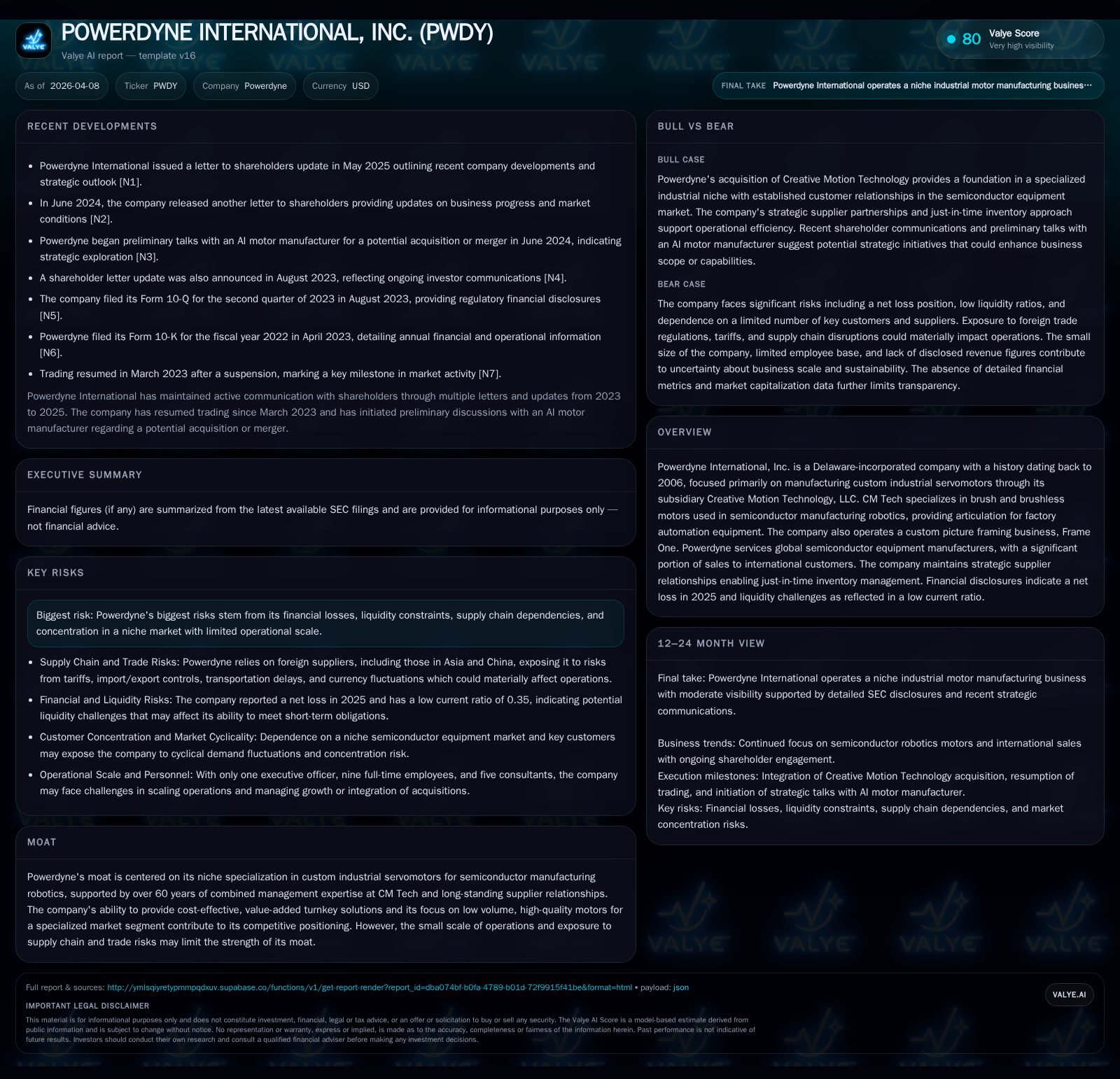

Powerdyne International’s Struggle for Stability in Custom Servomotors

Powerdyne International specializes in custom industrial servomotors for semiconductor robotics yet contends with sustained financial losses and liquidity constraints shaping its growth outlook.

Powerdyne International, through its subsidiary Creative Motion Technology (CM Tech), operates in a highly specialized niche of brush and brushless industrial servomotors focused on semiconductor manufacturing robotics. Despite over 60 years of combined management expertise and strategic supplier relationships enabling just-in-time operations, the company has encountered persistent operating losses and weak liquidity as of fiscal 2025. Revenue has declined significantly in recent years, while operating cash flow remains under pressure, highlighting challenges in scaling profitability. Future growth hinges on semiconductor industry demand and technological advancements but is tempered by supply chain dependencies, capital access constraints, and a concentrated customer base.

From Modest Revenues to Sustained Losses: Historical Financial Trajectory

Powerdyne International’s financial trajectory exhibits clear signs of operational stress marked by declining revenues and escalating losses over the last decade. The company reported revenues of $752 thousand in FY2015 which shrank to $488 thousand by FY2016, representing a significant contraction within a single year [F1]. While more recent annual revenue figures are unavailable, the downward trend up to 2016 underscores limited scale.

Operating income deteriorated substantially into negative territory over subsequent years. By FY2022, the company reported an operating loss of approximately $1.34 million—an order of magnitude greater than losses seen earlier in the decade (e.g., -$165.7K in FY2016) [F1]. This steep decline signals rising fixed costs or inefficiencies that the shrinking topline could no longer absorb.

Net income figures remained negative through FY2025 with a recorded net loss of nearly $19.8 thousand—the smallest annual deficit recorded in recent years though still reflective of sustained unprofitability [F1]. Operating cash flow mirrored this pattern with consistent outflows; FY2025 saw an outflow of about $192 thousand despite a slight sequential improvement over prior periods such as FY2024’s -$203K [F1]. Capital expenditures appear modest relative to cash consumption, indicating constrained reinvestment capacity.

Historical performance (annual)

| FY | Net ($) | CFO ($) | Net YoY |

|---|---|---|---|

| 2025 | -19808 | -192005 | +58.5% |

| 2024 | -47720 | -203925 | +43.3% |

| 2023 | -84173 | 35042 | +93.7% |

| 2022 | -1342016 | -44273 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 3.9 |

| 2024 | 18.8 |

| 2023 | 113.7 |

| 2022 | -120252.3 |

Source: SEC companyfacts cache [F1].

Note: Some year-over-year percentages are not computable due to missing prior year data; all figures USD except percentages.

The Semiconductor Robotics Motor Niche: Powerdyne’s Specialized Role

Powerdyne’s core business is centered on providing custom-designed industrial servomotors specializing primarily in brush and brushless variants tailored for semiconductor manufacturing robotics applications under its CM Tech subsidiary [S1]. These motors typically serve critical articulation axes—X, Y, and Z—in factory automation equipment tasked with delicate semiconductor wafer processing tasks.

The niche nature of this market segment demands motors engineered for low volume but high quality with strict tolerances and reliability requirements aligned with original equipment manufacturers (OEMs) servicing semiconductor fabs globally [N1][S1]. This specialization presents an embedded competitive moat grounded on decades of engineering expertise (over six decades combined among CM Tech’s leadership team) and long-standing supplier relationships that support just-in-time inventory models crucial to factory uptime.

However, the narrow focus also channels concentration risk both in revenue streams from limited OEM partners and raw material procurement dependencies—factors explicitly noted as risk drivers in company disclosures with significance placed on maintaining component availability amid global supply chain disruptions.[S1]

Liquidity Challenges and Capital Structure Under Pressure

A critical operational challenge facing Powerdyne is its stark liquidity constraints reflected by a current ratio approximating 0.35 as per fiscal year-end 2025 data [F1]. This level starkly underscores the gap between current assets ($273K) relative to current liabilities ($779K), implying insufficient short-term resources to cover immediate obligations without external financing or asset sales.

The low current ratio raises concerns regarding Powerdyne's ability to sustain its tightly coordinated just-in-time supplier framework necessary for complex servomotor components which often require precise timing for assembly schedules within OEM production lines.[N1][S1] Such tight liquidity also restricts flexibility to invest in growth opportunities or buffer market shocks arising from cyclic semiconductor capital expenditure patterns.

Furthermore, financing capital expenditures remains constrained given the negative free cash flows evidenced by persistent operating cash flow deficits offset only minimally by comparatively low capital spending initiatives — as indicated by lower capex relative to operating cash burns across recent periods.[F1]

Assessing the Acquisition of Creative Motion Technology and Synergies

In March 2022, Powerdyne acquired full control of Creative Motion Technology LLC through issuing two million shares of Series A Preferred Stock valued at approximately $1.5 million [S1]. Importantly, these preferred shares carry enhanced voting rights — one thousand votes per share — affording holders dominant control within corporate governance structures.

This arrangement appears designed both to consolidate operational command post-acquisition and preserve the stewardship of key management personnel who collectively bring over sixty years of design and manufacturing expertise specifically within servomotor technology.[S1]

Alongside CM Tech’s core motor manufacturing business comes Frame One—a custom picture framing operation with an established regional client base unrelated to Powerdyne’s semiconductor motor focus but included within the broader acquisition portfolio.[S1] The primary strategic value lies rather in CM Tech’s niche product portfolio offering turnkey solutions catering directly to highly specialized OEM customers within semiconductor automation sectors.

Future Growth Drivers Amid Market and Supply Chain Risks

Looking forward, Powerdyne's growth prospects fundamentally tie back to demand trends within semiconductor manufacturing equipment where advances in chip fabrication drive requirements for increasingly sophisticated factory automation motors capable of higher precision and reliability.[S1]

Technological developments advancing brushless servomotor designs coupled with potential expansion into adjacent tool articulation needs may provide avenues for incremental revenue gains.[S1] Moreover, persistent industry focus on semiconductors amid global digital infrastructure expansions can underpin long-term OEM investment cycles benefiting suppliers like CM Tech.

Conversely, exposure to raw material sourcing disruptions—especially when tied to geopolitical tensions impacting trade—and reliance on concentrated customers amplify downside risks.[S1] Economic downturns that impact end-market capital spending may curtail order volumes sharply given Powerdyne's smaller scale manufacturing footprint limiting economies compared with larger competitors.[S1]

Financial Performance Forecasts and Milestones to Watch

Currently absent explicit management guidance or forecast disclosures,[S1][S2] monitoring discrete developments becomes essential. Key indicators would include:

- Improvement in liquidity ratios signaling easing cash constraints;

- Margin rebound evidencing better absorption of fixed costs;

- Announcements of new OEM contract awards or expansions;

- Operational metrics reflecting production output scaling;

- Progress integrating components or cost synergies post-CM Tech acquisition. These would serve as tangible markers against otherwise enduring cyclical headwinds affecting niche motor suppliers.

Capital Allocation Strategy: ROE, Cash Flow, Dividends, and Shareholder Returns

Capital deployment discipline appears limited given Powerdyne's financial profile. The latest calculated return on equity stands at approximately 3.9%, reflecting marginal profitability amidst negative equity worth near -$505 thousand as of FY2025 end [F1].

Operating cash flow remains persistently negative (-$192 thousand) while capex spending is modestly scaled back—resulting in free cash flow deficits exceeding $200 thousand annually [F1]. No dividends have been declared nor share repurchase programs initiated likely stemming from ongoing net losses constraining distributable reserves.[F1]

This situation underscores an inability currently to generate shareholder returns beyond operational sustenance with significant emphasis needed on turning around core profitability before capital returns strategies could be revisited.

Operational Scale Limits and Moat Sustainability Concerns

While Powerdyne benefits from entrenched engineering know-how and long-term supplier ties specific to high-quality customized servomotors,[N1][S1] its limited operational scale poses substantial challenges. Small batch production dynamics increase per-unit costs compared to OEM competitors leveraging greater volume throughput or diversified product portfolios.[N1] Additionally, the continual evolution required in technology design places further strain on R&D resource allocation that might be tougher for smaller entities without extensive balance sheet backing. Further complicating sustainability is susceptibility to international trade restrictions disrupting foreign customer contracts central to revenue generation given significant overseas OEM sales exposure mentioned broadly.[S1] Collectively these macro risks constrain the underlying moat strength despite power accruing from managerial experience and niche specialization.

Disclaimer: This analysis is based solely on provided SEC filings ([S#]), numerical data ([F#]), and proprietary company information without conjecture or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments