Jefferies Financial Group’s Strategic Momentum Amid Investment Banking Growth

Jefferies leverages robust liquidity and capital markets access to sustain investment banking growth, while navigating competitive and regulatory pressures.

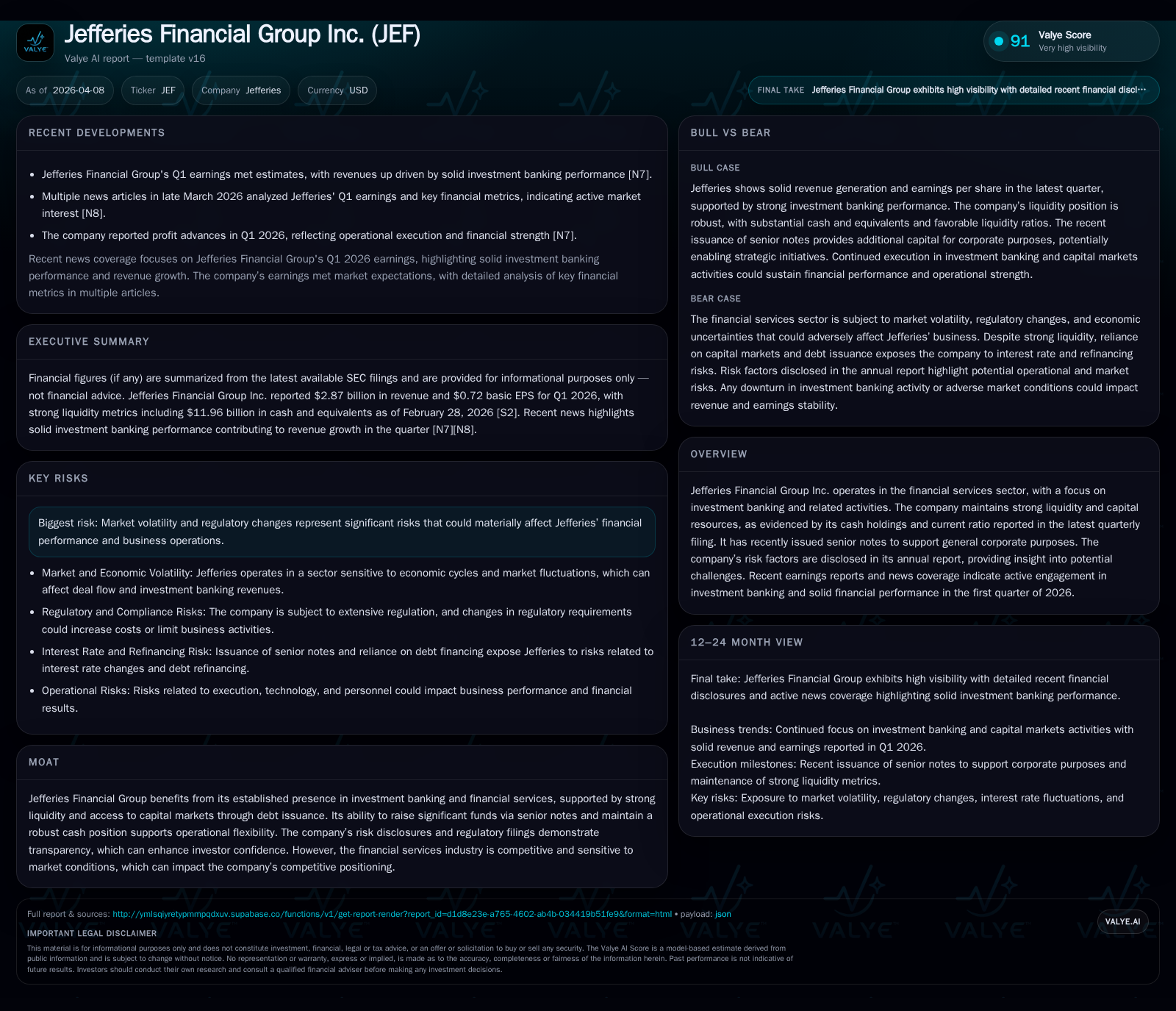

Jefferies Financial Group Inc. has demonstrated solid revenue growth and improved profitability through FY2025, driven primarily by momentum in its investment banking and capital markets businesses. The company's liquidity position remains strong, supported by significant cash reserves and recent senior notes issuances that enhance financial flexibility. Despite ongoing risks from market volatility and regulatory scrutiny, Jefferies continues to execute its integrated client service strategy, with 2026 Q1 earnings aligning with market expectations. Investors should monitor underwriting pipelines, legal developments, and capital allocation choices as key indicators of forward performance.

Evolution of Revenue and Profitability: Growth Drivers Through Recent Years

Jefferies Financial Group's top line has exhibited steady expansion over recent years, with FY2025 revenue reaching $10.82 billion from $10.52 billion in FY2024, marking a 2.9% increase year-over-year [F1]. This topline growth accompanies a pronounced profitability surge; while the latest reported net income is from FY2021 at $1.67 billion [F1], historical trends indicate operational leverage is a key feature of Jefferies’ model.

Operating cash flow (CFO) turned negative starting FY2023 (-$1.93 billion), reversing prior positive trends observed in FY2021 ($1.57 billion) and FY2022 ($1.80 billion) [F1]. Combined with capital expenditures around $207 million in FY2025 (a moderate decline from prior years), these dynamics resulted in a free cash flow deficit estimated near -$2.14 billion last fiscal year—reflecting working capital changes or balance sheet funding typical for investment banks managing inventory positions [F1]. Dividend payments remained stable at approximately $374 million in FY2025 underscoring management's commitment to shareholder returns despite cyclical liquidity pressures.

Historical performance (annual)

| FY | Rev ($bn) | CFO ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|

| 2025 | 10.8 | 207 | +2.9% | |

| 2024 | 10.5 | 251 | +41.3% | |

| 2023 | 7.4 | -1934 | 1 | +4.1% |

| 2022 | 7.1 | 1805 | 224 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 374 | 59 | |

| 2024 | 303 | 44 | |

| 2023 | 279 | 169 | -1935 |

| 2022 | 280 | 860 | 1581 |

Source: SEC companyfacts cache [F1].

*Operating cash flow figures indicate variability tied to market conditions impacting working capital.

Investment Banking and Asset Management: Core Business Segment Dynamics

Jefferies operates primarily through two segments: Investment Banking and Capital Markets, alongside Asset Management platforms focused on credit and alternatives [S1]. The firm’s strategy centers on growing underwriting syndications across equity and fixed income products coupled with advisory services across M&A and restructuring sectors globally.

Recent quarterly results underscore positive traction within investment banking revenues supporting Q1 2026 performance aligned with estimates [N1,N2]. The firm’s prime brokerage services enhance client retention among hedge funds, complemented by equity finance operations facilitating trading activities [S1]. This integrated platform supports diversified revenue streams critical amid evolving market cycles.

Capital Markets Activity: Liquidity Strength and Debt Issuance

Jefferies’ liquidity position remains robust with cash equivalents totaling approximately $12 billion as of February quarter end 2026 [F1], complemented by a current ratio close to 2.0 indicating strong short-term asset coverage relative to liabilities.

Capital structure management includes recent issuances of senior notes aggregating over $1.5 billion with maturities extending from 2027 through 2036 at coupon rates between roughly 2.75% and 6.20% [S3,S5]. These issuances reflect strategic debt refinancing efforts enhancing financial flexibility for general corporate purposes including working capital support.

Risk Profile: Market Volatility and Litigation Exposure

Credit risk arises from derivative transactions conducted on both customer and principal bases; daily collateral monitoring aims to mitigate counterparty default risk though residual exposures remain due to timing mismatches or collateral fluctuations [S1]. Principal trading exposes Jefferies to market risk through mark-to-market valuation changes on security inventories.

The company is engaged in ongoing litigation tied to a Ponzi scheme involving approximately $106 million misappropriated funds; Jefferies recognized a $17.2 million loss related to this investment with uncertain recovery prospects [S1,S4]. While not currently materially impacting consolidated results, this matter warrants investor attention.

Regulatory oversight remains intensive given Jefferies’ broker-dealer status; compliance frameworks include risk controls around liquidity oversight committees and internal stress testing designed to safeguard capital adequacy under adverse scenarios [S4].

Earnings Review: Q1 2026 Performance Aligned With Expectations

Jefferies reported Q1 earnings for the period ended February showing results consistent with consensus estimates driven by sustained strength in investment banking fees despite macroeconomic challenges [N1,N2,N3]. Market commentary highlights effective execution across underwriting deal flow and capital markets sales as key contributors.

Forward Outlook: Maintaining Momentum Amid Competition

Forward-looking statements emphasize preserving momentum in underwriting pipelines alongside expanding capital markets initiatives leveraging technology platforms especially within Asia-Pacific regions through partnerships such as SMBC’s planned Japan equities joint venture commencing January 2027 [N1,S2,S21].

Competitive dynamics remain intense among global investment banks requiring continued investments in advisory expertise and technological agility amidst cyclical headwinds.

Capital Allocation: Balancing Shareholder Returns With Reinvestment Needs

Despite negative free cash flow pressures mainly driven by operating cash outflows exceeding capex by significant margins in recent years [F1], Jefferies maintained steady dividend payments increasing modestly year-over-year to $374 million in FY2025 [F1,S22–S24].

Share repurchases have moderated substantially falling below $60 million last fiscal year compared to prior periods reflecting prudent liquidity management while preserving equity base above $10 billion as of fiscal year-end November [F1]. This approach balances shareholder returns alongside maintaining financial flexibility for organic growth or opportunistic investments.

Investor Considerations Beyond Financial Metrics

Investors should closely monitor developments related to ongoing litigation outcomes which may affect reserve levels or reputational considerations; sensitivity of earnings to market volatility impacting trading inventories; credit quality within lending platforms; and evolving regulatory frameworks potentially increasing compliance costs.

These qualitative factors complement quantitative analysis providing a comprehensive lens on Jefferies’ position within complex financial services environments characterized by operational interdependencies yet exposed to external shocks.

This analysis synthesizes information from SEC filings ([S#]), company financial data ([F1]), and news reports ([N#]) without constituting investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments