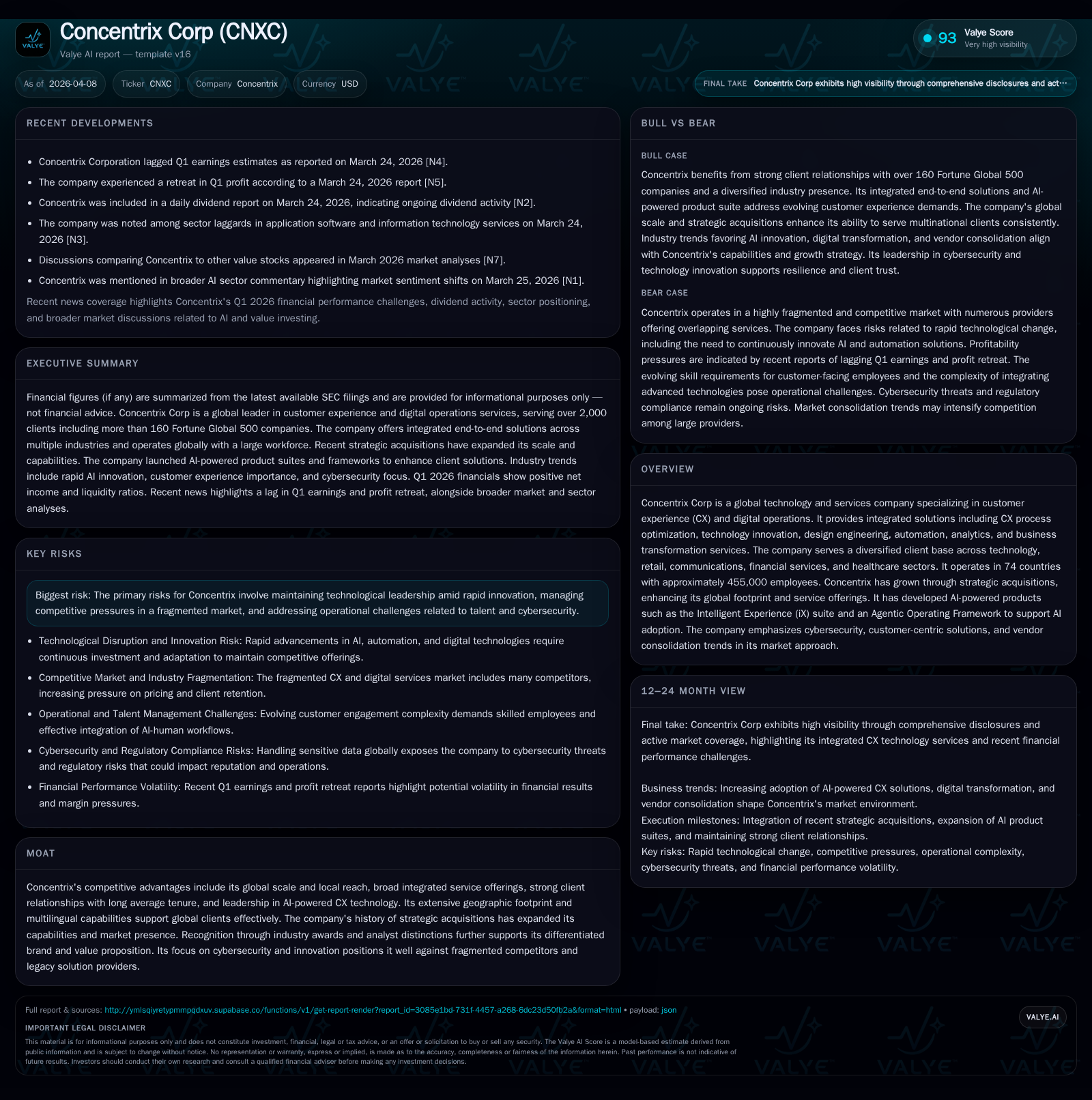

Concentrix’s Earnings Volatility and Strategic Shifts Challenge Growth Prospects

Concentrix confronts recent steep earnings declines while investing heavily in AI-driven customer experience innovations amid complex operational risks.

Concentrix Corp, a global leader in customer experience and digital operations, experienced a sharp decline in profitability in fiscal 2025 despite rising operating cash flow, driven by challenging macroeconomic conditions and integration costs. The company pursues growth through strategic acquisitions and advanced AI-powered CX technology platforms like its iX suite and Agentic Operating Framework. Operational risks including cybersecurity vulnerabilities exacerbated by AI use and workforce management challenges remain significant. While the company maintains a diversified, long-tenured client base across multiple verticals, its returns on equity have turned negative, raising questions about capital efficiency. Monitoring margin recovery and AI adoption rates will be crucial to assessing Concentrix’s trajectory amid an evolving, fragmented industry landscape.

Historic Performance and the Profitability Downturn of FY2025

Concentrix’s 2025 fiscal year underscored a stark departure from its prior stable profitability trajectory. The company reported an operating loss of approximately $918 million, representing a precipitous 254% year-over-year decrease from the $596 million profit in FY2024 [F1]. Net income plunged even more dramatically to a loss of roughly $1.28 billion, down over 609% from the prior year's $251 million net income. This disconnect between cash flow strength and accounting performance highlights nuances impacting reported earnings figures.

Notably, operating cash flow rose by nearly 21% year-over-year to about $807 million, emphasizing that core business operations continued to generate substantial liquidity despite steep inked losses [F1]. This uptick suggests effective cash conversion cycle management amid the earnings setbacks. Capital expenditures remained relatively flat at just under $235 million (-1.8% YoY), indicating consistent reinvestment levels aligned with ongoing technology deployments.

The sharp deterioration in profitability primarily reflects non-cash charges related to acquisition integration costs, restructuring expenses tied to strategic shifts towards AI deployments, and macro-driven demand softness affecting client forecasting accuracy as detailed in risk disclosures [S1]. These swings underscore sector-wide volatility where short-term earnings can diverge sharply from underlying operational health.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1279 | 807 | -918 | 234 | -609.1% |

| 2024 | 251 | 667 | 596 | 239 | -20.0% |

| 2023 | 314 | 678 | 661 | 181 | -27.9% |

| 2022 | 435 | 601 | 640 | 140 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 90 | 169 | 572 |

| 2024 | 84 | 136 | 429 |

| 2023 | 63 | 64 | 497 |

| 2022 | 53 | 121 | 461 |

Source: SEC companyfacts cache [F1].

Strategic Drivers: Acquisitions and AI Innovations Fueling Growth

Growth for Concentrix continues to hinge on both inorganic expansion and technology-led service differentiation. The company operates in 74 countries with approximately 455,000 employees as of late 2025 [S1].

Its growth strategy features targeted acquisitions that deepen geographic reach and vertical-specific expertise—a classic approach in services markets enabling rapid scale-up while broadening solution portfolios. These efforts dovetail with heavy investments in cutting-edge CX technologies designed to stem commoditization pressures within outsourced customer experience sectors.

Central to this strategy is the Intelligent Experience (iX) suite—a platform blending generative AI (GenAI), agentic AI-powered self-service tools, automation capabilities, and analytics intended for seamless CX process optimization. Complementing this is the Agentic Operating Framework that facilitates clients’ adoption of emerging AI modalities across front- and back-office digital operations [S1]. This integrated architecture seeks not only to enhance efficiency but to enable richer customer lifecycle value creation through data-driven insights and proactive engagement models.

This dual focus on acquisitions plus agentic AI innovation aims to build a technological moat against legacy providers who lack integrated AI readiness as well as against fragmented niche operators.

Operational Risks: Cybersecurity and Talent Management Pressures

While deployable AI technologies present growth avenues, they also introduce expanded ransomware attack surfaces and sophisticated cybersecurity threats. Concentrix explicitly calls out increased susceptibility due to the intertwining of internal networks with client systems coupled with the operational complexity of managing large volumes of sensitive personal data across diverse global jurisdictions [S1].

Cybercriminal activities—ranging from phishing campaigns to malware designed for social engineering—pose material risk vectors that could disrupt service continuity or trigger liability exposures under strict client confidentiality contracts.

From a talent perspective, sustaining workforce optimization amidst ongoing digital transformation places strain on recruiting skilled employees proficient not only in traditional CX disciplines but increasingly in data science, machine learning model governance, and cybersecurity protocols [S2]. Maintaining morale and retention within highly competitive labor markets further complicates operational stability.

Visible within risk filings is language around managing 'attack surfaces' created by new technology adoption alongside balancing resource allocations for upskilling staff—a dual challenge reflecting broader industry talent wars amplified by cybersecurity imperatives.

Client Concentration and Vertical Market Focus as Competitive Anchors

Concentrix serves more than 160 Fortune Global 500 companies spanning five primary verticals including technology, fintech, retail/e-commerce, communications/media, banking/insurance, and healthcare [S1]. The client base features sticky contract structures evidenced by top-30 client tenures averaging an impressive 16 years.

Such longevity reflects strong relational embeddedness generating consistent downstream revenue streams while mitigating churn risks typical in outsourcing arrangements. Moreover, vertical diversification cushions exposure to cyclical shocks concentrated within any single industry segment.

For example, Concentrix’s penetration among top-tier clients—8 of the top 10 global tech companies plus multiple leading financial institutions globally—grants it access to large-scale wallet share opportunities via expanding end-to-end digital transformation mandates [S1]. This enhances its ability to upsell new products like the iX platform offering across multiple lifecycle touchpoints.

Extensive multilingual capabilities paired with localized delivery further amplify competitive positioning by serving regionally nuanced customer expectations for large multinational clients.

Capital Deployment: Improving Cash Flow Amid Declining Returns on Equity

Despite accounting losses weighing on net income during FY2025 ($-1.28 billion net loss vs $2.74 billion equity at year-end), Concentrix generated free cash flow approximating $572 million (operating cash flow minus capex) sustaining healthy liquidity dynamics [F1].

Capital allocation decisions reflect prudence; dividends paid rose modestly to roughly $90 million while share repurchases accelerated reaching nearly $169 million in buybacks—a scale increase signaling management confidence in intrinsic value amidst volatile earnings [F1].

However, return on equity has swung dramatically negative (~-46.6%), spotlighting accounting profit erosion that challenges capital efficiency narratives [F1]. This disparity between robust CFO measures versus reported ROE reinforces nuances needed when interpreting performance metrics during periods of heavy restructuring investment.

The combination suggests that shareholder returns rely heavily on upcoming margin recovery and sustained cash generation rather than near-term profitability metrics alone.

Investor Considerations: Upcoming Milestones and Financial Metrics to Monitor

Current disclosure offers limited explicit forward guidance; thus investors should prioritize tracking dynamic KPIs such as rollout velocity for iX-related solutions across existing clients plus new accounts secured leveraging agentic AI capabilities [N1][N10].

Margins will be critical bellwethers given their compression impact during FY2025 setbacks. Likewise, monitoring client retention statistics within top verticals provides early visibility into potential lifecycle revenue sustainability amidst competitive pressures.

Market sentiment flagged by Q1/26 earnings lag relative to estimates likewise underscores volatility requiring a calibrated lens when evaluating quarterly outcomes against longer-term innovation-driven strategies [N1].

Emerging ‘customer experience transformation KPIs’ encompassing multichannel engagement success rates may provide leading insights into effectiveness of Concentrix’s integrated CX process optimization initiatives [N10].

The Future Outlook: Navigating Market Fragmentation and Technological Change

Looking ahead, Concentrix faces a bifurcated landscape characterized by accelerating platform consolidation among outsourcers contrasted with intensifying competition from niche CX tech firms exploiting specialized domains [S1][N7]. Its broad integrated service model paired with AI-powered service frameworks positions it favorably amidst these platform dynamics.

However, risks remain substantial given geopolitical uncertainties affecting cross-border workflows alongside rapid evolution of artificial intelligence demanding continuous reinvestment in innovation pipelines to uphold technological leadership.

Success depends on balancing ongoing cybersecurity risk mitigation against workforce skill enhancement efforts while capturing market share gains through differentiated CX offerings designed for discerning enterprise clients demanding measurable economic outcomes.

In sum, Concentrix embodies a complex interplay between steep recent earnings volatility offset by strategic shifts toward emergent agentic AI technologies poised to reshape customer lifecycle value creation across diverse industries worldwide.

This analysis is based solely upon publicly available information as of April 8, 2026; it contains no investment recommendations but aims to provide a detailed assessment of Concentrix Corp’s financial performance, strategic initiatives, risks, capital management practices, and outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments