SIMPPLE LTD. Emerges as a Robotics Pioneer in Facilities Management with Expanding Global Footprint

SIMPPLE LTD. drives rapid revenue growth through its proprietary integration of AI, robotics, and IoT despite financial and operational hurdles.

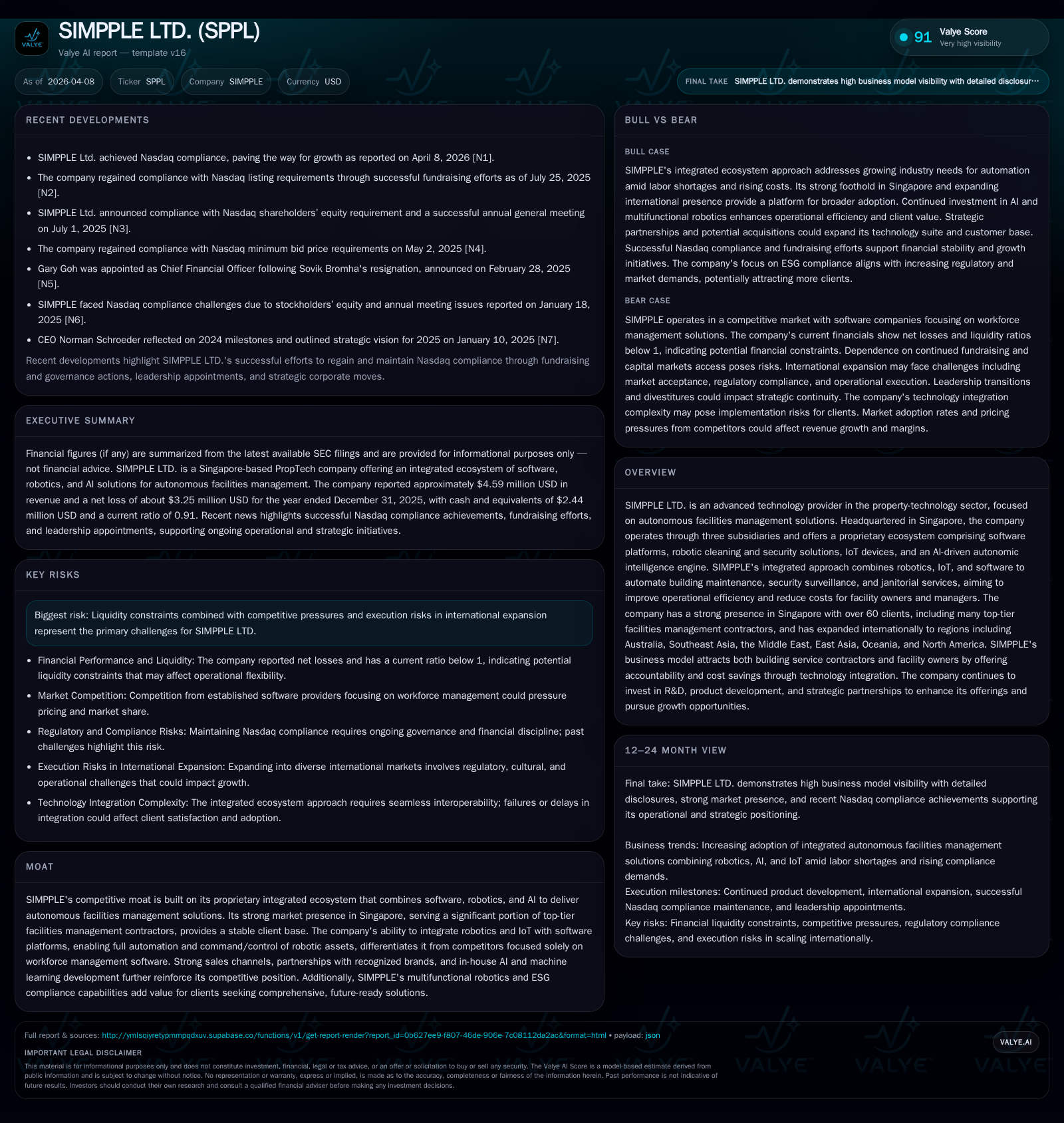

SIMPPLE LTD., headquartered in Singapore, has distinguished itself in the property-technology sector by seamlessly integrating autonomous robotics, IoT devices, and AI into an end-to-end facilities management ecosystem. Over recent years, the company achieved a striking revenue jump of 66.3% in 2025, propelled by increased adoption of its multi-functional robotic cleaning solutions and software services in Singapore and abroad. However, this top-line momentum belies ongoing operating losses exceeding $2.8 million USD and negative operating cash flow, underscoring challenges tied to scale-up costs, inflationary pressures, and international expansion. Liquidity constraints remain acute despite recent capital raises and cost rationalization efforts. Strategic partnerships and geographic diversification form the cornerstone of SIMPPLE's growth outlook amid competitive pressures and evolving compliance demands.

Historical Revenue Surge Countered by Persistent Operating Losses

SIMPPLE LTD.'s financial history over the last few years portrays a narrative of robust top-line growth shadowed by persistent losses that illuminate its early-growth-phase challenges. The company's annual revenue swelled from roughly $2.76 million USD in FY2024 to about $4.59 million USD in FY2025 — a remarkable 66.3% increase propelled largely by expanded sales of its multi-purpose robotic cleaning equipment alongside software service uptakes within Singapore and newly penetrated overseas markets [F1].

Yet this rapid scale-up comes at a cost: operating income remains firmly negative at around -$2.89 million USD for FY2025 even as it marks some improvement from a -$3.24 million USD loss in FY2024 [F1]. Net losses deepened slightly to nearly -$3.25 million USD for FY2025 as investments into research & development (R&D) and operating expenses step up aggressively to support the evolving technology portfolio and international ambitions [F1].

Importantly, operating cash flow deteriorated further from -$845K USD in FY2024 to -$1.41M USD in FY2025 reflecting ongoing capital deployment and working capital absorption during market expansion phases [F1]. This includes capex skyrocketing from a modest $11.6K USD in FY2024 to $437K USD (a 3653% increase), indicating substantial hardware investments primarily into its autonomous robotics platforms [F1][S7]. Such capital intensity underscores the company's aggressive growth strategy which prioritizes integrated robotics-software ecosystems over pure software solutions common among competitors.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5 | -3 | -1405644 | -3 | +66.3% | -13.1% |

| 2024 | 3 | -3 | -845470 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -1842473 | -121.9 |

| 2024 | -857109 | -160.8 |

Source: SEC companyfacts cache [F1].

Revenue/Income/Cash Flow figures converted from SGD where necessary per [F1].

Root Causes: Inflation, Tech Innovation Costs, and Market Adoption Dynamics

Analysis of SEC disclosures reveals that inflation exerts tangible upward pressure across SIMPPLE’s cost structure — from raw materials crucial for robotic manufacturing to labor wages impacted heavily by Singapore’s progressive minimum wage policies [S1][S6]. The company faces increased expenses due to mandated compliance requirements including data security protocols and professional fees associated with public company operations.

R&D investment has expanded significantly to fuel product innovation supporting the integrated ecosystem that combines AI-driven autonomic engines with IoT sensor networks for proactive facilities management solutions [S7]. The company emphasizes operating leverage effects wherein upfront fixed costs related to development are absorbed early before scale economies emerge with customer base growth internationally.

Despite these cost headwinds, industry adoption trends remain favorable due to structural labor shortages globally; aging workforce dynamics create demand incentivizing automation adoption within facilities sectors seeking efficiency gains amidst rising labor costs [S1][S18]. Government grants available primarily in Singapore provide helpful stimuli creating affordability pathways for technology uptake at grassroots customer levels.

Growth Outlook: Global Expansion and Strategic Partnerships Shape Future Trajectory

SIMPPLE’s ambition extends beyond its strong home base in Singapore — it actively pursues international footprint expansion leveraging subsidiaries such as SIMPPLE Australia Pty Ltd launched in late 2023 alongside channel partnerships spanning Southeast Asia (Malaysia, Thailand), East Asia (Hong Kong, Japan), the Middle East (Qatar), Oceania (New Zealand), Europe (Denmark), Canada, and the United States [N1][S14]. These alliances enable faster entry into diverse regulatory environments by partnering with local technology integrators or robot distributors familiar with their specific markets.

Strategic collaborations bolster cross-selling opportunities through recognized distributor networks facilitating adoption of multi-product ecosystem solutions rather than isolated tech components [S15]. This mix strengthens barrier-to-entry defensibility compared to software-only competitors reliant on workforce management tools.

Plans include development of next-generation SIMPPLE Software tailored for intricate enterprise-level workflows featuring enhanced data security architectures aiming at scalability across massive operations involving complex facility assets worldwide [S20].

Operational Headwinds: Navigating Labor Costs, Compliance, and Competitive Pressures

Labor-related operational challenges represent more than just cost inputs: SIMPPLE contends with regional labor shortages amplifying wage inflation pressures especially against Singapore’s incremental minimum wage policies influencing service contractor costs deeply tied into their customer base economics [S1][S26]. This dynamic complicates contract pricing models although simultaneously drives demand for automation mitigating future labor dependence.

Compounding this are rising compliance burdens—intensified reporting obligations across jurisdictions escalate administrative overheads alongside amplified cybersecurity governance demands designed to protect interconnected IoT devices controlling robotic assets remotely within buildings—a notable operational risk area overseen directly via board committees specialized on audit and cybersecurity oversight functions established recently [N1][S26].

Financial Health Check: Liquidity Status, Capital Structure, and Debt Obligations

Liquidity constraints constitute one of SIMPPLE’s most pressing challenges at present. As of December 31st, 2025 total current assets stood near $5.09 million USD against current liabilities totaling approximately $5.6 million USD yielding a sub-1 current ratio right at about 0.91x — signaling tight short-term liquidity conditions requiring judicious asset-liability management [F1][S4][S12].

Interest expenses spiked sharply mainly due to increased dependence on short-term borrowings from non-bank private lenders charging relatively higher rates versus traditional institutions—interest on short-term debt surged over thirteenfold reaching approximately S$502K SGD (~$390K USD) for FY2025 elevating finance costs notably over prior periods [S4].

In response management completed several equity raises including private placements totaling near $4.1 million USD combined during mid to late 2025 enhancing cash reserves alongside divesture of unprofitable Australian subsidiary early 2026 reducing continuing financial drag sources and elevating prospects for breakeven trajectory improvements going forward [S11][S19].

Capital Deployment Analysis: R&D Investments versus Returns and Cash Flow Trends

Capital allocation prioritizes iterative advancement of the integrated robotics/AI ecosystem encompassing new hardware platforms alongside software feature enhancements ensuring seamless interoperation amongst sensors, command/control devices and cloud analytics modules within the SIMPPLE Ecosystem architecture [S7][S8].

This up-weighting of capex has created significant cash flow pressure reflected in ballooning capex spending from just under $12K USD in FY24 to nearly half a million dollars in FY25 representing a capital intensity leap indicative of growth-stage software-hardware convergence businesses focused on platform build-out prior to scale profitability realizations [F1][S7].

However ongoing negative operating cash flows highlight risks related to scaling fixed costs rapidly while waiting for volume-driven margin benefits derived from accelerating enterprise-level customers adopting autonomous facilities management solutions internationally.

Governance Enhancements Bolstering Oversight During Growth Phase

A recent governance milestone involves appointing Mr. Ho Hin Yip — an independent director with extensive background as financial controller and senior executive across multiple Hong Kong Exchange-listed entities — to chair the Nominating & Corporate Governance Committee besides serving on audit and compensation committees effective April 2026 enhancing board-level expertise particularly around financial controls amid rapid growth stage complexities facing SIMPPLE [N1][S2].

The audit committee oversees cybersecurity risk management reflecting critical importance as reliance upon remote robotic systems grows across distributed geographies requiring robust IT infrastructure safeguards aligned with advanced data protection regulatory frameworks increasingly prevalent globally.

Key Benchmarks and Upcoming Milestones for Investors

Looking forward beyond historical results tracked herein, key metrics warrant monitoring include narrowing operating losses signifying improving cost structures coupled with operating cash flow stabilization reflecting better working capital efficiency amid maturing sales pipelines domestically plus internationally.

Developments regarding closing strategic partnership agreements facilitating faster overseas market penetration alongside successful bid conversions on large tenders requiring longer lead times underscore capacity building phases crucial before realizing contributory profits at scale [N1][S1].

The evolution of SIMPPLE's AI-powered autonomic intelligence engine combined with expanded hardware product offerings serves as another bellwether tracking innovation commercialization success possibly unlocking differentiated competitive advantages that distinguish it clearly from traditional facilities management software peers focusing narrowly on workforce optimization without integrated robotic command/control capabilities.

Disclaimer: This report is prepared solely for informational purposes based on publicly available sources provided herein including SEC filings ([F1], [S#]) and Nasdaq news ([N#]). It does not constitute investment advice or recommendations nor an offer or solicitation for any securities or investment products.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments