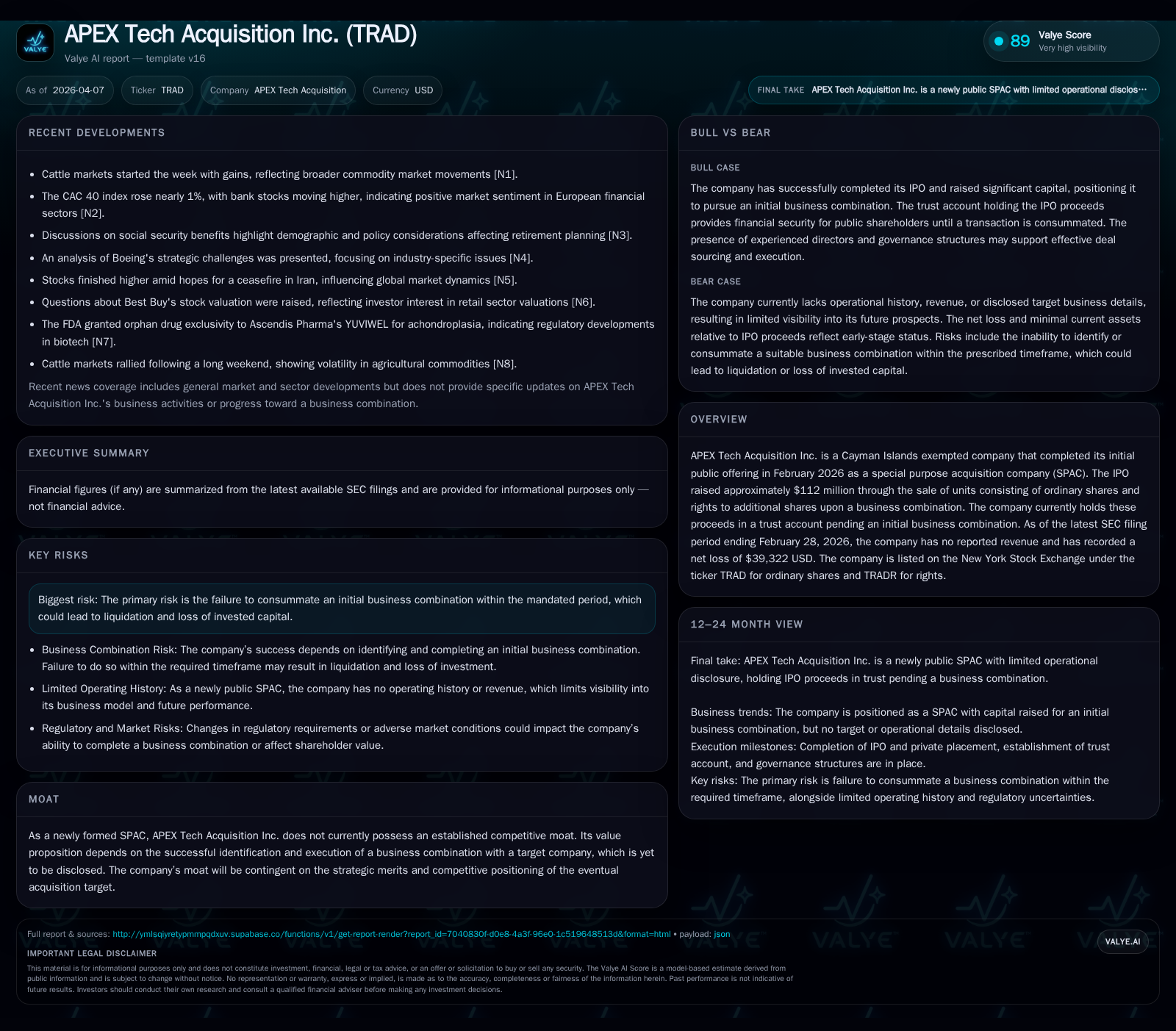

APEX Tech Acquisition Inc. Launches as SPAC with $112 Million Trust and Strategic Questions

A newly formed Cayman Islands SPAC raises capital, initiates with no revenue, and faces key timing challenges ahead of its first business combination.

APEX Tech Acquisition Inc. completed its IPO in February 2026, raising approximately $112 million, which is held in a trust account pending an initial acquisition. With no revenue and a modest net loss reflecting startup operating expenses, the company’s future growth depends entirely on successfully executing a business combination. Investors should monitor deal announcement timelines and redemption dynamics, as failure to close within the prescribed period risks liquidation and loss of capital.

A Short History: From Formation to IPO Completion

APEX Tech Acquisition Inc., incorporated as a Cayman Islands exempted company, officially entered the public markets when it completed its initial public offering (IPO) in late February 2026 [S3][S5]. The offering consisted of approximately 11.2 million public units priced at $10 each, representing ordinary shares coupled with rights entitling holders to additional shares upon consummation of an initial business combination. Concurrently, the sponsor subscribed for about 209,000 private units under similar terms contributing roughly $2.1 million in proceeds [S5][S7]. Following close of the IPO and private placement, APEX traded its ordinary shares on the New York Stock Exchange under ticker "TRAD," with associated rights trading as "TRADR" [S3]. This timeline reflects rapid progression from registration filings in December 2025 to public listing within three months—an efficient capitalization phase characteristic of well-sponsored Special Purpose Acquisition Companies (SPACs).

Financial Foundations: Initial Capital Raise and Asset Composition

The gross proceeds from both the public offering and private placement totaled approximately $114 million, with $111.97 million deposited into a segregated trust account specifically established for safeguarding investor funds pending an initial business combination [S5][S8][F1]. This trust structure is standard in SPAC frameworks to ensure capital preservation and mitigate liquidity risk prior to deal execution. As of the latest financial statements dated February 28, 2026, current assets stood at roughly $584,000 representing cash outside of the trust account used for administrative purposes; importantly, current liabilities were nil indicating no outstanding short-term obligations [F1]. The balance sheet paints a clear picture—a bulk of cash securely held in escrow awaiting deployment.

Zero Revenue Phase: Interpreting Early Losses and Operating Costs

Predictably for SPACs in their infancy without operational subsidiaries or revenue generation capability, APEX’s income statement through February reports no top-line sales activity. Instead, it registered a net loss marginally above $39,000—amounts accrued predominantly from general administrative expenses related to corporate maintenance and regulatory compliance preceding any actual business combination pursuit [F1]. Such nominal losses align with ongoing cost recognition typical for newly formed SPACs whose burn rate remains tightly controlled given limited personnel and reliance on third-party advisers. These early expenses set a baseline operational drag to monitor before meaningful deal costs or integration expenditures arise.

Strategic Outlook: Anticipated Business Combination and Value Drivers

The core investment thesis for APEX hinges on identifying one or more attractive technology-focused targets for its planned de-SPAC transaction. While specific target candidates remain undisclosed publicly, management’s ability to deploy capital successfully into an entity with scalable growth potential will ultimately define shareholder value realization . Key levers post-acquisition include synergy capture opportunities, revenue ramp from acquired operations, and capacity for raising further PIPE (Private Investment in Public Equity) financing frequently necessary to supplement SPAC equity pools during such transactions.

Should the company complete its first merger promptly within exchange-imposed deadlines (typically two years from IPO), it may capitalize on favorable market conditions and investor appetite for innovative tech businesses. The competitive moat traditionally attributed to operating businesses does not exist today; instead APEX’s advantage depends solely on strategic due diligence prowess and seller alignment at transaction closing.

Risks on the Horizon: Navigating Time Limits and Market Uncertainties

Amongst primary risk factors faced by APEX is failure to consummate an initial business combination before expiration of its mandate which triggers automatic liquidation procedures distributing remaining trust assets back pro rata but resulting in loss exposure including unfunded sponsor interests [S4]. Unlike larger reporting companies that provide fuller risk factor narratives per regulatory requirements, as a smaller reporting company APEX’s disclosures here remain succinct though underline this existential threat strongly.

Additional risks borne stem from volatile equity markets influencing investor redemptions rights exercised ahead of merger votes which can materially impact available deal funding size or valuation negotiation dynamics — common stress points inherent throughout SPAC lifecycle stages.

Capital Allocation Approach: Trust Account Structure and Absence of Dividends

Given the pre-combination stage profile where proceeds reside mostly untouched within a trust account managed by Continental Stock Transfer & Trust Company as trustee [S5], capital deployment beyond administrative expenses is highly restricted. No dividends or share repurchase programs have been declared nor are expected until after completion of an initial business combination when operating cash flow profiles can support distributions safely.

Sponsor units obtained via private placement remain subject to lock-up provisions typically extending at least 30 days post-combination closing limiting immediate dilution effects while aligning managerial incentives around successful deal closure rather than early liquidity extraction. Management expense reimbursements only relate to specific costs incurred supporting search activities rather than ongoing overhead commitments [S9].

Key Metrics Table: Financial Performance Snapshot Since Incorporation

Historical performance (annual)

| FY |

|---|

| 2026 |

Source: SEC companyfacts cache [F1].

This table encapsulates earliest reported accounting outcomes during APEX's pre-merger existence highlighting foundational financial health constrained by nascent activity status.

Forward Look: Monitoring Milestones for Value Realization

Going forward, stakeholders should track early announcements signposting potential acquisition targets or entering substantive negotiations. Shareholder votes authorizing mergers will represent pivotal events alongside transparency around redemption elections exercised by unit holders exercising their right to liquidate their pro-rata portion from trust accounts before deal closure.

Market participants commonly scrutinize tentative deal pipelines issued in press releases or SEC filings while assessing listing maintenance criteria imposed by NYSE ensures regulatory compliance continues seamlessly. Conversion rights attached to underlying securities after deal consummation impact capital structure evolution effecting longer-term equity dilution considerations.

Absent explicit guidance on timing milestones yet disclosed publicly by APEX management thus far, careful attention is warranted towards quarterly updates reflective of progress toward deal consummation deadlines.

This analysis draws exclusively upon publicly filed SEC documents dated through April 7, 2026 [F1], alongside Valye internal report excerpts provided without conjecture beyond documented statements. The content herein excludes investment recommendations or price forecasts in compliance with analytic best practices.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments