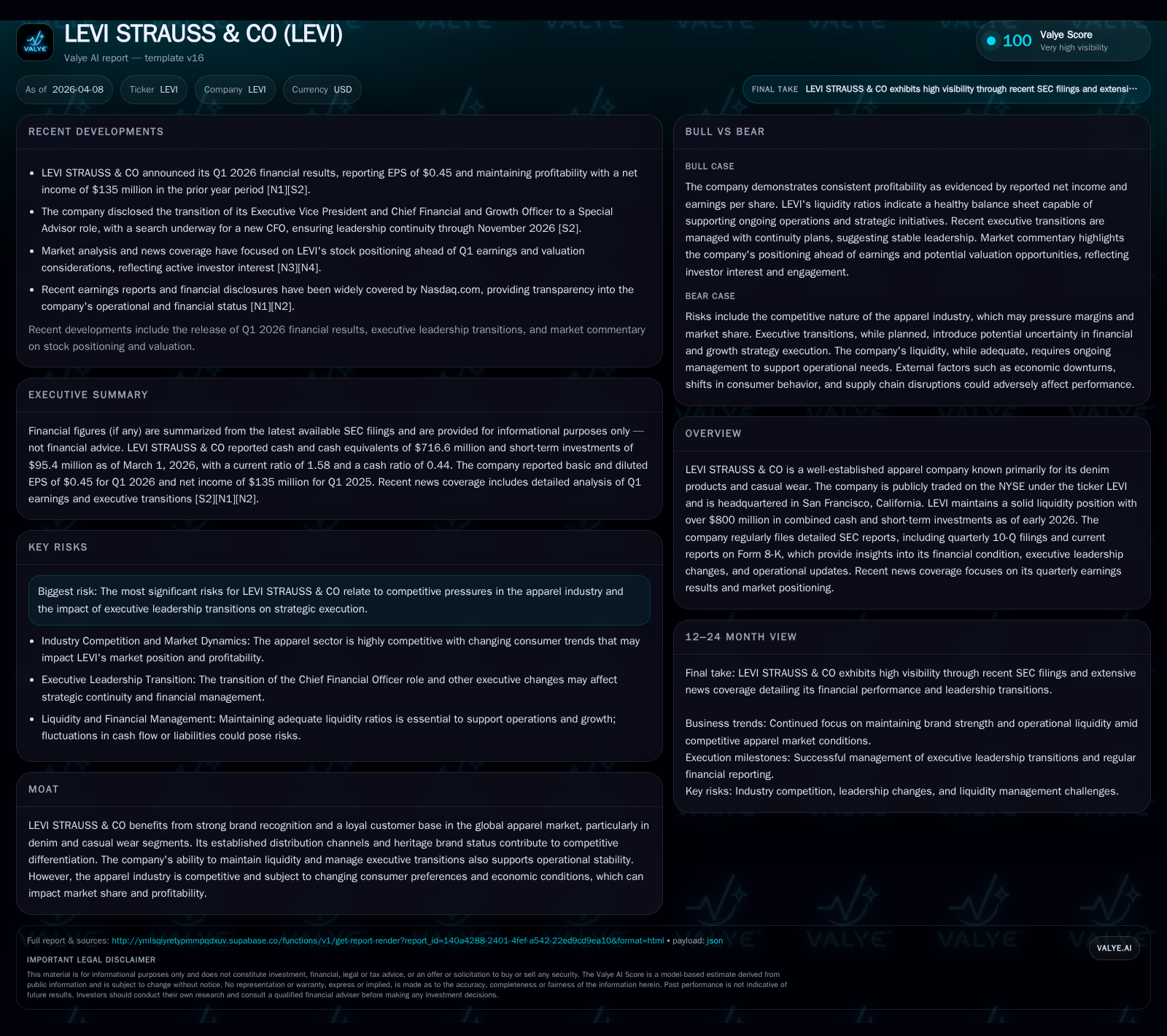

Levi Strauss & Co: Revenue Rebounds While Margins Expand in 2025

Levi Strauss delivered a notable financial turnaround in fiscal 2025, driven by revenue growth and operating leverage, alongside strategic leadership transitions and disciplined capital allocation.

Fiscal year 2025 marked a strong rebound for Levi Strauss & Co., with an 8.6% revenue increase complemented by a 156.6% surge in operating income versus the prior year, underscoring operational efficiencies and margin expansion. Despite improved operating results, net income declined 15.6%, reflecting challenges below the operating line including elevated non-operating expenses or tax impacts. Operating cash flow fell by over 40%, indicating working capital pressures. The company maintained consistent dividend payments while sharply reducing share repurchases, preserving liquidity above $700 million as of Q1 2026. Leadership changes at the Board and CFO level signal a strategic inflection point amid evolving growth priorities and competitive apparel market dynamics.

Financial Performance Highlights: Revenue and Profitability

Levi Strauss & Co demonstrated robust revenue growth in fiscal year 2025, with total revenue reaching $1.59 billion, up 8.6% from the prior year’s $1.47 billion [F1]. This rebound reflects stronger consumer demand for core products and effective channel management.

Operating income experienced a substantial increase of 156.6%, rising to $678 million from $264 million in fiscal 2024 [F1]. This surge was driven by operating leverage benefits, improved gross margins through pricing power, product mix optimization, and cost discipline across the supply chain.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 530 | 678 | 221 | ||

| 2024 | 211 | 898 | 264 | 228 | -15.6% |

| 2023 | 250 | 436 | 353 | 316 | -56.1% |

| 2022 | 569 | 228 | 647 | 267 | +2.8% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 213 | 31 | 308 |

| 2024 | 199 | 90 | 671 |

| 2023 | 191 | 8 | 120 |

| 2022 | 174 | 176 | -39 |

Source: SEC companyfacts cache [F1].

Note: Net income for FY2025 is not finalized; the latest available figure is for FY2024 as of December.

Profitability and Cash Flow Dynamics

Despite strong operating performance, net income declined by approximately 15.6%, falling from $249.6 million in FY2023 to $210.6 million as of December 2024 [F1]. This divergence suggests increased non-operating expenses or tax impacts highlighted in recent filings [S2][N1].

Operating cash flow contracted sharply by over 40% to approximately $530 million in FY2025, down from $898 million in FY2024 [F1]. This reduction indicates working capital buildup or timing differences between earnings recognition and cash movements—a typical pattern in retail inventory cycles.

Capital expenditures remained relatively stable at $221 million for FY2025 compared to $228 million the prior year, reflecting ongoing investments balanced with operational cash generation needs [F1].

Capital Allocation: Dividends, Buybacks, and Liquidity

Levi Strauss maintained a consistent dividend payout of approximately $213 million during FY2025, demonstrating commitment to shareholder returns despite earnings fluctuations [F1][S14]. In contrast, share repurchases were significantly reduced to about $30.5 million from higher levels in previous years, signaling a cautious approach focused on preserving liquidity amid market uncertainties [F1][S22].

Cash and equivalents stood at $716.6 million as of March 2026, providing a strong liquidity buffer for strategic flexibility [F1][S8].

Return on equity based on available net income and shareholders’ equity approximates around 9.2%, indicating moderate capital efficiency given profit pressures [F1].

Leadership Transitions and Strategic Outlook

Significant leadership changes include the appointment of Jeffrey J. Jones II as an independent director bringing retail marketing expertise to the Board effective January 21, 2026 [S14][S15]. Concurrently, Executive Vice President and CFO Harmit Singh announced his planned transition to a Special Advisor role through November 30, 2026, ensuring continuity during the CFO search process [S20][S21].

These developments occur against a backdrop of competitive pressure from fast fashion players and evolving consumer preferences toward sustainability and digital commerce channels [N3][S20]. Management emphasizes digital growth initiatives and selective geographic expansion while acknowledging risks such as supply chain disruptions detailed in risk factors disclosures.

Risks and Market Dynamics

Levi Strauss faces ongoing challenges including intense competition within the apparel sector, rapid fashion cycles requiring agility, and supply chain complexities exacerbated by geopolitical uncertainties [S4][S20]. Executive transitions add execution risk but also provide opportunities for strategic refreshment.

Conclusion: Monitoring Key Metrics Ahead

Investors should monitor upcoming quarterly earnings reports focusing on revenue trends including same-store sales growth, gross margin stability reflecting pricing power against cost inflation, operating cash flow quality amid working capital fluctuations, and progress on leadership succession plans.

This analysis is based on publicly available SEC filings through early April 2026 and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments