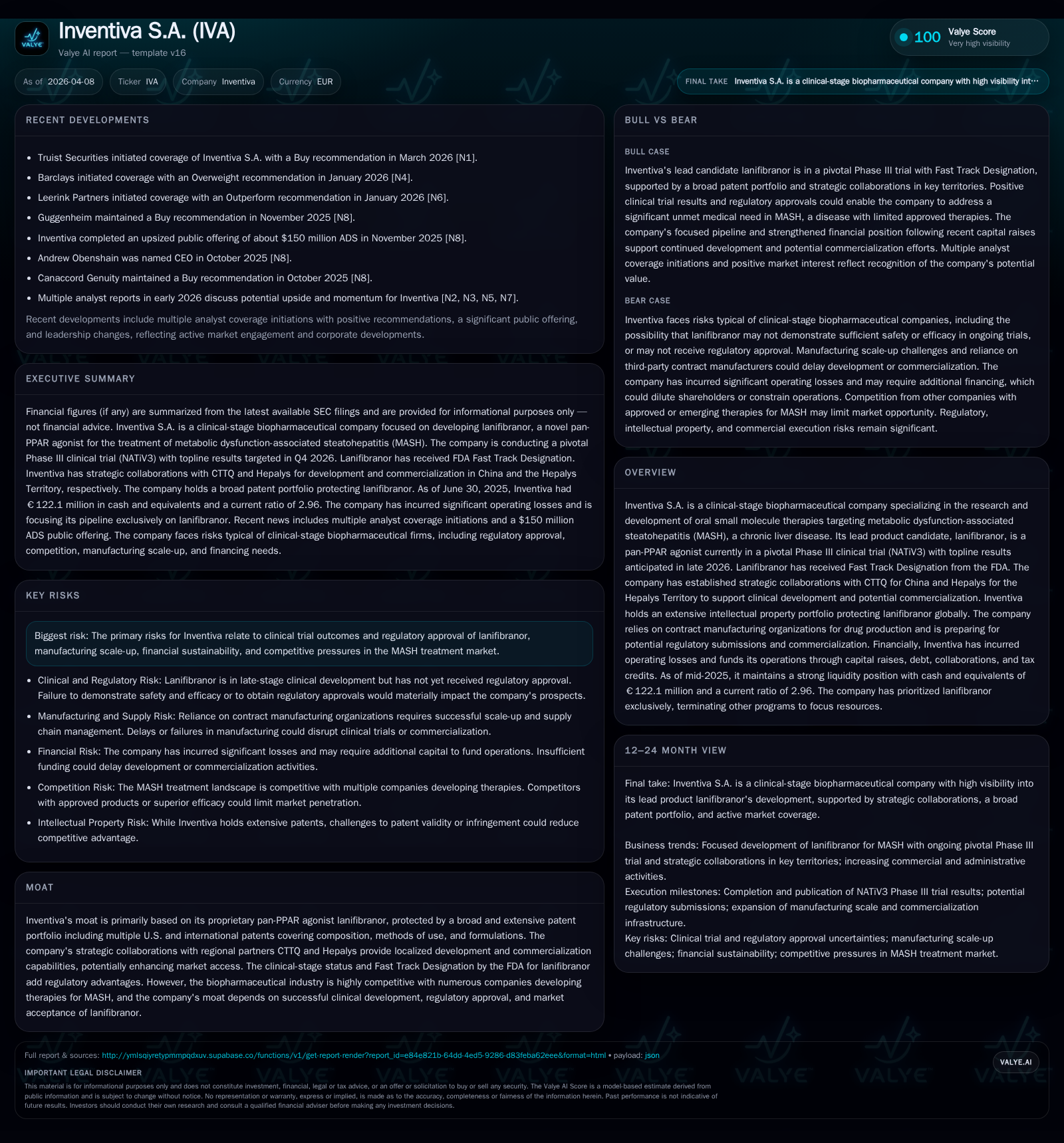

Inventiva S.A.’s Strategic Focus on Lanifibranor Faces Pivotal Phase III Readout and Capital Intensity

The clinical-stage biopharma is concentrating resources on its MASH therapy lanifibranor, navigating late-stage development risks amid intensifying competition and rising costs.

Inventiva S.A. operates as a clinical-stage biopharmaceutical company devoted primarily to the development of lanifibranor, a pan-PPAR agonist targeting metabolic dysfunction-associated steatohepatitis (MASH). The company’s growth trajectory hinges largely on the ongoing pivotal Phase III NATiV3 trial, with topline data expected late 2026. Historically, Inventiva has struggled with operating losses due to R&D investment but has secured substantial financing to fund its pipeline prioritization plan focused on lanifibranor. Strategic collaborations in China and Asia aim to bolster regional commercialization efforts, yet competitive pressures from approved therapies like Madrigal’s Rezdiffra present commercialization hurdles. Financially, Inventiva maintains a strong cash position supported by recent fundraising but faces significant contractual obligations and expected rising expenses as it advances toward regulatory filings and potential launch.

Company Background and Core Asset

Inventiva S.A. is a France-based clinical-stage biopharmaceutical company dedicated chiefly to developing oral small molecule therapies for metabolic dysfunction-associated steatohepatitis (MASH), a chronic liver disease affecting an estimated 2–6% of U.S. adults. Their lead candidate, lanifibranor, acts as a pan-PPAR agonist intended to leverage anti-fibrotic, anti-inflammatory, vascular, and metabolic benefits for MASH patients ([S1]).

Lanifibranor is under evaluation in the pivotal NATiV3 Phase III trial initiated in September 2021; enrollment completed April 2025 with topline results anticipated for Q4 2026. On positive outcomes, regulatory filing (NDA) could occur by H1 2027 targeting commercialization potentially starting in 2028 ([S1]). Lanifibranor has secured FDA Fast Track Designation facilitating expedited interactions and rolling review opportunities.

Historical Financial Performance

Inventiva’s financial history reflects typical biopharma clinical-stage dynamics: heavy operating losses driven by R&D expenditure without product revenue generation to offset costs yet.

Annual revenue has fluctuated reflecting milestone payments and collaboration income rather than sales:

Historical performance (annual)

| FY | Rev ($mm) | Rev YoY |

|---|---|---|

| 2024 | 9 | -47.4% |

| 2023 | 17 | +43.5% |

| 2022 | 12 | +190.4% |

| 2021 | 4 |

Source: SEC companyfacts cache [F1].

Net losses expanded significantly — over €354 million lost in fiscal year ending December 31, 2025 compared with €184 million in prior year — reflecting intensifying investment into the lanifibranor program including trial expansion, infrastructure build-out, and preparation for regulatory submission ([F1], [S1]).

Cash reserves improved markedly reaching approximately €122 million by mid-2025 with total current assets above €172 million against current liabilities near €58 million yielding a current ratio close to 3x ([F1]). This liquidity is principally supported by capital raises totaling €241 million in financing proceeds during calendar year 2025 through structured financing and public offerings primarily in U.S. markets ([S5],[S23]).

Strategic Refocus and Pipeline Prioritization

In early/mid-2025, Inventiva implemented a Pipeline Prioritization Plan terminating all other preclinical programs such as YAP-TEAD and NR4A1 to singularly concentrate resources on lanifibranor’s accelerated path forward. This process involved roughly halving workforce size by end of that year to streamline operations ([S1]).

Further strategic transactions included the December 2025 sale of the Odiparcil compound (assets related to another earlier pipeline candidate) to Biossil, generating upfront proceeds of approximately $0.6 million (€0.5m) plus potential future milestones up to $90 million if commercial success materializes—all risk-shifted away from Inventiva ([S1]).

Collaborations Enhancing Development Footprint

To augment clinical development reach and eventual commercialization scope for lanifibranor, Inventiva secured partnerships:

- CTTQ: agreement established in September 2022 focuses on China market support including patient randomization into NATiV3 within China starting in 2023 plus Phase I pharmacology studies.

- Hepalys: responsible for Hepalys Territory development/commercial authorization including Phase I trials conducted in Japan during 2025 with positive results supporting planned dedicated pivotal studies post-NATiV3 outcomes ([S1]).

These regional alliances afford localized expertise, funding sharing for trials, regulatory navigation assistance, and commercial infrastructure capabilities critical given geopolitical complexities around market entry into Asian healthcare systems.

Competitive Environment

MASH treatment space is intensely competitive with several players advancing therapies across various mechanisms targeting fibrosis reduction or metabolic modulation.

Madrigal Pharmaceuticals obtained FDA approval for Rezdiffra (resmetirom) in March 2024 for moderate-to-advanced liver fibrosis secondary to MASH — presently the only approved drug for this indication — while further candidates from Eli Lilly, Pfizer, Gilead Sciences, among others are progressing through earlier clinical stages ([S21]).

This dynamic complicates patient recruitment and retention for ongoing trials like NATiV3 due to availability of approved options, potentially impacting trial timelines or endpoints.

Payer access also presents risk amid growing scrutiny of pricing especially following U.S. Inflation Reduction Act provisions altering reimbursement frameworks ([S14], [S11]).

Intellectual Property Protection

Inventiva maintains a robust global patent estate protecting lanifibranor's composition-of-matter, methods of use, dosage forms including recent patent grants extending protections notably into Japan (July 2024) lining up with key commercial markets ([S1]). Such IP protection serves as an important barrier against generic competition post-launch.

Operational & Regulatory Considerations

Manufacturing relies on contract organizations; scaling up commercial supply while adhering to stringent cGMP compliance standards remains an execution risk ([S15]).

The company's regulatory strategy benefits from Fast Track Designation facilitating more frequent FDA engagements but requires demonstration of efficacy/safety meeting standard approval thresholds coupled with pharmacovigilance commitments post-market authorization ([S16]).

Additional hurdles include navigating evolving legislative environment around pricing transparency requirements as well as compliance regimes restricting promotional activity versus off-label uses both within EU and US jurisdictions ([S8], [S19]).

Financial Liquidity & Capital Allocation Patterns

Liquidity sources include equity raises comprising share issuances tied to royalty certificates plus structured finance agreements particularly via the European Investment Bank loan facility totaling €50 million drawn in two tranches at interest rates near ~7–8%, repayment scheduled through end-2026/27 periods ([S5], [S23]).

Operating cash outflows remain substantial due mainly to trial expenditures and infrastructure buildout; investing activities largely reflect increases in short-term deposits utilized as liquidity buffers rather than strategic capital expenditures ([F1], [S23]).

No dividends or share repurchases were reported—consistent with developmental stage focusing on growth capital retention rather than shareholder returns.

Outlook & Milestones To Monitor

Key upcoming events:

- Late-2026 release of NATiV3 topline data critically influencing regulatory filing prospects.

- Conditional NDA submission targeted H1 2027 subject to positive Phase III outcomes.

- Commercial launch planning contingent upon approvals aiming around or after 2028.

- Development progress monitoring within CTTQ-partnered China region plus Hepalys-driven Asian territories including initiation of localized pivotal studies post-NATiV3 readout ([N2], [N1], [S1]).

- Vigilance on competitive landscape shifts especially new entrant approvals or trial readouts.

- Watchfulness regarding legislative reforms impacting drug pricing or reimbursement given their implications on commercial viability.

Absent explicit guidance beyond these milestones, investors should monitor financial burn trends tied closely with late-stage development intensity alongside regulatory feedback cycles post-data release and partnership updates regarding regional launches.

Summary Impression

Inventiva’s concentrated pivot toward exclusively developing lanifibranor underscores commitment but concentrates risk onto successful late-stage trial execution and regulatory acceptance amidst a crowded competitive landscape where first-mover advantage exists but is challenged. Their capital structure appears adequate through near-term milestones fueled by recent financings though long-term sustainability depends heavily on licensing revenues or product sales following potential commercialization. Operational risks linked to manufacturing scale-up compliance remain alongside stringent global pharmaceutical regulation frameworks governing pricing transparency and promotion limiting marketing flexibility. The company’s wide patent coverage combined with strategic regional alliances represents foundational strengths though ultimate value crystallization relies on bridging execution through approval hurdles into market adoption.

Disclaimer: This report is prepared solely for informational purposes based on public sources cited herein; it does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments