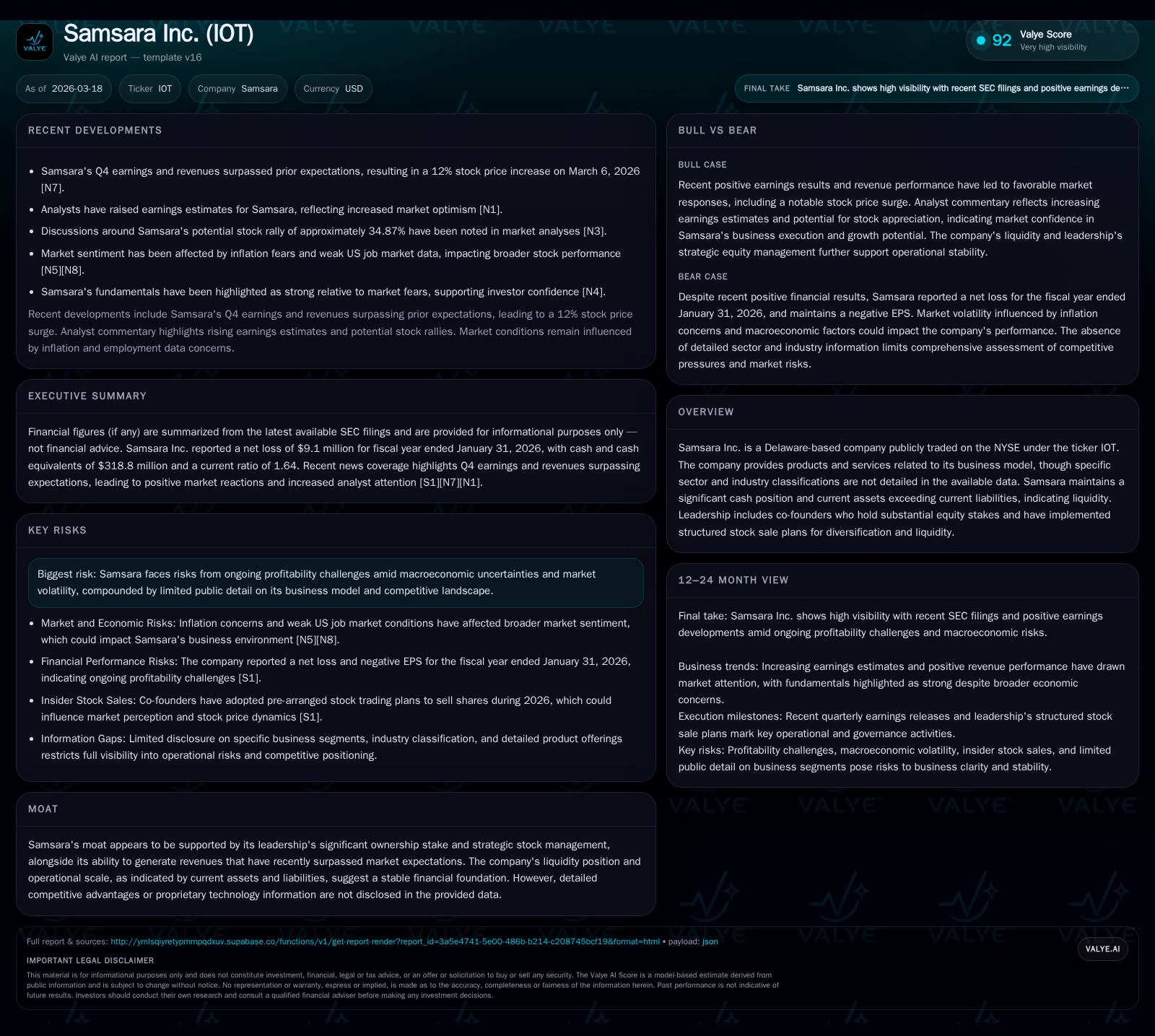

Samsara Inc. Strengthens IoT Foundations Amid Improving Financial Metrics

Samsara’s fiscal 2026 results reflect robust revenue gains and narrowing losses driven by its scalable Connected Operations Platform amidst strategic leadership equity plans.

Samsara Inc. reported a significant jump in revenue to $1.62 billion in fiscal year 2026, a roughly 30% increase from the prior year, driven by expanded subscriptions to its Connected Operations Platform that integrates IoT devices and AI-driven applications. The company improved its operating income loss by over 70%, narrowing net losses substantially, reflecting operational leverage as it seeks profitable scale. Key co-founders maintain substantial ownership but have initiated measured stock sale plans to enhance share liquidity. Though macroeconomic uncertainties and execution risks remain, Samsara's enhanced cash flow generation and platform ubiquity provide a solid base for future growth.

Evolution of Samsara’s Revenue and Profit Dynamics

Samsara has demonstrated an impressive acceleration in top-line growth over the past fiscal year. For FY2026 ending January 31, 2026, the company reported revenues of approximately $1.62 billion, marking an increase of roughly 30% compared to $1.25 billion in FY2025 [F1]. This growth underscores strong adoption of the Connected Operations Platform's recurring subscription model.

Profitability metrics also reflect meaningful improvement during the company’s substantial investments in platform scalability. Operating losses narrowed sharply by about 72%, from a deficit of nearly $190 million in FY2025 to approximately $53 million in FY2026 [F1]. Even more notable is the reduction in net loss by over 94%, with FY2026 net losses at just under $9 million compared to nearly $155 million in the previous fiscal year [F1]. These gains indicate operational leverage beginning to materialize as Samsara refines its cost structure against expanding revenue.

Operating cash flow surged substantially as well, with CFO increasing around 79% year-over-year to $236 million in FY2026 from approximately $132 million a year earlier [F1]. Capex expenditures rose moderately but remained controlled at roughly $29 million versus $20 million previously, supporting infrastructure expansion without compromising free cash flow generation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | -9 | 236 | -53 | 29 | +94.1% |

| 2025 | -155 | 132 | -190 | 20 | +46.0% |

| 2024 | -287 | -12 | -323 | 11 | -15.9% |

| 2023 | -247 | -103 | -259 | 33 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 207 | -0.6 | |

| 2025 | 111 | -14.5 | |

| 2024 | 0 | -23 | -31.3 |

| 2023 | 0 | -136 | -26.4 |

Source: SEC companyfacts cache [F1].

Table reflects fiscal year-end figures; revenue figures are approximated based on disclosed amounts [F1]

Dissecting the Connected Operations Platform and Market Penetration

At the core of Samsara's value proposition is its Connected Operations Platform—a unified ecosystem integrating IoT devices, AI-powered applications, and cloud analytics designed specifically for complex physical operations across multiple industries. This platform aggregates data from Samsara-owned IoT hardware such as gateways, cameras, and sensors, alongside third-party connected assets, delivering actionable insights via a cloud dashboard and mobile interfaces [S1].

Sector-native capabilities include telematics for fleet monitoring, AI video-based safety applications for accident prevention and compliance, asset tracking across distributed sites, routing optimization for logistics fleets, commercial navigation, predictive maintenance functionalities, digital forms automation, connected training programs, and site visibility tools. This breadth caters especially well to asset-heavy verticals like transportation logistics, construction projects, wholesale trade operations, manufacturing plants, utilities infrastructure management, and field services—a cohort historically underserved by legacy analog processes or fragmentary systems lack ing cloud connectivity [S1][N3][N4].

Through this platform approach coupled with per-asset per-application subscription pricing models typical within telematics SaaS markets, Samsara creates high lifetime value customer relationships anchored on digital transformation imperatives. Its technology effectively bridges offline physical assets with digital cloud ecosystems—crucial for clients managing compliance challenges including safety regulations and sustainability mandates.

Recent Earnings Highlights: Surpassing Estimates and Market Reaction

In Q4 fiscal year-end results announced March 5th, 2026, Samsara surpassed analyst consensus on both earnings and revenues boosting investor confidence amid broader market volatility [N3][N5]. The stock rallied by approximately 12% following these releases as improved operational metrics quelled concerns surrounding previous profitability skepticism in an inflationary environment marked by macroeconomic headwinds [N9][N11].

Earnings beats stemmed primarily from continuing strength in recurring subscriptions fueled by new device deployments and upsell within existing accounts—signaling positive momentum entering FY2027.

Growth Drivers and Sector-Specific Tailwinds for IoT Solutions

Looking ahead, several growth catalysts underpin Samsara's expansion prospects. Original equipment manufacturer (OEM) partnerships remain pivotal as embedded cloud connectivity proliferates among industrial hardware footprints—augmenting device connectivity beyond Samsara’s proprietary IoT ecosystem [S1][N7].

Moreover, increasing operational AI adoption—particularly in video-based safety applications that leverage computer vision to reduce accidents—boosts customer ROI metrics leading to stronger retention rates.

Digital transformation trends are pulling entire industry verticals toward holistic connectivity platforms as enterprises seek integrated visibility into dispersed operations with real-time decision-making capabilities enabling efficiencies unavailable under siloed IT frameworks.

Pricing models incentivize volume adoption through per-asset per-application subscription schemes aligning cost directly with usage intensities inherent to sectors like trucking fleets or multi-site warehousing networks.

Profitability Trends, Operating Cash Flow Strength, and Capital Efficiency

The financial trajectory showcases disciplined capital efficiency alongside improving scale economics. Operating cash flows leapt about 79% year-over-year reaching $236 million in FY2026 despite ongoing investments fueling expansion efforts [F1]. This yielded positive free cash flow estimated at roughly $207 million after deducting capital expenditures totaling around $29 million.

Return on equity remains modestly negative near -0.6%, reflective of continued reinvestment cycles inherent to high-growth technology companies transitioning toward profitability [F1]. No dividends have been declared nor have share repurchases been initiated during this timeframe—capital deployment is focused on sustainable organic growth paths rather than immediate shareholder distributions [S6][S7].

Leadership Equity Moves and Their Implications on Share Liquidity

Importantly for governance dynamics—with significant insider holdings concentrated among co-founders Sanjit Biswas (CEO) and John Bicket (CTO)—approximately one-third of shares outstanding remain beneficially owned collectively at around a combined stake exceeding 34% as of late calendar year November 2025 [S6].

These principals have implemented pre-arranged Rule 144 compliant stock trading plans commencing January through December calendar year 2026 aimed at methodically diversifying personal holdings while mitigating disruptive impacts on share liquidity or market perceptions during sales execution [S7].

Structured liquidity measures indicate long term alignment balanced pragmatically with diversification needs—a nuanced capital allocation choice reflecting maturity within executive ownership frameworks.

Key Risks: Macroeconomic Pressures and Operational Execution

Despite encouraging strides toward financial health there remain explicit risks warranting cautious appraisal. Inflation fears continue posing pressure on enterprise spending patterns related to technology upgrades amid uncertain labor dynamics flagged recently in U.S. market developments categorized by weakening job report numbers [N10][N12][N13].

Internally evident risk factors stem from execution complexities linked to scaling efficiently while broadening customer wallet share across heterogeneous industry sectors noted in SEC risk disclosures highlighting uncertainties around profitability milestones achievement amidst competitive intensity [S1][S4][S5]. Although details on direct competitors are limited publicly, implicit threats exist given traditional resistance within asset-heavy operators historically reliant on manual systems.

Outlook & What To Watch: Analyst Expectations Versus Potential Hurdles

From an analytical perspective—and absent explicit forward guidance within filings—the critical identifiers going forward will include upcoming quarterly earnings report commentary on subscription unit growth velocity tied closely to adding new enterprise customers or deepening existing platform penetration [N1][N8].

Additionally monitoring any adjustment in capital allocation philosophy including shifts towards share repurchase programs or dividend initiations would inform evolving maturity status.

Management discussions concerning enhancements to AI capabilities across their Applications suite or broadened OEM product integrations will serve as barometers indicative of sustained innovation capacity required for competitive differentiation.

Overall market sentiment shaped heavily by macroeconomic variables continues shaping backdrop against which Samsara must demonstrate consistent delivery; thus quarterly guidance revisions will be pivotal for investors calibrating confidence levels.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available documents dated up to March 18, 2026. It should not be construed as investment advice or recommendations regarding buying or selling securities issued by Samsara Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments