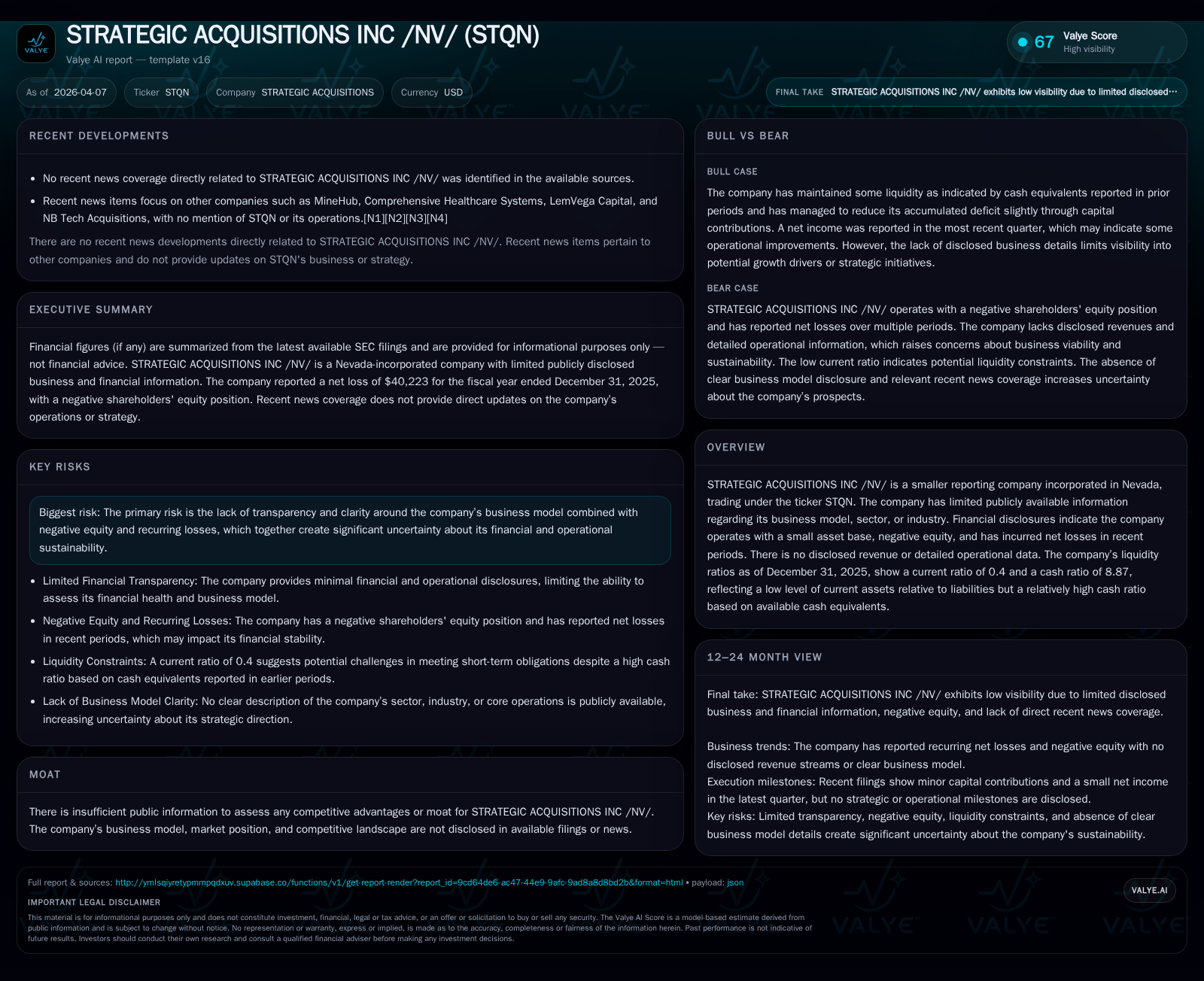

Strategic Acquisitions Inc’s Transition Through Digital Asset Lending Challenges

STQN shifted from a dormant shell to a digital asset-backed lender, facing persistent losses and operational hurdles amid early-stage fintech market realities.

STRATEGIC ACQUISITIONS INC /NV/ (STQN) evolved from a non-operating shell company into a niche digital asset collateralized loan provider via acquisition of Exworth Union in late 2022. Despite this strategic pivot, the company has struggled with ongoing operating losses and negative equity exacerbated by limited lending activity and the cessation of loan origination since mid-2024. Their early focus on Bitcoin-backed term loans targets small businesses and individuals but development delays in proprietary loan servicing technology due to funding shortages cloud near-term growth prospects. Financial reports highlight liquidity imbalances and auditor concerns that pose material risks to sustainability. Key turnaround milestones will hinge on resuming loan issuance, progressing platform development, and securing new financing.

From Shell to Lending: STQN’s Historical Growth Trajectory

STRATEGIC ACQUISITIONS INC /NV/ (STQN), originally incorporated in Nevada in 1989, functioned as a shell company without commercial operations until its December 22, 2022 reverse recapitalization merger with Exworth Union Inc. This acquisition transitioned STQN into the business of providing U.S. Dollar denominated loans secured by digital assets, primarily Bitcoin as collateral. Prior to this transaction, the company had nominal interest income but no operational revenues or substantive business activity [S1].

Post-merger financials reveal persistently negative operating income and net income figures; however, there has been measurable improvement over time. For example, operating income losses narrowed from -$136K in FY2022 to -$40K in FY2025 — an improvement exceeding 60% year-over-year between FY2024 and FY2025 [F1]. A similar trend is observed in net income: it shifted from a positive $249K in FY2022 (reflecting pre-merger adjustments or other nonrecurring items) into consistent annual losses exceeding $40K thereafter [F1]. Operating cash flows also remain negative but have improved substantially from nearly -$175K in FY2023 to approximately -$30K in FY2025 [F1], signaling ongoing operating inefficiencies tempered by reduced scale or cost-cutting.

These trends correspond directly with the company's strategic shift toward originating and servicing digital asset-backed loans after acquiring Exworth Union's niche lending expertise. The early years post-merger reflect formative stages marked by investment in infrastructure alongside nascent loan issuance activities.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -40223 | -30473 | -40223 | +67.7% |

| 2024 | -124714 | -110124 | -102149 | +23.1% |

| 2023 | -162260 | -175058 | -120603 | -165.3% |

| 2022 | 248672 | -133683 | -136371 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 507.2 |

| 2024 | 152.0 |

| 2023 | -380.1 |

| 2022 | 40.8 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary FY2022-FY2025 [F1]

Digital Asset-Backed Loan Market and STQN’s Business Model

STQN occupies an early-stage fintech sub-sector: digital asset-backed lending focused on small enterprises and individual borrowers possessing intangible crypto-assets primarily Bitcoins. Its model entails origination of term loans denominated in USD secured by such collateral—an approach reliant on efficient collateral valuation mechanisms and risk management tailored to volatile crypto markets.

As described in SEC filings, their target customer base includes those seeking liquidity against holdings of digital currencies without liquidating them outright — essentially monetizing appreciating assets [S1]. The dependence solely on Bitcoin as acceptable collateral constrains diversification but reflects focused risk appetite aligned with initial market penetration ambitions.

However, unlike larger fintech peers who have invested heavily to build proprietary platforms enabling seamless loan origination and collateral monitoring automation—which are essential for scaling—STQN has yet to initiate development of such technology given funding limitations encountered as recently as end-2025 [S1][S2]. The absence of this critical infrastructure places operational scalability challenges ahead.

Revenue Generation and Operational Setbacks in Recent Years

Post-merger revenue generation sources have principally stemmed from interest accruals on issued loans and associated fee income tied to loan origination events managed through Exworth Union’s services integrated under STQN’s control. Nevertheless, these revenues have failed to offset overhead costs.

Importantly, filings disclose a cessation of new loan issuances beginning July 2024 following borrower settlement of outstanding loans — effectively pausing primary revenue streams while the company reevaluates operations or pursues platform developments [S1]. This operational pause explains much of the suppressed revenue visibility coupled with ongoing operating losses.

This indicates short-term challenges in maintaining top-line growth without active lending volume or alternative fee-generating services.

Evaluating the Company’s Financial Sustainability and Risks

STQN presents considerable financial fragility underscored by repeated operating losses throughout its recent history despite some margin improvement efforts. The company's auditor has expressed substantial doubt on its ability to continue as a going concern due to insufficient cash flow generation from commercial operations and reliance on external financing to sustain activities [S1].

Compounding concerns is the permanent revocation of PCAOB registration for STQN’s prior auditor — Michael Studer CPA — who was barred following regulatory violations. This revocation undermines confidence in historical audited financial statements prepared during his tenure requiring increased scrutiny of past disclosures [S1].

These factors collectively elevate risk profiles for ongoing operational continuity absent successful strategic execution or adequate capital inflows.

Critical Capital Structure and Cash Flow Analysis

At fiscal year-end December 31, 2025 STQN reported current assets totaling only $5,388 against current liabilities of $13,319 yielding a current ratio near 0.4—a clear signal of short-term solvency stress relative to liabilities owed within one year [F1]. In stark contrast however is an unusually high reported cash ratio around 8.87 due primarily to available cash equivalents relative to short-term liabilities which may indicate concentration of liquid assets amidst otherwise constrained working capital components.

Yet overall equity remains negative at roughly -$7.9K demonstrating accumulated deficit position influenced by ongoing net losses eroding shareholder value since the merger date [F1]. Negative equity conditions typically render traditional return-on-equity metrics ineffectual given numerator-denominator sign conflicts; thus pure ROE analyses lack relevance.[F1]

No dividend payments or share repurchases have been declared—consistent with preservation of capital resources during loss-making phases prioritized towards sustaining core business operations instead.

Future Outlook: Growth Prospects and Strategic Constraints

Going forward STQN identifies strategic intent centered on developing a proprietary software platform designed specifically for digitized loan origination and servicing workflows optimized for blockchain-backed collateral assets [S1][S2]. Such proprietary technology is widely recognized across digital asset lenders as essential enabler for both operational efficiency gains and regulatory compliance monitoring under evolving fintech frameworks.

Nonetheless actual development efforts remain stalled chiefly due to funding unavailability as disclosed through latest quarterly updates ending September 30, 2025 limiting timeline visibility for delivering such strategic initiatives[S2]. Without technology deployment facilitating wider product offering beyond Bitcoin collateral or enhancing customer experience capabilities scaling may prove elusive.

The management explicitly acknowledges ongoing loss incursions will continue near-term reflecting investment-heavy phases pre-profitability thresholds achievable only upon broader lending recommencement coupled with platform rollout.[S1]

Key Milestones to Monitor for Turnaround Progress

(Analysis) Investors examining STQN should focus attention on several potential inflection points indicative of business stabilization or growth resumption:

- Formal announcements or SEC disclosures confirming recommencement of loan issuance volumes beyond July 2024 cessation.

- Material progress towards development milestones or beta launch updates of proprietary loan origination/servicing platform software.

- Capital raising rounds documented through SEC filings or press releases indicating enhanced financial flexibility.

- Improvement trajectories reflected within interim quarterly results concerning narrowing operating losses and positive free cash flow generation.

- Changes in auditor status including engagement of new independent registered public accounting firms restoring audit credibility.

Such milestones would materially alter perceptions regarding operating momentum restoration capacity amid competitive fintech ecosystems targeting digital asset lending demands.

Management’s Capital Allocation Approach and Investor Returns

Currently STQN prioritizes capital allocation toward sustaining lending infrastructure foundations alongside preparatory steps toward software platform creation rather than return distribution strategies typical among mature lenders such as dividends or share buybacks [F1][S1].

Persistent negative equity distorts conventional profitability metrics like ROE rendering them practically non-informative from shareholder value perspective despite numeric calculation attempts showing anomalous values given deficit base [F1]. Cash flows remain deployed primarily for working capital support versus capital return programs underscoring stage-appropriate reinvestment orientation during operational establishment phases.

The combination of recurring net losses alongside reliance on external funding raises questions over dilution risk exposure for shareholders inherent within subsequent financing rounds — an element warranting continuous surveillance through updated corporate disclosures going forward.

This analysis synthesizes publicly available SEC filings up to April 7th, 2026 alongside historical financial data snapshots compliant with provided evidence constraints. It avoids speculative forecasts outside stated corporate guidance or disclosed facts emphasizing transparent assessment aligned with buy-side analytical rigor tailored for understanding early-stage FinTech lending ventures reliant on digital asset ecosystems.

Disclaimer: This report is prepared solely for informational purposes without any recommendation regarding transactions involving STRATEGIC ACQUISITIONS INC /NV/. Readers should perform their own due diligence or consult professional advisors when considering related investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments