High-Trend International's Revenue Surge Overshadows Persistent Profitability Hurdles

The company nearly doubled revenue in FY2025 but continues to grapple with losses and moderate liquidity amid capital-intensive marine shipping challenges.

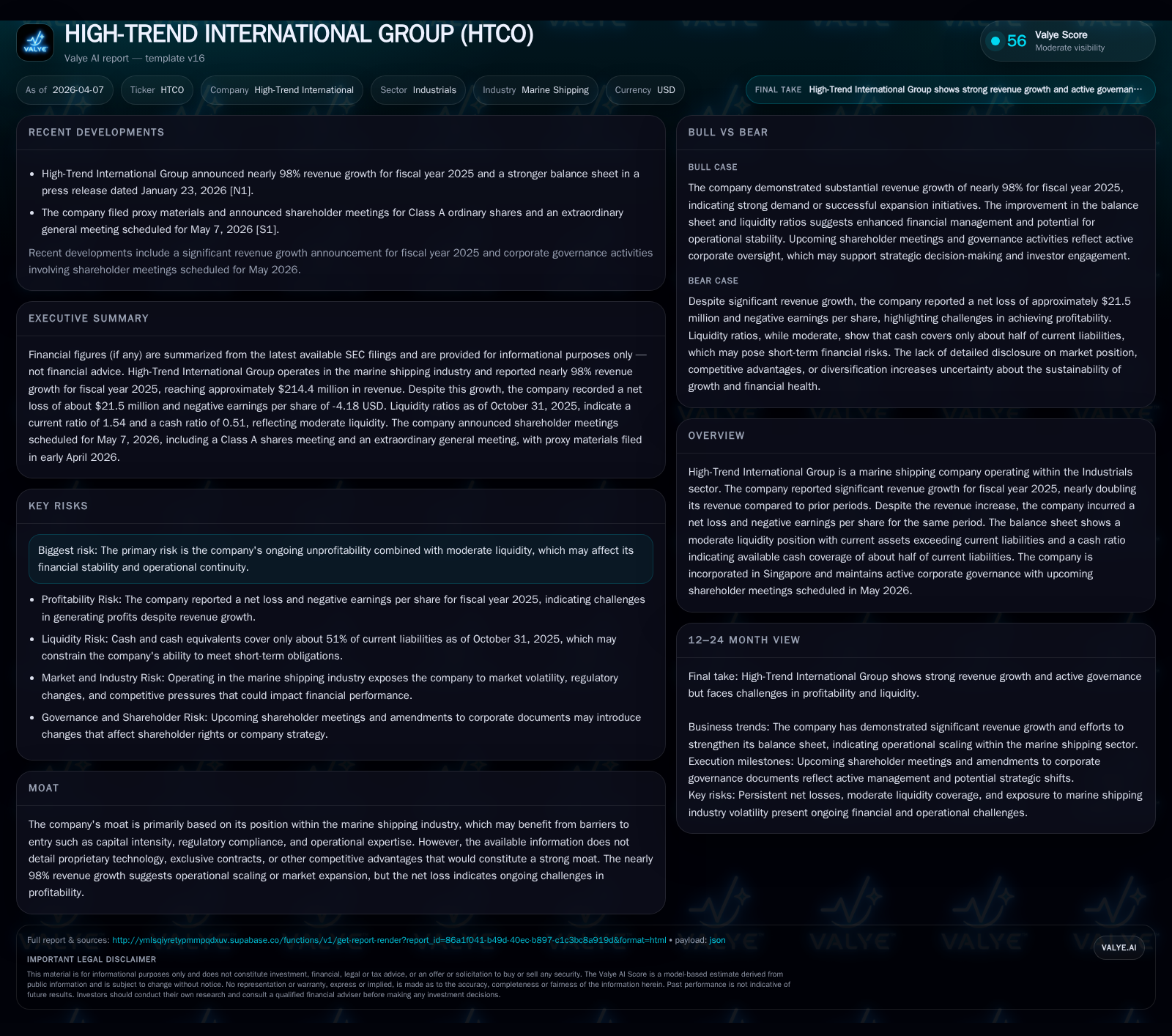

High-Trend International Group reported a substantial 98.2% revenue increase to $214.4 million in fiscal year 2025, reflecting strong operational scaling or market recovery within marine shipping. Despite this growth, the company recorded a net loss of $21.5 million and operating losses widened significantly, indicating ongoing margin pressures from sector-specific cost elements such as fuel and compliance. The balance sheet shows a current ratio of 1.54 and available cash covering about half of current liabilities, suggesting moderate liquidity but exposure to capital intensity risks. Dividend payments remained stable despite losses, while operating cash flow turned positive, marking a tentative improvement in cash generation.

Revenue Growth Trajectory: Explosive Gains and Operational Scaling

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 214 | -21 | 5 | -20 | +98.2% | +9.0% |

| 2024 | 108 | -24 | -3 | 2 | +13.6% | -152.9% |

| 2023 | 95 | -9 | -18 | -16 | -48.6% | -176.3% |

| 2022 | 185 | 12 | 33 | 24 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1 | 5 | -272.5 |

| 2024 | 1 | -440.0 | |

| 2023 | 1 | 172.6 | |

| 2022 | 17 | 33 | 269.8 |

Source: SEC companyfacts cache [F1].

High-Trend International’s fiscal year 2025 posted an impressive top-line leap to $214.4 million, translating into a nearly doubling (+98.2%) compared to $108.2 million recorded in FY2024 [F1]. This rapid escalation marks a critical shift from previous volatility seen in earlier years—for example, revenues had dropped from $185.3 million in FY2022 down to approximately $95.3 million in FY2023 before recovering strongly thereafter.

Such steep gains typically reflect elevated fleet utilization rates or heightened freight demand recovery within marine shipping—a sector notoriously susceptible to cyclical trade flows and global economic shifts. The jump contrasts with the significant contraction seen in FY2023 and suggests that High-Trend managed operational scaling successfully during the latest fiscal period, potentially capitalizing on market expansion or improved vessel deployment efficiency.

Challenging Profitability: Drivers Behind Operating and Net Losses

Despite translating revenue growth into scale, profitability metrics paint a starkly different picture. Operating income reversed dramatically from a positive $2.3 million gain in FY2024 to a negative swing approaching -$19.9 million in FY2025 [F1], representing an almost tenfold deterioration (-964% YoY). This margin squeeze aligns with increased cost pressures common in marine shipping such as spikes in fuel prices (bunker costs), regulatory compliance expenses related to environmental standards (e.g., IMO sulfur caps), and potential integration or maintenance costs tied to fleet expansion.

Net income followed suit with sustained losses of roughly -$21.5 million in FY2025 [F1], a slight worsening from prior year deficits but still indicative of structural profitability challenges despite revenue momentum.

The divergence between revenue and profitability highlights typical industrial shipping complexities: rising operational leverage does not necessarily translate quickly into margin improvement due to fixed cost burdens and volatile input costs affecting expense structures.

Liquidity and Balance Sheet Health: Assessing Financial Stability in 2025

The balance sheet reveals moderate liquidity resilience amid mounting losses. Current assets stood at approximately $30.3 million at fiscal year-end versus current liabilities of about $19.7 million, yielding a current ratio around 1.54x [F1]. Cash and equivalents totaled just over $10.1 million, covering roughly half (51%) of short-term obligations—a cautious buffer given the sector’s capital demands.

Equity recovered substantially from negative territory (-$5.4 million) two years ago up to nearly $7.9 million by end-FY2025 [F1]. While an encouraging trajectory, this equity level remains relatively modest considering the capital intensiveness typical for marine shipping companies needing continuous reinvestment into their fleets.

Taken together, these indicators suggest that while High-Trend has stabilized its near-term solvency profile somewhat, the company remains exposed to liquidity risk if operational losses persist or unexpected capex needs arise.

Capital Allocation Overview: Investment, Dividends, and Equity Trends

Capital expenditures were negligible at just above $5,000 for FY2025 [F1], a figure exceptionally low for an industrial-scale marine shipping entity where vessel acquisition or refurbishment can require multi-million dollar investments. Such minimal capex could imply deferred maintenance or reliance on existing fleet operational status rather than aggressive expansion.

Dividend payments were sustained at approximately $902,000 annually through recent years including FY2025 despite ongoing losses [F1]. This payout policy indicates management’s intent either to maintain shareholder return consistency or reflects limited options for internal reinvestment alongside losses.

Operating cash flow saw pivotal improvement returning positive at about $4.6 million after multiple years of negative cash generation [F1]. Free cash flow consequently is also positive near this level given minimal capex outlays.

The approximate return on equity (ROE) calculated as net income divided by equity was deeply negative at roughly -272% for FY2025 [F1], quantitatively reflecting poor returns relative to shareholders’ funds.

These capital allocation patterns underscore tension between preserving dividends amid financial strain and conservative investment decisions potentially limiting future growth prospects without external funding.

Growth Outlook: Navigating Market Expansion and Industry Barriers

Although direct company guidance or forecasts are absent [N#], High-Trend International’s moat primarily rests on industry inherent barriers such as substantial capital intensity to acquire/operate tankers & vessels, regulatory compliance complexity especially post-IMO emissions regulations, and operational expertise needed for global logistics coordination.

No explicit proprietary technology advantages or exclusive contracts have been documented that could offer significant competitive insulation beyond these broad industry factors . Thus market expansion will likely depend heavily on continuing fleet optimization, freight rate environments influenced by global trade trends, and ability to maintain cost discipline under volatile input price scenarios.

Given the recent top-line surge paired with continued losses and moderate equity base, growth potential is tempered by operational scaling risks and profitability turnaround requirements typical within marine shipping amid economic uncertainties.

Key Performance Milestones and What Investors Should Monitor

High-Trend has scheduled key shareholder meetings for early May 2026 encompassing both class A ordinary shares and general meeting agendas [S3]. These forums could serve as platforms for potential strategic pivots including capital structure decisions or governance adjustments.

Absent explicit forecasts from the company [N#], critical metrics warranting close observation include:

- Subsequent quarterly earnings tracking operating margin improvements or further erosion,

- Cash flow sustainability given limited capex commitments,

- Changes in dividend policy aligned with profitability trajectory,

- Evolution of equity base addressing solvency risks,

- Operational signals such as fleet utilization rates or contract renewals impacting revenue stability.

A sustainable profitability inflection supported by consistent free cash flow generation would represent an important turnaround milestone.

Conclusions on Risk-Return Profile Amid Marine Shipping Industry Constraints

High-Trend International exhibits a classic industrial shipping profile characterized by rapid revenue expansion enabled by fleet utilization gains or market rebound juxtaposed against persistent bottom-line deficits driven by margin pressures intrinsic to capital-intensive logistics operations.

While improving liquidity ratios and positive operating cash flows alleviate immediate solvency concerns somewhat, the modest equity base combined with sustained net losses weighs heavily on shareholder returns as reflected in deeply negative ROE figures.

Dividend consistency amid losses reveals management preference toward shareholder distributions possibly constraining reinvestment capacity needed for long-term growth acceleration.

Overall, the company’s risk-return balance hinges on its ability to convert scale advantages into structured profitability while navigating volatile marine fuel costs, strict regulatory landscapes, and competitive freight markets—no small feat given absent proprietary technological edges or lock-in contracts detailed thus far.

This analysis reflects exclusively reported financial data and disclosed corporate information without extrapolation beyond documented sources nor offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments