.6 million (2022), $15.1 million (2023), $15.0 million (2024), and $11.0 million (2025) respectively [F1]. This persistent bottom-line deficit suggests operating expenses have remained elevated relative to gains.

A critical factor is INRE’s external management structure where its operations are managed by Inland Real Estate Investment Corporation-affiliated entities: the IREIT Business Manager & Advisor handles external management functions while Inland Commercial Real Estate Services LLC manages properties [S1]. Such arrangements—common among non-listed REITs—can result in management fees and related expenses that weigh on profitability metrics if operational scale does not generate sufficient overhead absorption or economies of scale.

Operating cash flows have remained relatively stable despite net losses; CFO was $44.8 million in FY2022 decreasing slightly to $42.7 million by FY2025 [F1]. The ability to generate consistent operating cash flows indicates rental collections continue effectively even as accounting conventions and expenses push GAAP earnings negative.

Capital expenditure levels have been modest but increased cautiously over time (from $253k in FY2022 to $1.63 million in FY2025), reflecting limited reinvestment possibly aimed at preserving liquidity [F1]. The interplay between externally influenced cost structures and efforts to maintain cash flows marks key tension underlying INRE's financial results.

Capital Structure Complexity and Liquidity Constraints

INRE’s capital structure presents a blend of revolving credit facilities alongside term loans totaling approximately $860 million drawn primarily under agreements established or amended as recently as November 2025 [S4][S8][S9]. The revolving credit subfacility specifically provides up to $285 million availability, with borrowings standing at roughly $248 million as of December 31, 2025 [S4], leaving only a small buffer for additional draws given covenant limits.

The company’s leverage ratio stood at approximately 57% at year-end compared to a maximum covenant threshold of about 65%, reflecting some breathing room yet highlighting limited capacity for further borrowings without violating terms [S4][S5]. Covenants also impose consolidated tangible net worth requirements influencing capability to make distributions or pursue acquisitions without lender consent.

Notable features include cross-default provisions tying together mortgage defaults across subsidiary entities which amplify risk should any tenant bankruptcy trigger reductions in property valuations affecting covenant compliance [S5][S7]. Many loans hold interest-only periods with balloon maturities due by April 2029, injecting refinancing risk in an uncertain credit market environment characterized by rising interest rates tied primarily to Term SOFR benchmarks plus variable margins dependent on leverage [S6][S27].

Variable-rate debt exposure close to half of total borrowings introduces sensitivity to Fed policy moves; INRE employs derivative instruments such as interest rate swaps for partial hedging though residual risks remain material [S24][S27]. Additionally, lock-out provisions restrict prepayments or sale proceeds usage during certain periods impeding capital flexibility [S14].

Overall tight liquidity combined with layered covenant restrictions demand rigorous monitoring especially amid market volatility that could impair access or cost of financing going forward.

Dividend Policy, Shareholder Returns, and Capital Allocation Decisions

Although INRE has reported ongoing GAAP net losses for multiple recent periods, it maintained broadly consistent dividend payments averaging approximately $19.6 million annually between FY2022 and FY2025 [F1]. These payments comply with REIT obligations requiring distribution of taxable income but may be funded partially from sources other than operational cash flow earnings given reported deficits [S22].

Share buybacks under an amended Share Repurchase Program were reinstated effective February 1, 2026 after suspension during strategic reviews; recent repurchase values approximated around $5 million annually indicating modest activity relative to overall equity base [$F1][S10][S19]. The repurchase price framework links closely to Estimated Per Share NAV — last reported at $16.89 as of September 30, 2025 — with ordinary repurchases occurring at an approximate discount reflecting liquidity constraints [S11][S25][S23].

With equity declining from above $451 million (FY2022) down to around $325 million by FY2025 largely driven by accumulated losses [F1], approximate return on equity stands negative near -3.4%. Free cash flow generation remains positive near $41 million after capex adjustments illustrating some internal funds available for distributions or reinvestment despite unprofitability on GAAP basis.

These allocation patterns underscore management’s prioritization of sustaining shareholder distributions where feasible but constrained buyback scope due to limited liquidity reserves.

Future Growth Opportunities and Strategic Review Outcomes

The board initiated a comprehensive strategic review process aimed at assessing business plans focused on accretive asset growth alongside efforts to bolster equity capital resources providing improved liquidity options for stockholders over time [S1]. While no definitive liquidity events such as listing or sale materialized following this review through early 2026, the company has committed the Business Manager to pursue plan enhancements designed to grow assets sensibly within existing debt constraints plus explore alternate value-accretive avenues [N1][S16].

Potential strategies under consideration include selective acquisitions of grocery-anchored centers positioned in favorable markets as well as redevelopment initiatives converting vacant big-box shell spaces into higher-yielding uses — although no transactions were conducted since last acquisitions closed in early-to-mid-2022 timeframe [S17].

Meanwhile management’s reiteration of CEO agreement into March/April 2026 supports continuity amidst ongoing evaluation phases although concrete milestones remain undefined absent public guidance or formal growth targets beyond qualitative commentary [N1]. Thus stakeholders should expect incremental progress balanced cautiously against existing financial limitations.

Navigating Debt Covenants in a Volatile Credit Environment

The credit facility governing INRE’s primary indebtedness incorporates rigorous covenants including maximum leverage ratios (~65%) and consolidated tangible net worth minimums designed to safeguard lenders yet restrict agility for funds application toward expansions or distributions without prior consent [S4][S7]. Failure to comply constitutes default events potentially accelerating repayment obligations which would materially impact liquidity.

Cross-default clauses link obligations across subsidiaries preventing isolated renegotiations without cascading consequences; tenant bankruptcies exacerbate these risks as they may reduce valuations impacting covenant formulas even if rents continue momentarily flowing under leases [S5][S24]. Interest-only loan periods lower scheduled outflows temporarily but introduce balloon payment risk approaching maturity horizons requiring refinancing or asset disposals under uncertain market conditions marked by tightening underwriting standards stemming from Fed rate hikes [S9][S27][S13]. Lock-out provisions impede prioritizing voluntary principal repayments or asset sales temporarily restricting turnaround options [S14].

Derivative instruments mitigate some interest rate variability risk partially but carry inherent counterparty risks alongside basis mismatches limiting full hedge effectiveness in turbulent markets constrained further by rising funding costs evidenced through incremental margins tied variably either leverage ratios or issuer credit ratings when applicable [S24][S27].

Overall capital stewardship demands meticulous navigation balancing compliance risks against the imperative for growth financing amid compressed market conditions affecting commercial real estate lending availability.

Key Milestones and Market Watch Points for Investors

Explicit company guidance remains sparse; however investors should focus attention toward the following metrics and calendar events:

- Maintaining occupancy close to current (~92%) supports rental revenue stability needed for sustaining dividends amid challenges [S1];

- Refinancing risks intensify approaching April 2029 maturity dates on both Revolving Credit Facility extensions optioned only once subject to fees/consent requiring early planning given extant credit market volatility [S8];

- CEO leadership continuity assured through first half of calendar year via contract extension mitigates operational disruption threats during strategy execution windows [N1];

- Monitoring Funds From Operations (FFO) metric trends which ideally align more closely with distributable cash flow given GAAP distortions affecting reported earnings;

- Progress or announcements concerning strategic plan outcomes such as acquisitions or redevelopments that can shift trajectory from maintenance mode toward accretive growth remain pivotal;

- Developments regarding shares’ potential public listing prospects influence liquidity possibilities substantially although none are currently committed per disclosures.[S16]

Prudence dictates careful appraisal given no assurances exist related to liquidity events or equity issuance timing challenging valuation clarity while leveraging capital judiciously within covenant frameworks further defines operational latitude going forward.

This analysis synthesizes INRE's disclosures as filed through March 11, 2026 focusing exclusively on factual data without extrapolation beyond available filings ([F1],[N1],[S1][...][S29]). It is intended solely for informational purposes illustrating corporate dynamics within its unique operational niche alongside evolving financial constraints typical among externally managed non-listed REITs concentrated on grocery-centric retail assets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments